You’ve spent weeks searching for the perfect Florida home, but a low appraisal suddenly threatens to derail your dream. It’s a high-stakes moment that creates immediate anxiety for any buyer. You’re likely wondering, what is the VA Tidewater Initiative and does it mean your deal is over? Far from being a deal-killer, this process is a vital 48-hour second chance designed to protect your path to homeownership. We’re here to help you turn a potential setback into a successful closing.

We know the stress of facing a ticking clock when your future home is on the line. This guide breaks down exactly how to navigate the two-day window and how to help your agent provide the right data to the appraiser. You’ll learn how to leverage the latest VA Home Loan updates to save your purchase without paying more out of pocket. We’ll show you how to handle the pressure, find better comps, and secure your property with total confidence.

Key Takeaways

- Understand what is the VA Tidewater Initiative and how it functions as a critical safety net for your home’s value.

- Navigate the firm 48-hour window with confidence by knowing exactly when and how the appraiser triggers this protocol.

- Differentiate between Tidewater and a Reconsideration of Value (ROV) to choose the fastest, most effective path to a successful closing.

- Identify high-quality comparable sales in local markets like Melbourne or Palm Bay to support your purchase price with precision.

- Leverage the regional expertise of a dedicated VA Home Loan specialist to manage complex appraisal rules with effortless confidence.

What is the VA Tidewater Initiative? Definition and Purpose

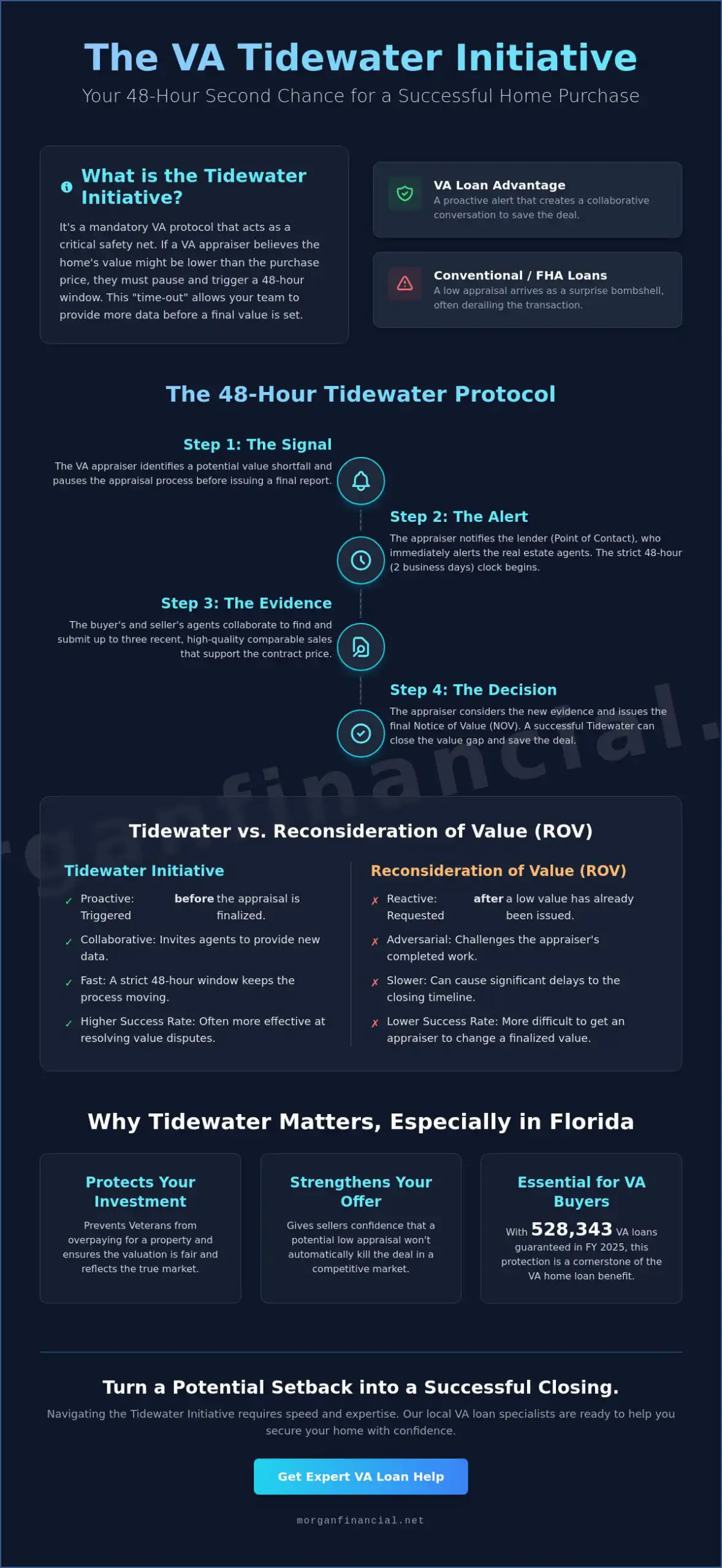

What is the VA Tidewater Initiative? At its core, it is a mandatory communication protocol. It requires a VA appraiser to stop and notify the lender if the property’s appraised value looks like it will come in lower than the contract price. Think of it as a formal "time-out." This system is named after the Tidewater region of Virginia, where the program was originally tested and proven successful. While most loan types leave you in the dark until the final report arrives, the VA loan program offers this proactive alert. It’s a distinct advantage. It’s a shield. It’s a second chance.

Unlike FHA or conventional financing, where a low appraisal often lands like a surprise bombshell, Tidewater forces a pause. This pause allows your real estate team to gather better data. It ensures the appraiser hasn’t missed a recent high-value sale. The mission is simple: protect veterans from overpaying while ensuring the valuation reflects the true market. This process is built into the VA Home Loan framework to keep your transaction on track when the numbers don’t immediately align. It turns a potential roadblock into a collaborative conversation.

The Goal: Protecting Your Investment

The primary objective is to prevent an appraisal gap from immediately killing your home purchase. By triggering a 48-hour window for additional data, the VA Tidewater Initiative empowers you. You aren’t just a bystander in the valuation process. You have a voice. This protocol ensures that every relevant local sale is on the table before the final Notice of Value (NOV) is issued. It maintains the integrity of your benefits by keeping the process transparent and collaborative. It prevents "low-ball" appraisals from ignoring the nuances of a specific neighborhood or unique property features that may justify a higher price point.

Why It Matters in the 2026 Florida Market

In the 2026 Florida real estate landscape, especially across Brevard County, market shifts happen fast. Prices in Melbourne and Palm Bay can fluctuate based on new space industry growth or inventory changes. During the 2025 fiscal year, the VA guaranteed 528,343 home loans nationwide. That high volume proves how essential these protections are for modern buyers. In a competitive "Space Coast" bidding war, having a built-in mechanism to address low appraisals makes your offer stronger. It gives sellers confidence that the deal won’t just collapse at the finish line. It positions you as a serious, protected buyer who is ready to close. You aren’t just another applicant; you’re a veteran with a specialized support system designed for your success.

The 48-Hour Window: How the Tidewater Process Works

The moment a VA appraiser realizes the property value might fall short of the contract price, they don’t just file a low report. Instead, they invoke a specific protocol. Understanding How the Tidewater Process Works is essential for every Florida veteran. The appraiser contacts the designated Point of Contact (POC), which is typically the lender, to signal that the Tidewater Initiative is active. At this stage, the appraiser cannot disclose the exact value they’ve found. They only signal that a gap exists. It is a high-speed mission to protect your deal.

This notification starts a strict 48-hour clock. This isn’t just a suggestion; it is a firm regulatory deadline. During these two business days, the real estate agents must provide additional data to support the sales price. If you’ve ever wondered what is the VA Tidewater Initiative, think of it as your emergency response system for home appraisals. It requires immediate action and precise coordination between all parties involved. There is no room for delay when your future home is on the line.

Step-by-Step Breakdown of the Protocol

The process follows a logical, rapid sequence to ensure fairness and accuracy. It demands total coordination between your lender and your real estate agent. We handle these steps with professional confidence to keep your closing on track.

-

Step 1: The Signal. The appraiser identifies a potential value issue and pauses the appraisal report without disclosing the current number.

-

Step 2: The Alert. The lender immediately notifies the buyer’s and seller’s agents. Speed is everything here.

-

Step 3: The Evidence. Agents have 48 hours to gather up to three strong comparable sales that the appraiser might have overlooked.

-

Step 4: The Decision. The appraiser reviews the new data and issues the final Notice of Value (NOV).

Critical Deadlines You Can’t Miss

The 48-hour window refers specifically to business days. If the appraiser invokes Tidewater on a Friday afternoon, the clock typically doesn’t expire until Tuesday. However, federal holidays can shift this timeline. You don’t want to leave your dream home to chance. If the window closes without a response, the appraiser must proceed with their original, lower valuation. This often leads to a deal-killing appraisal gap. Working with a team that understands these nuances is vital. If you have questions about your specific situation, reach out to our local specialists today. We ensure every second of that 48-hour window is used effectively. Our goal is to keep your purchase moving forward without unnecessary delays. We act fast. We stay transparent. We deliver results for our neighbors.

Tidewater vs. Reconsideration of Value (ROV)

Many buyers get confused by the technical jargon of the VA loan process. It’s understandable. When you are trying to understand What is the VA Tidewater Initiative, you must recognize that it is a "pre-final" intervention. It happens while the appraiser is still drafting the report. A Reconsideration of Value (ROV), however, is a formal appeal that occurs only after the final Notice of Value (NOV) has been issued. Think of Tidewater as a proactive warning and the ROV as a reactive appeal. One is collaborative; the other is often confrontational.

Timing is the biggest differentiator here. During Tidewater, the appraiser is essentially saying, "I can’t find the value; please show me what I’m missing." Once that report is finalized and the NOV is published, that door slams shut. At that point, you enter the ROV phase. The burden of proof shifts significantly. In Tidewater, you are simply providing additional context. In an ROV, you are often trying to prove the appraiser made a professional error. Winning an ROV is statistically much harder. It requires a Staff Appraisal Reviewer (SAR) to override a peer’s judgment. It’s slower. It’s more complex. It’s inherently more stressful.

Success rates are generally much higher during the Tidewater phase. Because the appraiser hasn’t "gone on the record" with a final number yet, they are more open to reviewing new data. Using the VA Home Loan benefit effectively means winning the battle as early as possible. We focus on getting it right the first time. We understand that a successful closing depends on managing these nuances before they become major obstacles.

When to Use the Reconsideration of Value

Sometimes Tidewater doesn’t solve the problem. If the appraiser ignores perfectly valid comps without a logical explanation, an ROV is your next move. It’s also the correct path if the report contains blatant factual errors. If the appraiser missed a bedroom, got the square footage wrong, or overlooked a major upgrade, the SAR can step in to correct the record. It is a formal safety net for when the standard process fails to produce an accurate result.

Why Tidewater is Your Best Defense

Tidewater remains your strongest tool because it keeps your momentum alive. It allows for "pending" sales data to be considered, which is crucial in a fast-moving market. This collaborative moment saves your closing timeline. Instead of waiting weeks for a formal appeal process, you resolve the issue in 48 hours. It is the steady hand in a complex landscape. It protects your earnest money. It protects your dream home. It ensures you don’t pay more out of pocket than necessary.

Winning the Tidewater: Selecting Comps in Brevard County

Winning a Tidewater challenge in Brevard County requires more than just a list of nearby houses. It demands a strategic, data-driven approach tailored to the Space Coast market. National lenders often rely on generic algorithms, but local expertise provides the nuance needed to sway an appraiser. When you are explaining what is the VA Tidewater Initiative to a concerned seller, your ability to present ironclad data is your best leverage. You need to prove the value with precision.

Location is paramount. In dense areas like Melbourne or Palm Bay, you should prioritize sales within a one-mile radius of the subject property. If you stray too far, the appraiser may discount the data as irrelevant to the specific neighborhood dynamic. Timing is equally critical. In a volatile market, sales from the last 90 days carry significantly more weight than older transactions. We look for the most current snapshots of market health to ensure the appraiser sees the same upward trends that you do. Finally, match the physical characteristics. Focus on homes within 20% of the subject’s square footage, similar year built, and comparable lot sizes.

Brevard County has unique property features that require special attention during the valuation process. A home with modern hurricane shutters, a recently resurfaced pool, or direct waterfront access in Merritt Island commands a premium that generic reports might miss. You must ensure these "Space Coast nuances" are highlighted clearly. This isn’t just about finding three houses; it’s about finding the right three houses that mirror the lifestyle and safety features of your potential new home.

What Makes a "Strong" Comp?

Not all sales are created equal. To win during the 48-hour window, you must provide the highest quality evidence possible. This keeps the process moving forward with professional confidence.

-

Closed Sales: These are the gold standard. They represent completed transactions and verified market value.

-

Subdivision Priority: Properties within the same HOA or subdivision are always prioritized over homes across a major thoroughfare.

-

Pending Sales: While not as strong as closed sales, pending contracts serve as vital supporting evidence of current demand.

-

No Outliers: Avoid "distress" sales or family-to-family transfers that don’t reflect true fair market value.

Collaboration Between Agent and Lender

The Tidewater response is a team effort. Your real estate agent must format the data into a clear, concise narrative. It isn’t enough to just send a spreadsheet; they must explain why these specific comps are superior to the ones the appraiser originally used. This narrative bridge is often what secures the higher valuation. To prepare for this possibility, it helps to Learn more about the VA loan purchase process and how we support our clients through every hurdle. We act as your steady hand. We provide the tools. If you’re ready to start your journey with a team that knows the local landscape, speak with our VA loan specialists today. We’re here to turn your homeownership goals into a reality.

Why a Local VA Specialist Makes the Difference

Choosing the right lender is the most critical decision you’ll make after finding your home. National call centers often treat your file as just another number. They lack the geographic seal of approval that only a regional authority can provide. When you are faced with a low valuation and need to understand what is the VA Tidewater Initiative, you don’t want to talk to an automated system. You need a steady hand. Our Morgan Financial loan officers live and work in the same neighborhoods you’re looking to join. We know the difference between a waterfront property in Merritt Island and a suburban lot in Viera. This deep local knowledge allows us to advocate for you with a level of precision that national competitors simply cannot match.

We bring a veteran-owned perspective to every transaction. We understand that your VA Home Loan is more than a financial product; it’s a benefit you earned through service. We treat your purchase with the absolute respect it deserves. During that high-pressure 48-hour Tidewater window, we provide direct communication. You’ll have a dedicated specialist as your point of contact. We don’t hide behind layers of bureaucracy. We act with high-energy efficiency to ensure your data is submitted correctly and on time. We are neighbors helping neighbors. We take personal responsibility for your success.

Beyond Pre-Approval: Our Commitment to Closing

Our work begins long before the appraiser visits the property. We proactively manage the appraisal process by setting clear expectations with all parties involved. This preparation often prevents Tidewater issues from arising in the first place. We encourage you to See our "Stronger Than a Pre-Approval" program to understand how we position your offer for success. Our established relationships with local appraisers and real estate agents ensure smooth, professional communication. We bridge the gap between technical requirements and positive emotional outcomes. We make the complex feel simple.

Ready to Secure Your Florida Home?

Don’t let the fear of a low appraisal stop you from utilizing your hard-earned benefits. The VA loan program remains one of the most powerful tools for building wealth. With the right team behind you, even a Tidewater notification is just a temporary hurdle. Contact our Melbourne-based team today to discuss your goals. We are ready to provide the effortless expertise you need to cross the finish line. Start your VA loan journey with Morgan Financial and experience the difference that local dedication makes. We are ready when you are.

Take Command of Your Space Coast Home Purchase

Your journey to homeownership in Brevard County shouldn’t be derailed by a single appraisal report. You now understand that the 48-hour window is a powerful tool for your protection. It’s a second chance. It’s a strategic pause. It’s a path to victory. By providing precise local data and acting with high-energy efficiency, you can turn a low valuation into a successful closing. Understanding what is the VA Tidewater Initiative gives you the confidence to stay in the game and ensures your hard-earned benefits work exactly as intended.

We’re here to lead the way as your local specialists. Morgan Financial has been veteran-owned and operated since 2002. We’re dedicated specialists in Florida VA lending with a local office right here in Melbourne, FL. We don’t just process loans; we advocate for our neighbors. Our team provides the steady hand you need in a complex market. We handle the technical details while you focus on the excitement of your new home. Experience the difference that local expertise and professional confidence can make for your family.

Ready to move forward? Start Your VA Loan with a Local Veteran-Owned Expert and secure your future today. We’re ready to help you win.

Frequently Asked Questions

Does the VA Tidewater Initiative mean my loan is denied?

No, a Tidewater alert is not a loan denial. It is a proactive safety measure. It signals that the appraiser needs more data to support the contract price. This process gives you a 48-hour window to provide better evidence before a final value is set. It’s an opportunity. It’s a shield. It’s a second chance.

Who can provide the comparable sales during the Tidewater process?

The real estate agents involved in the transaction provide the data. Once the appraiser notifies the lender, the buyer’s and seller’s agents collaborate to find the strongest comps. These must be submitted to the lender’s point of contact within two business days. Fast. Reliable. Expert. This teamwork is what keeps your deal moving forward.

Can I pay the difference if the Tidewater Initiative doesn’t raise the value?

Yes, you can choose to pay the difference out of pocket if the final valuation still falls short. The VA allows veterans to cover an appraisal gap with their own funds. However, you should never feel pressured to overpay. We help you analyze the data so you can make an informed, confident decision about your investment and your future.

How often does the Tidewater Initiative actually work?

Success depends heavily on the quality of the data provided by your real estate team. While specific national percentages fluctuate yearly, this protocol successfully resolves many valuation issues before they become permanent. Understanding what is the VA Tidewater Initiative and how to use it effectively is often the difference between a closed loan and a cancelled contract.

What if there are no good comparable sales in my neighborhood?

Your team may need to look slightly further out or at slightly older sales if your immediate area lacks data. The appraiser will consider these secondary comps if they are logically explained in the narrative. If no data exists to support the price, you may need to renegotiate the contract or consider a formal Reconsideration of Value later.

Is the seller required to lower the price if Tidewater fails?

No, the seller is not legally obligated to reduce their price. If the appraisal comes in low and Tidewater doesn’t fix it, the transaction enters a new negotiation phase. You can ask for a price reduction, meet in the middle, or walk away with your earnest money protected by the mandatory VA amendatory clause.

Can I request a second appraisal if I am unhappy with the Tidewater outcome?

Requesting a new appraisal is rarely permitted under VA rules. You cannot simply appraisal shop because you dislike the number. Your primary recourse is the Reconsideration of Value (ROV) process. This allows you to challenge the existing report based on factual errors or overlooked data through official channels with the help of your lender.

How does Tidewater affect my closing date in Florida?

The process adds at least two business days to your timeline. In the fast-paced Florida market, this minor delay is a small price to pay for protecting your equity. We work with high-energy efficiency to ensure this pause doesn’t cause a domino effect on your move-in date. We keep the process brisk. We keep it logical. We keep it on track.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.