Did you know that Florida is home to over 1.5 million veterans, yet many still walk into closing day blindsided by a five-figure charge? It’s a common story. You find the perfect property in Brevard County, start the paperwork, and suddenly face a significant VA loan funding fee Florida cost that wasn’t in your initial budget. We’re here to change that. Fast. Reliable. Local. We believe your path to homeownership on the Space Coast should be transparent, efficient, and rewarding.

You’ve served your country, and you deserve a lending process that respects your sacrifice without the stress of unexpected expenses. We’ll help you master the 2026 VA funding fee requirements, explore Florida-specific exemptions for disabled veterans, and learn how to minimize your out-of-pocket closing costs. This guide breaks down the updated 2.15% first-time and 3.3% subsequent use rates while showing you exactly how to roll the fee into your loan. Get ready for a clear, logical, and efficient look at your 2026 home buying strategy.

Key Takeaways

- Understand how this one-time administrative fee replaces monthly mortgage insurance, keeping your long-term homeownership costs predictable.

- Confirm your eligibility to potentially waive the VA loan funding fee Florida entirely through disability-related or surviving spouse exemptions.

- Compare the 2026 rate differences between first-time and subsequent use to plan your down payment strategy effectively.

- Navigate unique Space Coast closing requirements, including Florida-specific documentary stamps and intangible taxes on your loan.

- Discover why partnering with a local, veteran-owned lender ensures a streamlined and highly personalized experience in Brevard County.

What is the VA Funding Fee and Why is it Required?

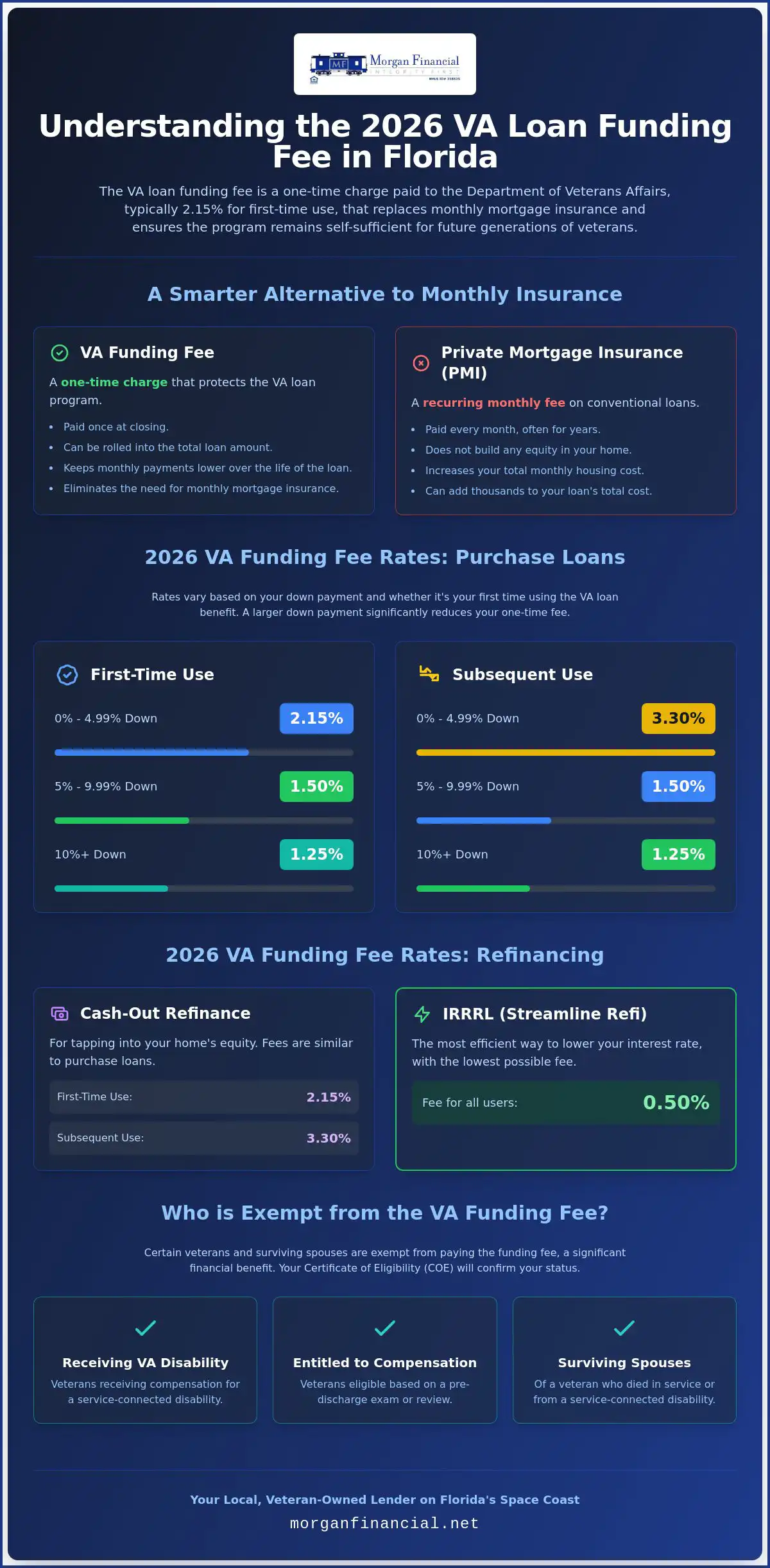

The VA loan funding fee Florida is a one-time administrative cost paid directly to the Department of Veterans Affairs. It serves a vital purpose. It protects the program. It ensures future generations of heroes can access zero-down financing. Think of it as the engine that drives the most powerful mortgage product on the market. This fee is the reason the federal government can guarantee your loan without requiring a massive budget from taxpayers. It’s a collective pool that keeps the benefit sustainable for every veteran who follows in your footsteps.

This cost applies to both purchase loans and VA cash-out refinancing across the Sunshine State. The VA loan program was established to provide long-term financing to eligible American veterans, and this fee is the primary way the program remains self-sufficient. You have flexibility in how you handle this requirement. You can pay the entire amount upfront at the closing table, or you can choose to roll the fee into your total loan balance. Most Space Coast veterans choose the latter to keep their initial out-of-pocket expenses as low as possible. It’s a simple, strategic choice that preserves your cash for what matters most.

The VA Funding Fee vs. Private Mortgage Insurance (PMI)

Conventional buyers with less than 20% down are almost always hit with Private Mortgage Insurance. This is a recurring monthly cost. It never builds equity. It simply disappears into the lender’s pocket. The VA funding fee is different. It’s a one-time charge that replaces the need for monthly PMI entirely. For a homeowner in Brevard County staying in their property for five years or more, the savings are substantial. You avoid the monthly drain. You build equity faster. You enjoy a lower total monthly payment. If you want to see how these numbers impact your specific budget, explore our VA loan resource page for deeper insights.

Who is Responsible for Paying the Fee?

Responsibility for the fee falls on the borrower. This includes veterans, active-duty service members, and eligible National Guard or Reserve members. While the borrower is technically responsible, the Florida real estate market offers creative ways to manage the cost. We often see savvy buyers negotiate seller concessions to cover closing costs, which can include this fee. Our team works with you to ensure your offer is competitive while protecting your financial interests. We provide the steady hand you need. We offer the local expertise you deserve. We make the process transparent, efficient, and rewarding from start to finish.

2026 VA Funding Fee Rates: A Breakdown for Florida Borrowers

Success in the Florida real estate market requires precision. For 2026, the VA loan funding fee Florida percentages are clearly defined. If you’re using your benefit for the first time with less than a 5% down payment, your rate is 2.15% of the total loan amount. This is the standard entry point for most Space Coast veterans. These rates are federal. They apply whether you’re buying a beachside bungalow in Melbourne or a family home in Titusville. Accuracy matters here. Knowing these numbers upfront helps you calculate your buying power with total confidence.

Many veterans are surprised to see the rate jump for subsequent use. If you’ve used your VA home loan benefit before, the fee increases to 3.3% for a zero-down purchase. Subsequent use is defined as any VA-backed loan after your initial purchase or refinance has closed. The Department of Veterans Affairs sets these higher rates to ensure the program remains robust for the long haul. You aren’t stuck with the 3.3% rate if you have cash on hand. You can actively lower your costs by putting money down. A 5% down payment drops your fee to 1.5%. A 10% down payment slashes it further to 1.25%. If you’re unsure which tier fits your budget, reach out to our Space Coast team for a personalized breakdown.

While most borrowers will pay these standard rates, certain individuals may qualify for VA Funding Fee Exemptions based on service-connected disabilities or other specific criteria. We’ll dive deeper into those exemptions in the next section, but always keep your Certificate of Eligibility (COE) ready to verify your status. Our goal is to make your transition into a new home as smooth as possible. We provide the expertise. We offer the speed. We deliver the results you expect.

Funding Fees for VA Cash-Out Refinancing

Equity is a powerful tool. If you’re looking to tap into your home’s value for renovations or debt consolidation, a VA Cash-Out Refinance is a strategic move. In 2026, these transactions carry the same fee structure as purchase loans: 2.15% for first-time use and 3.3% for subsequent use. This is higher than a simple rate reduction, but it reflects the increased administrative scope of a cash-out transaction. We guide you through this process with speed and reliability. We ensure you maximize your equity while minimizing your costs.

The IRRRL Exception: Lower Fees for Streamline Refinancing

The Interest Rate Reduction Refinance Loan (IRRRL) is the gold standard for efficiency. It’s often called a VA Streamline. This option carries the lowest fee in the entire program at just 0.5%. This is the preferred choice for Florida veterans who want to lower their monthly payment without the heavy lifting of a full appraisal or extensive credit underwriting. It’s fast. It’s simple. It’s effective. Check your current interest rate against the 2026 market trends to see if an IRRRL can put more money back in your pocket every month.

VA Funding Fee Exemptions: Who Doesn’t Have to Pay?

While the rates we discussed previously are standard for many, a significant number of Space Coast heroes find they don’t owe a dime. The VA loan funding fee Florida requirement isn’t universal. Exemptions exist to honor your service and your sacrifice. If you fall into a specific category, you can bypass this cost entirely. This isn’t just a discount. It’s a complete waiver. It’s a benefit you’ve earned through your dedication to our country.

The primary group eligible for an exemption includes veterans receiving compensation for a service-connected disability. This is the most common way to waive the fee. However, the list doesn’t end there. Surviving spouses who receive Dependency and Indemnity Compensation (DIC) are also exempt from paying. Additionally, active-duty service members who have been awarded the Purple Heart do not have to pay the fee. For those currently transitioning out of the military, a "proposed or memorandum rating" can serve as vital proof of future disability status. This allows you to secure the exemption before your final discharge papers are even signed. You can find the Official VA funding fee rates and full exemption criteria on the VA’s site to confirm your specific situation.

Pending Disability Claims and Retroactive Refunds

Timing is everything in real estate. Sometimes, your disability claim is still in the works when you head to the closing table. If your claim is approved after your loan closes, and the effective date of the rating is before your closing date, you’re entitled to a refund. Don’t leave that money on the table. Follow this simple process to get your funds back:

- Secure your rating: Obtain your official award letter from the VA confirming the effective date.

- Notify your lender: Contact your loan officer or servicer to initiate the refund request.

- Submit documentation: Provide a copy of your rating letter and your final Closing Disclosure.

Always keep a digital copy of your Closing Disclosure. It’s the essential piece of evidence for any refund application. We help you navigate this paperwork with ease. We provide the steady hand you need during the transition.

Verifying Your Status with the Certificate of Eligibility (COE)

Your Certificate of Eligibility is the only document that truly matters here. It’s the official proof of your entitlement and your exemption status. Without it, lenders are required by law to charge the fee. We recommend visiting our VA Loan Resource center to understand how this document impacts your buying power. Morgan Financial can often pull a COE for veterans in minutes. It’s fast. It’s simple. It’s accurate. We handle the technical details so you can focus on choosing the right neighborhood in Brevard County.

The Florida Factor: Managing Closing Costs in Brevard County

Buying a home in the Sunshine State involves more than just the purchase price. You face unique state taxes. You deal with documentary stamps on the note. You pay intangible taxes. The VA loan funding fee Florida integrates into this broader financial landscape, and it’s essential to see how these costs interact. In the competitive 2026 markets of Melbourne and Palm Bay, understanding these line items upfront is your greatest advantage. We ensure there are no surprises at the closing table. Our process is transparent, logical, and efficient.

Florida charges a documentary stamp tax on all promissory notes at a rate of $0.35 per $100 of the loan amount. Additionally, you’ll encounter a non-recurring intangible tax of $0.002 per dollar on the total mortgage amount. While these might seem like small percentages, they add up quickly on a standard Space Coast mortgage. We help you calculate these specific Florida expenses alongside your funding fee so you can walk into your new home with total financial clarity. We provide the steady hand you need in a complex market.

Strategic Use of Seller Concessions on the Space Coast

Seller concessions are a powerful tool for veterans in Brevard County. The VA allows sellers to pay all normal and customary closing costs (as deemed by the VA) as well as contribute up to 4% of the total purchase price toward "sales concessions". Remember, this does have to be negotiated into your sales contract. This isn’t just for traditional title fees. You can negotiate for the seller to pay your entire funding fee upfront. This keeps your loan balance lower. It saves you money over the life of the mortgage. It preserves your hard-earned cash. When making an offer in a high-demand area, we suggest balancing your request for credits with a competitive purchase price. This makes your offer stand out to sellers while still protecting your bottom line. Talk to our local experts to craft a winning offer strategy today.

High-Value Homes and Jumbo VA Loans in Brevard

Brevard County features incredible high-value properties, especially in beachside communities. If you’re looking at Satellite Beach or Indialantic, you might be considering a loan amount that exceeds traditional conforming limits. For veterans with full entitlement, those limits no longer exist. You can secure a jumbo-sized VA loan with zero down payment. The funding fee scales with these larger amounts, making it even more important to verify your exemption status or plan for the cost. Partnering with the best home loan lenders in FL ensures you have the specialized knowledge required for high-balance transactions. We provide the expertise. We deliver the reliability. We secure your future on the Space Coast.

Why a Local Veteran-Owned Lender Makes the Difference

Choosing the right partner for your home purchase is a strategic decision. You need more than a lender. You need a regional specialist who understands the Space Coast terrain. Morgan Financial is a veteran-owned and operated firm. We don’t just process loans; we live and work in the same communities you’re looking to call home. This shared background creates a level of trust and accountability you won’t find at a national call center. We handle every detail of the VA loan funding fee Florida with total transparency. No hidden surprises. No bureaucratic delays. Just professional confidence.

National lenders often struggle with the nuances of Florida real estate law. They might miss the specific calculations for documentary stamps or intangible taxes required in our state. Our local team moves with high-energy efficiency. We know the local appraisers. We understand the Brevard County title requirements. We provide the steady hand needed to navigate a complex financial landscape. You deserve a partner who is pleasant, human, and highly capable. We deliver that expertise every single day. We are faster. We are more efficient. We are committed to your success.

The "Stronger Than a Pre-Approval" Advantage

In the competitive 2026 market, a standard pre-approval isn’t enough. You need the Stronger Than a Pre-Approval advantage. This isn’t a simple credit check. It’s a fully underwritten commitment. Our underwriters review your file upfront, which includes a precise calculation of your VA loan funding fee Florida and total closing costs. This gives you a massive edge in multi-offer situations. Sellers in Melbourne and Palm Bay prioritize offers backed by our reputation for reliability. You walk into the negotiation with the strength of a cash buyer. It’s a logical, streamlined, and intentional way to secure your home.

Ready to Start Your Space Coast Home Search?

Your mission to own a home on the Space Coast starts now. Don’t leave your financial future to guesswork or a detached national corporation. Use our Mortgage Calculators to estimate your monthly payments and potential funding fees today. Once you’re ready for a personalized strategy, Contact Morgan Financial to speak with a dedicated specialist. We’ll help you maximize your benefits, confirm your exemption status, and minimize your out-of-pocket costs. We take personal responsibility for the financial well-being of our neighbors.

Fast. Enjoyable. Consistent.

Secure Your Space Coast Future Today

You now possess the strategic blueprint for the VA loan funding fee Florida in 2026. You’ve mastered the rate tiers. You’ve identified your potential exemptions. You’ve learned how to turn closing costs into a manageable part of your homebuying victory. This clarity replaces anxiety with confidence. It transforms a complex process into a clear path forward. Expert. Efficient. Proven.

Your service deserves a local partner who respects your sacrifice. Morgan Financial has been veteran-owned and operated since 2002. We are Space Coast specialists. We’ve served over 2,000 local veterans with the same dedication you gave to our country. We offer the speed, reliability, and regional authority you won’t find at a national call center. Get Your Personalized VA Loan Quote from Morgan Financial to start your next chapter. Your new home is waiting, and we’re ready to help you claim it.

Frequently Asked Questions

Is the VA funding fee tax deductible in Florida in 2026?

No, the funding fee is generally not tax deductible for the 2026 tax year. While mortgage insurance premiums were deductible in the past under specific legislative extensions, the VA funding fee is currently treated as a cost of the loan rather than deductible interest. You should always consult with a qualified tax professional regarding your specific financial situation in Brevard County. We provide the technical data you need for those conversations. Accurate. Professional. Detailed.

Can I pay the VA funding fee in cash instead of financing it?

Do National Guard members pay a higher VA funding fee than active duty?

No, National Guard and Reserve members now pay the exact same funding fee rates as active-duty service members. This parity was established to honor the service of all components equally. Whether you serve full-time or in the reserves, your 2026 rates are based solely on your down payment amount and whether it’s your first or subsequent use of the benefit. We treat every hero with the same high-energy efficiency. Reliable. Fair. Local.

What happens to the funding fee if I sell my home after two years?

The funding fee is a one-time, non-refundable charge paid at closing. If you sell your home in Melbourne or Palm Bay after two years, you do not receive a pro-rated refund of the fee. However, the benefit of avoiding monthly mortgage insurance during those two years often outweighs the cost of the fee itself. It’s a sunk cost that served its purpose by securing your zero-down financing. We help you look at the long-term logic.

Is the funding fee required for a VA loan assumption in Florida?

Yes, but the rate is significantly lower for an assumption. When a buyer assumes an existing VA loan, the funding fee is typically just 0.5% of the current loan balance. This makes VA assumptions an incredibly attractive option in a high-rate environment. We understand the complexities of these transactions on the Space Coast. We provide the steady hand you need to navigate the assumption process with speed and total transparency.

Can the VA funding fee be waived for a 10% disability rating?

Yes, a service-connected disability rating of 10% or higher qualifies you for a total waiver of the VA loan funding fee Florida. This is a significant financial benefit that can save you thousands of dollars at closing. Your Certificate of Eligibility must reflect this status to automate the waiver. Our team can pull your COE in minutes to confirm your exemption. It’s fast. It’s simple. It’s the least we can do for your sacrifice.

How does the funding fee change for a VA home construction loan?

The funding fee for a construction loan is the same as a standard purchase loan. For 2026, you’ll pay 2.15% for first-time use with zero down or 3.3% for subsequent use. The fee is calculated based on the total loan amount, including the costs of construction. Building your dream home in Indialantic requires precision, and we ensure your funding fee is calculated accurately from the start. We deliver results with professional confidence.

Does the funding fee apply to surviving spouses?

Generally, no. Surviving spouses who are eligible for the VA home loan benefit are typically exempt from the funding fee if they receive Dependency and Indemnity Compensation (DIC). This exemption honors the ultimate sacrifice made by your family. We handle these files with the utmost care and reassurance. We ensure you receive every benefit you’re entitled to while making the process feel human and supportive. We are here for you.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.