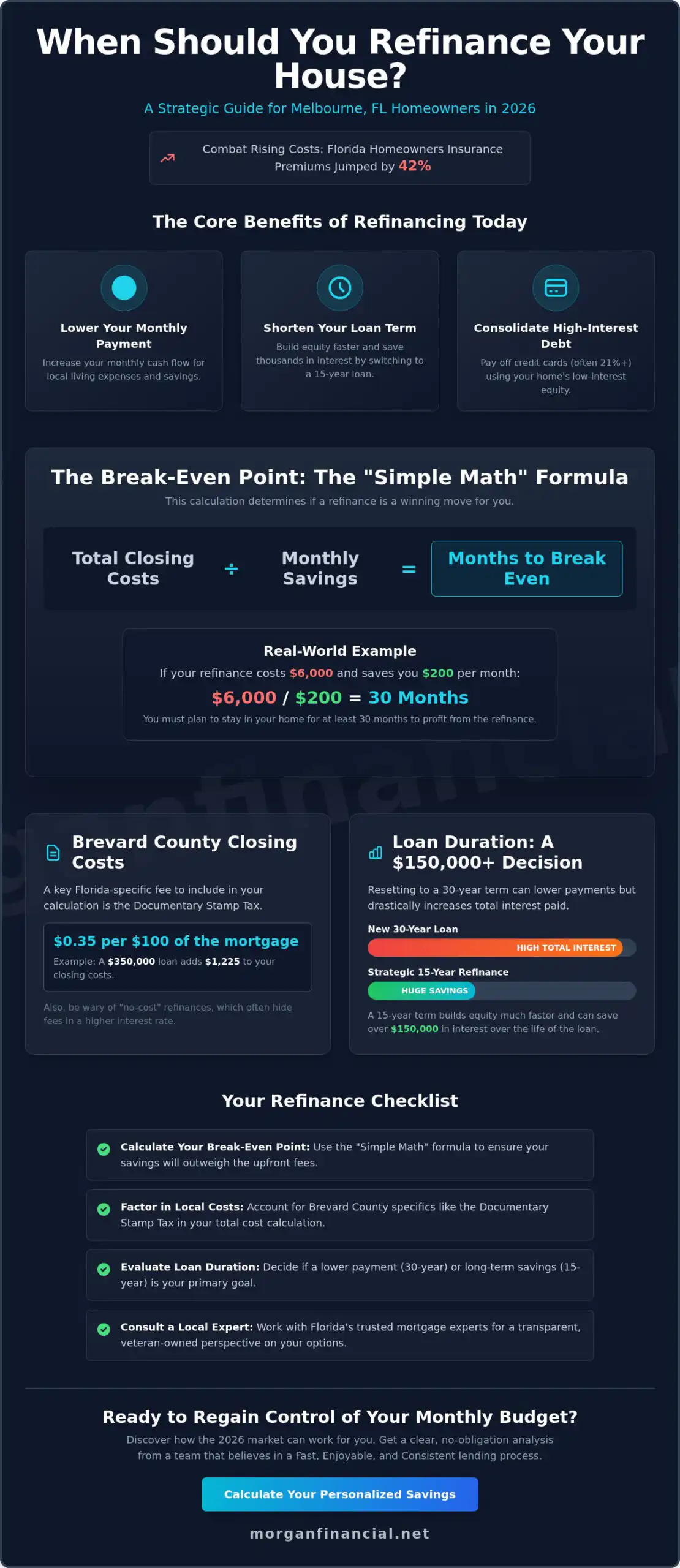

Waiting for a specific interest rate might actually be costing you more than the closing costs you’re trying to avoid. You’ve likely watched your monthly escrow climb as Florida homeowners insurance premiums jumped by 42% in recent years according to data from the Insurance Information Institute. It’s exhausting when high monthly payments eat into your disposable income, and determining exactly when should you refinance your house can feel overwhelming without the right data. We believe the lending process should be fast, enjoyable, and consistent for every Melbourne homeowner.

You deserve to know the exact financial triggers and Brevard County market conditions that make a new loan a winning move in 2026. This guide delivers a professional roadmap to help you decide if the long-term savings will outweigh the upfront fees. We’ll break down the math behind the break-even point and show you how to offset rising local costs through strategic equity management. Discover how to regain control of your monthly budget with the confidence of a seasoned local expert by your side.

Key Takeaways

- Master the “Simple Math” formula to calculate your break-even point and ensure your refinance delivers immediate financial value.

- Identify the specific Space Coast market conditions and triggers that signal when should you refinance your house for maximum savings.

- Compare VA IRRRL and Conventional options to discover the “Fast. Enjoyable. Consistent.” path tailored to your unique military or civilian status.

- Understand how local Brevard factors, including homeowners insurance shifts and “Save Our Homes” tax caps, impact your new escrow account.

- Learn how working with Florida’s trusted mortgage experts simplifies the process through a transparent, veteran-owned perspective.

Understanding Mortgage Refinancing in the 2026 Melbourne Market

Refinancing is a strategic financial move. At its core, it involves what refinancing is; replacing your current mortgage with a new loan to secure better terms or access your home’s equity. For Space Coast homeowners in 2026, this decision is more relevant than ever. Brevard County property values have shifted significantly over the last three years, meaning many residents now sit on more equity than they realize. As Florida’s Trusted Mortgage Experts, we help you determine if the current market aligns with your long-term goals.

You generally choose between two primary paths. A rate-and-term refinance focuses on changing your interest rate or the length of your loan without taking out extra cash. A cash-out refinance allows you to tap into your home’s value to receive a lump sum. Both options aim to improve your financial health by reducing your monthly obligation or the total interest paid over time. Determining when should you refinance your house requires a clear look at your current rate versus what the 2026 market offers.

The Core Benefits of Refinancing Today

Refinancing isn’t just about a lower number on a page. It’s about freedom and flexibility. Fast. Enjoyable. Consistent. That’s how the process should feel. Here are the primary reasons Melbourne residents are re-evaluating their debt this year:

- Lowering your monthly mortgage payment: Reducing your rate by even a small margin can increase your monthly cash flow for local living expenses.

- Shortening your loan term: Moving from a 30-year to a 15-year mortgage helps you build equity faster and save thousands in interest.

- Consolidating high-interest debt: Use your home equity to pay off credit cards or personal loans that often carry rates above 21%.

If you want to see how these changes impact your bottom line, you can explore our easy refinance options to get started.

When “Just Lowering the Rate” Isn’t Enough

A 0.5% drop in interest rates might be a massive win for a homeowner with a $500,000 balance, but it might not justify the costs for someone with a $150,000 balance. You must consider the closing costs associated with the new loan. It is vital to stay in the home long enough to see the actual benefit of the change. The break-even point for a Space Coast homeowner is the specific month when your cumulative monthly savings finally surpass the total closing costs of the new loan. Knowing when should you refinance your house depends entirely on this calculation and your future plans in the Melbourne area.

The Math Behind the Move: Calculating Your Break-Even Point

Deciding when should you refinance your house in Melbourne depends on one specific metric: the break-even point. This is the exact month where your accumulated savings from a lower interest rate finally exceed the upfront costs of the new loan. If you move or sell before reaching this point, you have lost money on the transaction. It is a simple calculation, but the variables change based on Florida’s specific tax laws and your long-term goals.

Determining when should you refinance your house requires looking beyond just the interest rate. Use this formula: Total Closing Costs / Monthly Savings = Months to Break Even. For example, if your refinance costs $6,000 and saves you $200 per month, it takes 30 months to recover your investment. Florida homeowners must account for the documentary stamp tax on notes, which is currently $0.35 per $100 of the mortgage amount. On a $350,000 loan, this tax alone adds $1,225 to your total. You must factor in your planned tenure in the home to ensure the math aligns with your life plans.

Evaluating Closing Costs in Brevard County

Closing costs in Brevard County typically include the appraisal fee, title search, and lender origination charges. You should examine your Loan Estimate carefully for “no-cost” refinance traps. These programs aren’t actually free. Lenders often increase the interest rate to cover the fees, which costs you more over the long term. It is often better to pay the costs upfront to secure the lowest possible rate. You can run these scenarios yourself using Mortgage Calculators to see how different fee structures affect your monthly payment.

The Impact of Loan Duration

Duration is just as important as the interest rate. If you have already paid ten years on a 30-year mortgage, refinancing into a new 30-year loan resets the clock. You might lower your monthly payment, but you will pay significantly more interest over the additional decade. A strategic alternative is a 15-year refinance. While the monthly payment might stay the same or increase slightly, the interest savings can exceed $150,000 over the life of the loan. This approach builds equity faster and clears your debt sooner. If you want a personalized look at your numbers, reach out to a local expert who understands the Melbourne market.

VA vs. Conventional: Choosing the Best Refinance Path

Choosing the right loan product depends on your military status and your specific financial goals in Brevard County. For many local families, the decision of when should you refinance your house hinges on whether they can leverage unique VA benefits or if a conventional loan offers better flexibility for their current equity. Morgan Financial provides the expertise to help you navigate these choices with a process that is Fast. Enjoyable. Consistent.

The VA IRRRL: The Space Coast Veteran’s Secret Weapon

If you currently hold a VA loan, the Interest Rate Reduction Refinance Loan (IRRRL) is often the most efficient path. This “streamline” refinance is built for speed. It requires no appraisal and minimal paperwork, making it an ideal choice for veterans working at Patrick Space Force Base or living in Melbourne. To qualify, you must meet the “Net Tangible Benefit” rule. This rule dictates that the refinance must provide a clear financial advantage, such as lowering your interest rate by at least 0.5% or moving from a volatile variable rate to a stable fixed rate.

- No out-of-pocket costs options are often available.

- No new home inspection or appraisal is required in most cases.

- Fast closing times help you lock in 2026 market rates quickly.

Learn more about your specific benefits at our VA Loan Resource page.

Conventional Refinance for Palm Bay and Viera Homeowners

Homeowners in Viera and Palm Bay often choose conventional refinances to eliminate Private Mortgage Insurance (PMI). Once your home equity reaches 20%, refinancing into a conventional loan can save you significant money by dropping that monthly insurance premium. With Viera home values seeing steady appreciation through 2025 and into 2026, many residents now have the Loan-to-Value (LTV) ratio required to make this move. A conventional refi also allows you to exit a restrictive Adjustable-Rate Mortgage (ARM) in favor of a 15 or 30-year fixed term, providing long-term budget certainty.

Florida’s Trusted Mortgage Experts can also help you transition from a conventional loan into a VA loan. If you are an eligible veteran currently using a conventional mortgage, you can refinance into a VA loan to take advantage of typically lower interest rates. For those needing liquidity, a VA Cash-Out refinance in Florida requires a valid Certificate of Eligibility (COE) and allows you to access up to 100% of your home’s value. This is a strategic move for those looking to fund home improvements or consolidate high-interest debt. Determining when should you refinance your house depends on these specific equity benchmarks and your long-term plans for your Florida property.

Local Brevard Factors: Insurance, Taxes, and Escrow

Deciding when should you refinance your house involves more than just watching the national interest rate ticker. In Melbourne and the surrounding Space Coast areas, local escrow factors often dictate whether a refinance actually saves you money. Your monthly mortgage payment consists of principal, interest, taxes, and insurance. While the interest rate might look attractive, Florida’s unique insurance and tax landscape can shift the final numbers significantly.

Managing Rising Florida Insurance Premiums

Florida’s homeowners insurance market remains a primary concern for any borrower in 2026. When you start the refinance process, your new lender will re-evaluate your current windstorm and hazard coverage. They need to ensure the policy meets modern replacement cost requirements. It’s a common reality where a homeowner’s monthly payment goes UP even if their interest rate goes DOWN. This happens because the escrow account must be funded at today’s higher premium rates rather than the rates from three or four years ago.

- Review your current declarations page to see if you have a separate hurricane deductible.

- Get a wind mitigation inspection if yours is older than five years; it can save you hundreds on premiums.

- Shop with local Melbourne insurance agents who understand coastal building codes before you sign your final loan documents.

Property Tax Assessments in Titusville and Cocoa Beach

A common myth circulating in Brevard County is that refinancing triggers a property tax re-assessment. This is false. Under Florida’s “Save Our Homes” law, your assessed value remains capped as long as the title doesn’t change hands in a way that triggers a reset. Refinancing your existing debt doesn’t count as a change in ownership. You can check your current standing on the Brevard County Property Appraiser’s website to ensure your exemptions, like the Homestead Exemption, are correctly applied.

A sale appraisal determines the market price for a buyer, while a refinance appraisal verifies the home’s value to secure the lender’s loan-to-value requirements. This distinction is vital in a rapidly changing market like the Space Coast. With local aerospace and tech growth driving demand, values in neighborhoods from Viera to Palm Bay can shift by 4% or 5% within a single six-month period. Local expertise prevents “escrow shock,” which occurs when a lender underestimates your taxes or insurance, leading to a painful payment spike the following year.

Our team at Morgan Financial focuses on making the numbers work for your specific Florida home. We provide the steady hand you need to navigate these local variables. Fast. Enjoyable. Consistent.

How Morgan Financial Simplifies Your Refinance Process

Deciding when should you refinance your house is a major financial milestone that requires more than just a calculator. It requires a partner who understands the nuances of the Brevard County market. At Morgan Financial, we’ve built our reputation on a simple promise: Fast. Enjoyable. Consistent. We don’t just process paperwork; we guide our neighbors through a streamlined experience designed to eliminate the typical anxiety associated with mortgage lending.

Our identity as a veteran-owned business shapes every interaction. We prioritize integrity and transparency, ensuring you understand every fee and timeline from day one. While national lenders often treat you as a data point in a massive database, our team provides the steady hand you need to navigate the 2026 economy. We focus on getting you to the closing table with high-energy efficiency so you can start benefiting from your new terms immediately.

The Morgan Financial Advantage

Working with a local Melbourne expert offers benefits that a national “big bank” call center simply can’t provide. You get direct access to your mortgage expert throughout the entire journey. We know the specific property values in Melbourne, Palm Bay, and the surrounding Beaches because we live and work here too. This local insight allows us to move faster and anticipate hurdles before they arise. Start your journey with our Easy Refinance tool to see how we bring “Fast. Enjoyable. Consistent.” to life.

- Direct communication with a dedicated professional, not a rotating queue of anonymous operators.

- In-depth knowledge of Florida-specific lending requirements and local appraisal trends.

- A commitment to a stress-free experience that respects your time and financial goals.

Ready to Secure Your Financial Future?

Taking the first step toward a better rate is easier than most homeowners realize. To get a quick and accurate quote, simply gather your current mortgage statement and your most recent pay stubs. These documents allow our experts to provide a personalized analysis based on your current equity and income. With market shifts projected throughout 2026, locking in your strategy now is the smartest way to protect your home’s value. Don’t wait for the next economic shift to wonder if you missed your window. Contact a Mortgage Expert today for a personalized analysis of your options.

Take Control of Your Melbourne Home Equity

Navigating the 2026 mortgage landscape requires more than just watching interest rates. You need to calculate your specific break-even point, which typically lands between 18 and 30 months for most Melbourne homeowners according to current industry benchmarks. Understanding when should you refinance your house involves balancing these timelines with Brevard County’s specific insurance and tax escrow requirements. Whether you’re leveraging the benefits of a VA loan or moving into a conventional mortgage, the right strategy can save you thousands over the life of your loan.

Morgan Financial stands as Florida’s Trusted Mortgage Experts. As a Veteran-Owned and Operated business, we take pride in delivering a lending experience that is Fast. Enjoyable. Consistent. Our team is ready to help you analyze 2026 market data and find the path that fits your budget. Your home is your largest investment, and it deserves the attention of seasoned professionals who live and work right here in Brevard. We’re here to ensure your next financial move is your best one yet.

Check your 2026 refinance options with our Easy Refinance tool

Frequently Asked Questions

Is it worth it to refinance for a 0.5% lower interest rate?

It’s often worth it if you plan to stay in your Melbourne home long enough to recoup the closing costs. A 0.5% reduction on a $350,000 loan saves about $115 monthly. If your closing costs are $6,000, your break-even point is approximately 52 months. Our experts help you calculate this exact timeline so you know exactly when should you refinance your house to maximize your long-term savings.

How much are the typical closing costs for a refinance in Florida?

Florida closing costs typically range between 2% and 5% of your total loan amount based on 2024 industry averages from Freddie Mac. For a $400,000 refinance in Melbourne, you should expect to pay between $8,000 and $20,000 at the closing table. These costs include appraisal fees, title insurance, and state taxes. We keep the process transparent and consistent so there aren’t any surprises at the finish line.

Can I refinance my house if I have a VA loan?

You can absolutely refinance a VA loan into a new VA loan or a conventional mortgage. Veterans in Brevard County often use this path to lower their monthly payments or pull equity for home improvements. Deciding when should you refinance your house depends on current market rates and your personal financial goals. We specialize in VA lending and ensure the transition is fast and stress-free for our local heroes.

What is a VA IRRRL and who is eligible in Melbourne?

A VA Interest Rate Reduction Refinance Loan (IRRRL) is a streamline option designed for homeowners who already have a VA-backed mortgage. To be eligible in Melbourne, you must show a net tangible benefit, such as a lower interest rate or a shift from an adjustable to a fixed rate. This program requires minimal paperwork and usually doesn’t need a new appraisal, making the entire experience fast and enjoyable for military families.

How long does the mortgage refinance process take with Morgan Financial?

Morgan Financial streamlines the mortgage refinance process to close most loans in 30 days or less. Our high-energy team uses an efficient system to eliminate the typical delays found at big banks. We focus on being fast, enjoyable, and consistent for every Melbourne homeowner. You’ll receive regular updates throughout the journey, ensuring you’re never left wondering about the status of your application or your scheduled closing date.

Will refinancing my house lower my property taxes in Brevard County?

Refinancing your mortgage won’t lower your property taxes because those are determined by the Brevard County Property Appraiser. Taxes are calculated based on your home’s assessed value as of January 1st each year. While a refinance changes your loan terms, it doesn’t impact the municipal tax rate or your Save Our Homes assessment cap. You’ll still pay the same amount to the county regardless of your new interest rate.

Can I get cash out of my home during a refinance to pay for repairs?

You can use a cash-out refinance to access your home’s equity for repairs or renovations. Most lending guidelines, including those from Fannie Mae, allow you to borrow up to 80% of your home’s current appraised value. If your Melbourne home is worth $500,000 and you owe $300,000, you could potentially access $100,000 in cash. This is a powerful tool for maintaining your property’s value while securing a professional, low-rate loan.

If you’re looking for funds but prefer not to borrow against your home’s equity, you can check out ILoveUrLoans for personal and installment loan options that provide quick access to capital.

What credit score do I need to refinance my mortgage in 2026?

You generally need a minimum credit score of 620 for a conventional refinance according to 2024 Fannie Mae standards. If you’re looking at an FHA refinance, you might qualify with a score as low as 580. Higher scores above 740 typically unlock the most competitive interest rates in the 2026 market. Our experts review your credit profile to help you secure the best possible terms for your specific financial situation.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.