Over 1.5 million veterans call the Sunshine State home, yet many remain unaware that a 5% down payment can reduce their upfront costs from 2.15% to 1.50% for first time users of their VA loan benefits. Mastering the 2026 VA loan funding fee Florida requirements is the first step toward securing your piece of the Space Coast without unnecessary expenses. You’ve earned these benefits through service. You deserve a mortgage process that is transparent, high-energy, and completely streamlined. Fast. Reliable. Local.

We understand the frustration of tracking shifting percentage rates and the concern over rolling extra costs into your loan balance. It’s a lot to handle, but you don’t have to do it alone. This guide will help you master the 2026 fee tiers and discover the specific ways to minimize or waive this cost entirely. Our VA Loan Specialists are here to ensure you move forward with professional confidence and regional expertise.

We will provide a clear calculation of your 2026 fees, verify your exemption status, and outline a payment strategy that fits your unique financial goals. Your path to homeownership starts with the right information.

Key Takeaways

- Understand why this one-time fee is a strategic reinvestment that secures your right to a no-down-payment home in Florida.

- Calculate your exact 2026 VA loan funding fee Florida costs and see how a 5% down payment acts as a “sweet spot” for savings.

- Determine your exemption status immediately to see if disability ratings or service honors allow you to waive the fee entirely.

- Evaluate the long-term benefits of paying the fee at closing versus financing it into your total loan balance for your Brevard County home.

- Leverage the expertise of a veteran-owned local guide to navigate the technical requirements of the VA program with speed and reliability.

What is the VA Loan Funding Fee and Why is it Required?

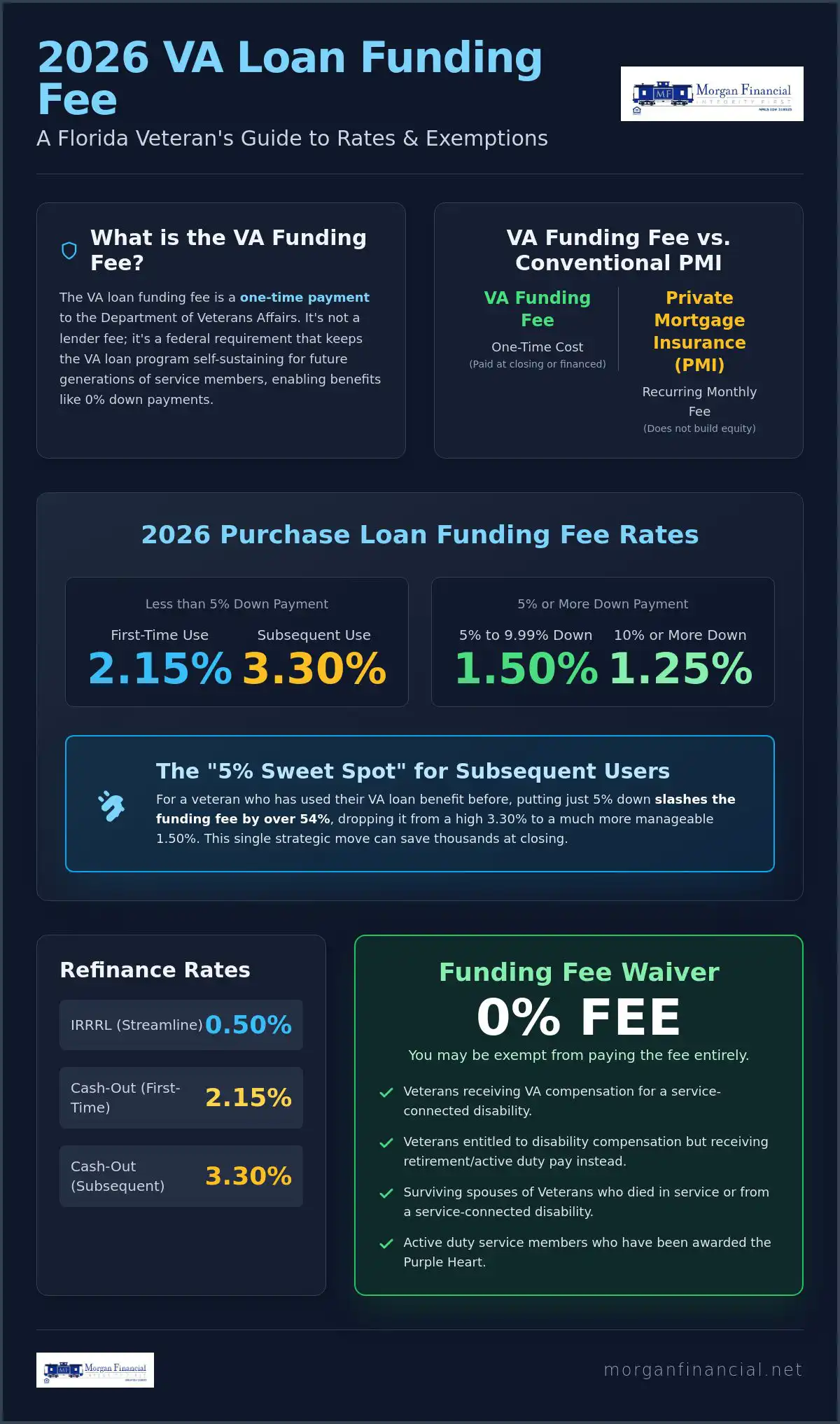

The VA loan funding fee Florida is a one-time administrative payment required by the Department of Veterans Affairs. It isn’t a lender profit-center or a "junk fee" tacked on by a bank. It’s a federal requirement designed to keep the program healthy and functional. This fee ensures the VA loan program remains self-sustaining for the next generation of service members. By contributing this amount, you help preserve the benefit for your fellow veterans across the Space Coast. What is the VA Loan Funding Fee? It is a collective reinvestment into a program that empowers veterans to achieve homeownership without the traditional barriers of high down payments or expensive mortgage insurance.

Think of this fee as the price of admission to the most powerful mortgage product on the market. It’s a small trade-off for the massive flexibility you receive in return. This isn’t about red tape. It’s about reliability. It’s about security. It’s about your future. We focus on making this process clear so you can move forward with confidence. Fast. Reliable. Local.

The Mechanism: How Your Fee Backs the VA Guaranty

The VA provides a 25% guaranty to lenders like Morgan Financial. This backing is the reason we can offer 0% down payment options in Melbourne, Palm Bay, Viera and throughout Brevard County. Without this safety net, lenders would require significant cash upfront to mitigate risk. The funding fee is the engine behind the VA’s competitive interest rates and flexible credit requirements. It provides the financial stability needed to keep the program running at peak efficiency. It’s the mechanism that turns your military service into a tangible financial advantage.

VA Funding Fee vs. Conventional PMI

On a conventional loan, if you put down less than 20%, you are forced to pay Private Mortgage Insurance (PMI) every month. These payments don’t build equity. They simply protect the lender. The VA fee is different because it’s a "one and done" cost. You pay it once at closing or roll it into your loan balance. You’ll never see a monthly insurance premium on your VA mortgage statement. For most Florida homebuyers, the funding fee is significantly cheaper than the lifetime cost of conventional monthly premiums. You can explore more about these advantages on our VA Home Loans Resource page. It’s a smarter way to borrow. It’s a faster way to build wealth. It’s a better way to buy.

2026 VA Funding Fee Rates for Florida Homebuyers

Clarity is the foundation of a confident home purchase. When you calculate your VA loan funding fee Florida, remember that the percentage is applied to the total loan amount, not the sales price of the home. If you choose to roll the fee into your mortgage, your total balance will increase, which slightly impacts your monthly payment and long-term interest. Understanding these specific tiers allows you to plan with precision. Professional. Transparent. Effective.

The Department of Veterans Affairs updated the 2026 VA Funding Fee Rates to ensure the program remains robust for everyone. Whether you are buying your first home in Melbourne or upgrading to a larger property in Palm Bay, these numbers dictate your upfront costs. Our team focuses on high-energy efficiency to get these calculations right the first time so there are no surprises at the closing table.

Purchase Loan Rate Chart for 2026

The difference between "First-Time Use" and "Subsequent Use" is a major factor for Florida veterans. If you’ve used your VA entitlement before and didn’t dispose of the previous property or restore your entitlement, you fall into the subsequent use category. However, a strategic down payment can level the playing field. Use this breakdown to see how your down payment affects your costs:

- First-Time Use (Less than 5% down): 2.15%

- Subsequent Use (Less than 5% down): 3.30%

- 5% to 9.99% Down Payment: 1.50% (Same for first or subsequent use)

- 10% or More Down Payment: 1.25% (Same for first or subsequent use)

Notice the "5% sweet spot." For a subsequent user, putting 5% down slashes the fee from 3.30% to 1.50%. This single move can save you thousands of dollars in Brevard County’s competitive market. It’s a logical, simple way to keep more equity in your pocket from day one.

Refinance Rates: IRRRLs and Cash-Out Options

Refinancing your current Florida home follows a different set of rules. If you are simply looking to lower your interest rate, the Interest Rate Reduction Refinance Loan (IRRRL) carries a flat 0.50% funding fee. It is the most cost-effective way to improve your financial position. For those looking to pull equity out for home improvements or debt consolidation, Refinance Loans involving cash-out carry higher rates. A first-time cash-out refinance sits at 2.15%, while subsequent cash-out transactions move to 3.30%.

Every veteran’s situation is unique, and your specific service history may qualify you for further reductions. If you want to see how these 2026 rates apply to your specific goals, reach out to a local specialist for a personalized breakdown.

Who is Exempt from the VA Funding Fee in Florida?

The prospect of a $0 funding fee is a reality for many Florida veterans. This waiver can save you thousands of dollars at the closing table, making homeownership even more accessible across the Space Coast. We believe in maximizing every benefit you’ve earned through your service. Accurate. Efficient. Transparent. While most borrowers anticipate this cost, specific groups are legally exempt from the VA loan funding fee Florida requirements. This includes veterans with service-connected disabilities, active-duty Purple Heart recipients, and surviving spouses of veterans who died in service or from a service-connected disability.

Your Certificate of Eligibility (COE) acts as the "Golden Ticket" for fee exemption. This document tells your lender exactly where you stand regarding the VA Funding Fee Rates. Before your loan moves to underwriting in Melbourne or Palm Bay, follow this 3-step checklist to verify your status:

- Access your eBenefits or VA.gov account to pull your most recent COE.

- Locate the "Funding Fee" section on the document to see if you are listed as exempt.

- If the status is "Non-Exempt" but you have a pending disability claim, notify your lender immediately.

Disability Ratings and the Purple Heart Waiver

A disability rating of 10% or higher generally grants you a full waiver of the VA loan funding fee Florida. This applies whether you are a first-time homebuyer or a subsequent user. Additionally, the 2026 rules confirm that active-duty service members who have been awarded the Purple Heart are exempt from this cost. We make it our mission to ensure these details are verified early in the process. We don’t just process loans; we protect your benefits. You can find more details on our VA loan resource page. It’s about professional standards and local pride.

The Pending Claim: How to Get a Funding Fee Refund

What happens if your disability claim is still stuck in the system when you close on your home? This is a common point of confusion for veterans in Brevard County. If the VA awards you disability compensation retroactively to a date that precedes your loan closing, you are eligible for a full refund of the fee. You shouldn’t worry about losing that money forever.

You must work closely with your regional specialist to track your claim status. If the award letter arrives after your closing date, you can submit a request through the VA for a reimbursement of the amount paid or financed. There are specific time limits for these filings, so acting with speed is essential. We stay by your side through this process to ensure you get every dollar back. Brisk. Logical. Intentional.

Strategic Ways to Pay the Fee in the Brevard County Market

Deciding how to handle the VA loan funding fee Florida is a strategic choice that impacts your monthly budget and long-term equity. You have options. You have flexibility. You have a team ready to crunch the numbers. Most buyers in Melbourne and Palm Bay choose to finance the fee, but savvy investors often look toward seller concessions to keep their loan balance low. Our goal is to provide the effortless expertise you need to make the right call for your family’s future. Precise. Efficient. Reassuring.

We see two primary paths for Florida homebuyers. You can pay the fee upfront as a closing cost or roll it into the total loan amount. There is no one-size-fits-all answer. The right choice depends on your current cash reserves and your long-term financial goals for your Space Coast property. We work with you to analyze the interest impact and equity growth of each scenario. Fast. Reliable. Local.

Financing the Fee: Pros, Cons, and Long-Term Costs

Data shows that approximately 90% of VA borrowers choose to roll the funding fee into their loan. This strategy preserves your liquid cash for moving expenses, new furniture, or home upgrades. On a typical Melbourne home loan, financing the fee might only add between $15 and $30 to your monthly mortgage payment. It is a logical way to keep your initial investment at a minimum while still securing a premium interest rate. This Funding fee is a closing cost, but there are closing costs other than the funding fee. The other closing costs can not be rolled into a VA loan.

However, financing the fee does mean you are paying interest on that amount for the life of the loan. If you plan to stay in your home for thirty years, that small monthly increase adds up. If you have the extra capital available, paying the fee in cash at the closing table keeps your loan balance lower and your equity higher from day one. We help you weigh these monthly savings against your immediate cash needs to find the perfect balance.

Using Florida Seller Concessions to Cover Your Fee

Brevard County is a competitive market, but the VA program offers a powerful tool for buyers. The VA allows sellers to contribute up to 4% of the total loan amount toward your closing costs and the funding fee. This is a game-changer for veterans who want to buy a home with truly zero out-of-pocket costs. In the current Space Coast landscape, we frequently see successful offers that include these concessions.

To make this strategy work, your offer needs to be undeniable. Presenting a Stronger Than a Pre-Approval letter gives sellers the confidence they need to accept an offer with concessions. This high-achieving approach positions you as a reliable buyer who is ready to close quickly. Additionally, some borrowers may benefit from a "Lender Credit," where the lender covers a portion of the fee in exchange for a slightly different interest rate.

Every dollar counts when you are building a life in Florida. If you want to explore which payment strategy maximizes your benefits, contact our regional specialists today for a personalized loan scenario.

Navigating VA Costs with a Veteran-Owned Florida Lender

Choosing the right partner for your home purchase is about more than just finding a low rate. It is about working with someone who understands the weight of your service. We are a veteran-owned lender. We speak the language of your benefits. We know the 2026 VA loan funding fee Florida guidelines because we live them every day. This isn’t just business for us. It’s a commitment to our neighbors. Professional. Confident. Human.

National call centers often treat the VA program like a secondary product. To us, it is the gold standard. Our team focuses on high-energy efficiency to ensure you never miss a deadline in the fast-moving Florida market. We eliminate the anxiety of the lending process by providing a streamlined, logical path to the closing table. You deserve a steady hand in this complex landscape. Fast. Reliable. Local.

The Space Coast Specialist Advantage

Local knowledge is your greatest asset when buying property in Brevard County. Since 2002, we have built deep roots in this community. From the historic streets of Titusville to the quiet shores of Melbourne Beach, we understand the specific nuances of the Space Coast market. This regional authority matters when it comes to VA appraisals and fee verifications. We have the local connections necessary to resolve issues quickly, often walking directly into local offices to get the answers you need.

Your Next Steps: COE Verification and Pre-Approval

You don’t have to guess about your costs or your eligibility. Your first step is to gain total clarity on your budget. Use our Mortgage Calculator to estimate your potential fee and monthly payments. This tool provides an immediate, practical look at how different loan scenarios fit your long-term goals. Inspiration followed by action.

Once you have a baseline, our team can pull your Certificate of Eligibility (COE) in minutes. This document is the only way to officially confirm your VA loan funding fee Florida status and any potential exemptions. We move quickly to verify your benefits so you can shop for a home with absolute confidence. Don’t let confusion over percentage rates hold you back from the home you’ve earned. Contact Morgan Financial today for a personalized VA cost breakdown and experience the overachiever difference.

Take Command of Your Florida Home Purchase

Don’t let technical details slow you down. We are here to pull your COE, verify your savings, and guide you home with professional confidence. Calculate your VA loan savings with a local Space Coast expert at Morgan Financial. Your new chapter in the Sunshine State is waiting. We are ready to help you secure the future you’ve earned.

Frequently Asked Questions

Is the VA funding fee different in Florida than other states?

No, the VA funding fee Florida residents pay is the same as in any other state because it is a federal requirement. While property taxes and insurance vary locally, the VA sets these percentage rates on a national level. You can count on the same standard tiers whether you are buying on the Space Coast or across the country. Reliable. Consistent. Fair.

Can I include the VA funding fee in my total loan amount?

Yes, you can roll the entire funding fee into your total loan balance. Most borrowers choose this option to minimize their upfront cash requirements. It increases your total mortgage amount and monthly payment slightly, but it allows you to keep your savings intact for other expenses. Efficient. Logical. Intentional.

How do I know if I am exempt from the VA funding fee?

Your Certificate of Eligibility (COE) is the definitive source for your exemption status. If you receive VA disability compensation for a service-connected condition, you are typically exempt. Purple Heart recipients and certain surviving spouses also qualify for a full waiver. We pull this document for you in minutes to provide instant clarity. Precise. Fast. Reassuring.

What happens to the funding fee if I sell my home after two years?

The funding fee is a one-time, non-refundable payment made at the time of closing. If you sell your home after two years, you don’t receive a partial refund or credit. However, the fee has already served its purpose by allowing you to secure a no-down-payment loan with competitive interest rates. It is a sunk cost of the transaction.

Is the VA funding fee tax deductible in 2026?

Tax laws change frequently, and you should always consult with a qualified tax professional regarding your specific situation. Generally, the VA funding fee is not considered a deductible expense under federal guidelines for 2026. However, your individual circumstances or Florida-specific property tax exemptions for disabled veterans may offer other significant financial benefits. Professional. Transparent. Honest.

Can a seller pay my VA funding fee in Florida?

Yes, Florida sellers can contribute up to 4% of the total loan amount toward your closing costs, which includes the funding fee. This is a powerful strategy in the Brevard County market to reduce your out-of-pocket expenses. We help you structure offers that leverage these concessions to maximize your military benefits. Brisk. Strategic. Effective.

How much is the VA funding fee for a second-time homebuyer?

For a second-time user with a 0% down payment, the 2026 fee is 3.30% of the loan amount. You can reduce this rate to 1.50% by making a 5% down payment. This "subsequent use" rate applies if you have used your VA loan benefit previously and don’t qualify for an exemption. Logical. Simple. Smart.

Do I have to pay the funding fee on a VA IRRRL refinance?

Yes, but the rate is significantly lower for an Interest Rate Reduction Refinance Loan (IRRRL). The fee is fixed at 0.50% of the new loan amount. This makes the IRRRL the most affordable way to lower your interest rate or move from an adjustable-rate to a fixed-rate mortgage. Fast. Reliable. Local.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.