What if the path to your next home was already paved by the hero you loved? Securing a home after a loss shouldn’t feel like a second battle against red tape, and qualifying for a VA loan for surviving spouse in Florida shouldn’t be a source of stress. We understand the weight you’re carrying. It’s heavy, personal, and real. You want more than just a mortgage; you want a way to honor a legacy while finding financial stability in the Sunshine State.

We promise to provide total clarity on your eligibility and show you how to leverage exclusive benefits, including zero down payment options and powerful tax exemptions. This guide breaks down your eligibility, explains the $5,000 Florida widow’s exemption, and outlines how you can avoid the 2.15% funding fee entirely. Let’s turn this complex process into a clear, confident step toward your new home in Florida.

Key Takeaways

- Define your eligibility. Understand the specific service-connected death and disability requirements to claim your earned benefits.

- Save your capital. Secure a VA loan for surviving spouse Florida with zero down payment and a total exemption from the VA funding fee.

- Reduce your taxes. Learn how to qualify for Florida’s aggressive property tax exemptions, including potential 100% homestead relief.

- Win the offer. Use a “Stronger Than a Pre-Approval” to compete effectively in the fast-moving Brevard County real estate market.

Qualifying for a VA Loan as a Surviving Spouse in Florida

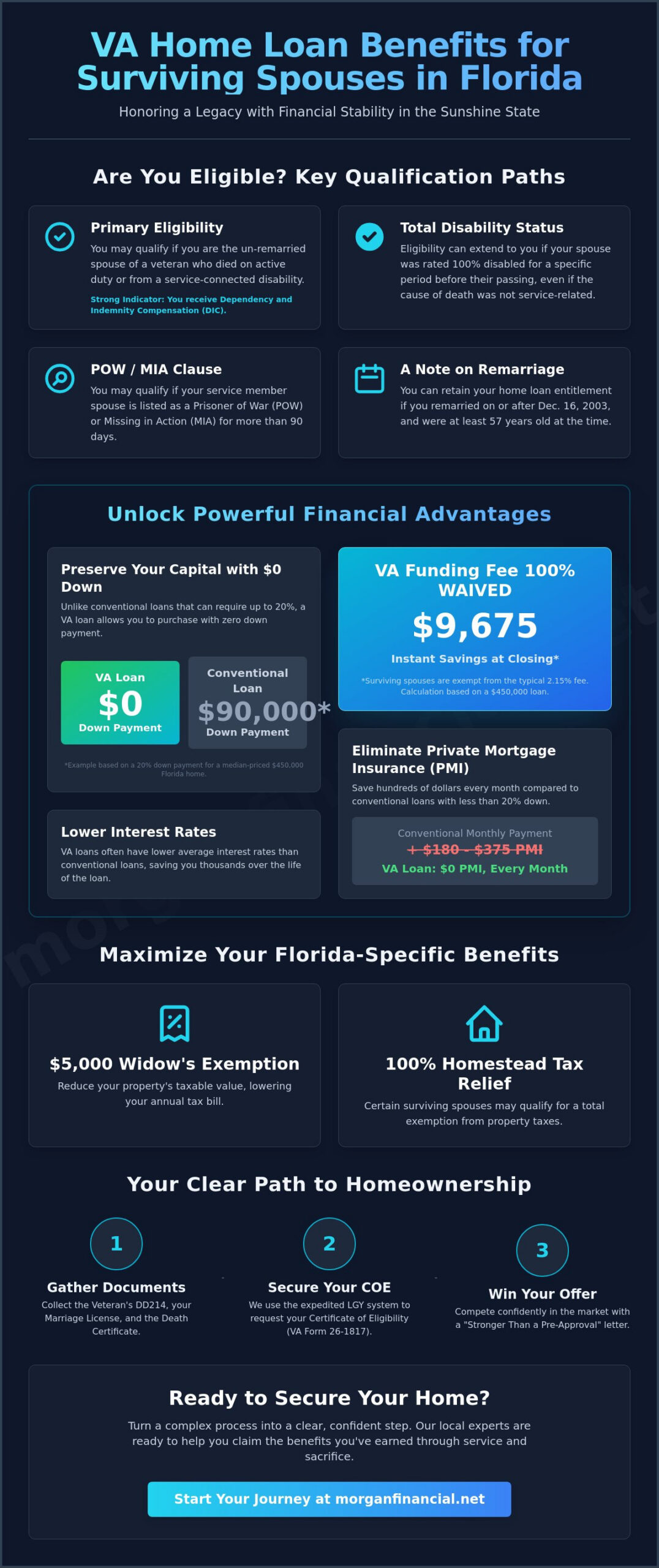

Navigating federal eligibility requirements shouldn’t feel like a solo mission during a time of transition. Florida is home to over 1.3 million veterans, and their families deserve clear, actionable answers. A VA loan for surviving spouse in Florida represents a significant financial advantage that honors a legacy while providing a stable foundation for your future. This benefit isn’t a gift; it’s a right earned through service and sacrifice. To qualify, you generally must be the un-remarried spouse of a veteran who died on active duty or from a service-connected disability.

Service-connected disability acts as the primary anchor for your eligibility. This means the VA has determined the veteran’s death resulted from an injury or illness related to their military service. Even if the cause of death was unrelated to their service, you may still qualify if your spouse was rated as totally disabled for a specific period before their passing. The VA loan program was designed to protect families in these exact scenarios. If you currently receive Dependency and Indemnity Compensation (DIC), it’s a strong indicator that you meet the core requirements for this benefit.

Remarriage is a common point of confusion, but the rules are specific. If you remarried on or after December 16, 2003, and were at least 57 years old at the time, you likely retain your home loan entitlement. For those who remarried before reaching age 57, the benefit is usually lost unless that marriage later ends through death or divorce. Our team acts as a steady hand in this complex landscape. We help you determine a clear “yes or no” on your status quickly.

The Certificate of Eligibility (COE) for Spouses

The Certificate of Eligibility is your gateway to the purchase of a home. For surviving spouses, this requires VA Form 26-1817 rather than the standard veteran application. You’ll need to gather the veteran’s DD214, your marriage license, and the death certificate. Don’t let the paperwork intimidate you. Our Brevard County-based team is here to help you gather whatever documents you need.

Eligibility Scenarios: MIA, POW, and Disability

Special circumstances require specialized knowledge. If your spouse was 100% disabled but passed away from other causes, you are often still eligible provided the disability rating was held for the required duration. We also assist families of those who never returned home. Under 38 U.S.C. § 3701(b)(2), the POW/MIA clause extends home loan eligibility to the spouse of any service member listed as a prisoner of war or missing in action for more than 90 days. These nuances are vital for our neighbors in Brevard County and beyond. We ensure no earned benefit is left on the table.

The Financial Advantages: Zero Down and No Funding Fees

Financial peace of mind is paramount when you’re navigating life after a loss. The VA loan for surviving spouse offers a unique path to homeownership that prioritizes your stability. Unlike conventional financing that often demands a 20% down payment to avoid penalties, this benefit allows you to purchase a home with zero money down. Savings stay put. Liquidity remains high. Your future stays secure. This isn’t just about buying a house; it’s about preserving the capital you need for daily life and long-term goals.

Beyond the lack of a down payment, VA loans consistently offer more competitive interest rates than conventional products, typically outperforming traditional market rates by 0.25% to 0.50%. These savings compound over the life of your loan, keeping your monthly overhead manageable. We provide the expert guidance you need to maximize these advantages. You can verify your specific VA eligibility for surviving spouses through official channels, but our team handles the heavy lifting to ensure every dollar of your benefit is utilized.

Understanding the Funding Fee Waiver

The VA funding fee is a one-time payment that helps sustain the program for future generations. While most veterans pay 2.15% for their first use, eligible surviving spouses are completely exempt from this cost. On a median-priced Florida home of $450,000, this waiver instantly saves you close to $10,000 in closing costs. This exemption applies whether you are looking at a new purchase or exploring refinance loans to lower your current rate. It’s a direct, high-impact financial win that rewards your family’s service.

PMI vs. VA Loan: Monthly Savings Analysis

Conventional loans usually require Private Mortgage Insurance (PMI) if you put down less than 20%. This is a monthly fee that protects the lender, not you. VA loans eliminate PMI entirely, which can save you between 0.5% and 1% of your loan balance annually. On a typical Florida mortgage, this puts hundreds of dollars back into your pocket every single month. You can use our mortgage calculators to see exactly how these savings lower your true monthly payment. If you’re ready to see what your specific savings look like, reach out to our local team today for a personalized analysis.

Maximizing Florida-Specific Benefits for Gold Star Spouses

Florida stands as a national leader in honoring the families of fallen service members. While federal benefits provide the foundation, our state-specific tax laws offer a powerful financial safety net that significantly reduces the cost of homeownership. For those utilizing a VA loan for surviving spouse Florida, these exemptions are not just perks; they are essential tools for long-term stability. By combining zero-down financing with aggressive property tax relief, you can secure a home that honors your spouse’s legacy while protecting your financial future.

The “Fallen Heroes Family Tax Relief Act” is perhaps the most significant benefit available to our neighbors in Brevard County. If your spouse died from service-connected causes while on active duty, you may qualify for a 100% homestead property tax exemption. This benefit has a massive impact on your purchasing power. When we evaluate your VA Home Loan Eligibility Requirements, the absence of a monthly property tax obligation lowers your debt-to-income ratio. This allows you to qualify for a higher loan amount or simply enjoy a much lower monthly payment compared to a conventional buyer. It turns the dream of a Space Coast home into a sustainable reality.

Florida Homestead Exemptions for Spouses

Securing these benefits requires proactive steps with the Brevard County Property Appraiser. You must file your application by the critical March 1st deadline to see the relief reflected in your current year’s taxes. Beyond the 100% exemption for Gold Star spouses, Florida residents who are widows or widowers may also claim a permanent $5,000 exemption. If you decide to move within the state, Florida’s portability laws allow you to transfer a portion of your “Save Our Homes” tax savings to a new primary residence. We guide you through these local nuances to ensure no benefit is overlooked.

Lowering Your Escrow Payments

Your monthly mortgage payment is typically comprised of PITI: Principal, Interest, Taxes, and Insurance. By qualifying for a 100% tax exemption, you effectively eliminate the “T” from that equation. This results in a significantly lower escrow requirement and more cash in your pocket every month. We work directly with you to ensure your escrow account is set up correctly from day one, reflecting your exempt status immediately. Navigating the specifics of VA home loans requires a partner who understands both federal regulations and Florida statutes. Our team acts as your steady hand, ensuring your transition into your new home is as smooth and affordable as possible.

Your Step-by-Step Path to Homeownership in Brevard County

The journey to your new front door requires a plan that works. A VA loan for surviving spouse in Florida is a powerful tool, but applying it in the competitive 2026 Space Coast market takes precision. You shouldn’t have to guess the next move or feel overwhelmed by federal requirements. We provide a clear, logical sequence to move you from eligibility to keys in hand. Our team acts as your steady hand, ensuring your offer stands out in a crowded field of buyers.

- Secure your COE: We use the LGY system to pull your Certificate of Eligibility in minutes, saving you from weeks of government back-and-forth.

- Upgrade your status: Move beyond a basic letter and get Stronger Than a Pre-Approval. This tells sellers your financing is already fully underwritten and ready to close.

- Find a Local Partner: We connect you with local real estate professionals who understand the specific nuances of surviving spouse benefits.

- Navigate the VA Appraisal: We guide you through the safety and sanitation requirements specific to Florida homes.

- Close with Care: Our process is designed to be efficient, transparent, and human, leading to a stress-free closing day.

Navigating the Space Coast Market

The 2026 real estate landscape in Cape Canaveral, Viera, and Palm Bay remains brisk. With the baseline conforming loan limit rising to $832,750 this year, you have more purchasing power than ever. Sellers in Brevard County value VA buyers when they are backed by a reputable local lender. During the appraisal process, our local expertise is vital. We look for Florida-specific items like roof age and HVAC efficiency to ensure the home meets VA Minimum Property Requirements before you commit. We protect your interests at every turn.

Closing Costs and Seller Concessions

Closing costs in Florida typically include title insurance, recording fees, and transfer taxes. However, you don’t have to carry this burden alone. VA guidelines allow you to negotiate for the seller to pay up to 4% of the purchase price in concessions. This can cover your closing costs, prepaid taxes, and even pay down existing debt. Your goal should be to combine your zero-down benefit with these concessions to keep your savings intact. If you’re ready to start your journey with a partner who cares, connect with our Space Coast specialists today.

Partnering with a Veteran-Owned Lender for Your Space Coast Home

Choosing the right partner makes all the difference when securing a VA loan for surviving spouse in Florida. Big national banks often treat you like a file in a digital queue. We don’t. As a veteran-owned firm, we understand the depth of your sacrifice and the specific requirements of your benefit better than any detached institution. Our team provides more than just a mortgage; we provide a steady hand in a complex landscape.

We are deeply rooted in the Brevard County community. This isn’t just business for us; it’s about taking care of our neighbors. Our process is designed for high-energy efficiency and professional confidence. We know that speed matters when you’re trying to secure a home in a competitive market. By pairing technical expertise with a human touch, we aim to alleviate the anxiety typically associated with lending. You’re in the hands of seasoned professionals who have mastered the local landscape.

Local Expertise, National Standards

From the historic streets of Titusville to the growing communities in Viera and our beautiful beaches, we offer personalized lending that national lenders simply can’t match. Our status as a regional specialist provides an extra layer of security for your investment. You get direct access to local advisors who understand the specific property tax codes and appraisal nuances of the Space Coast. We treat you like a neighbor because you are one.

Start Your Journey Today

Your next chapter begins with a single, confident step. We’re here to help you honor your spouse’s legacy by securing the home you deserve with the benefits you’ve earned. Whether you’re ready to buy now or just want to understand your options, we’re ready to listen. Contact our team for a compassionate, professional consultation that puts your needs first.

You can also explore our full range of purchase options to see how we serve residents across the state. Using a VA loan for surviving spouse Florida is more than a financial transaction; it’s a way to build a lasting legacy. We are committed to your success and honored to be part of your journey. Let’s find your way home together.

Step into Your New Chapter with Confidence

Honoring a legacy means securing a future where you feel supported and stable. You’ve seen how a Florida VA loan for surviving spouse provides a clear path to homeownership with zero down payment and no funding fees. By integrating Florida’s powerful property tax exemptions, you can significantly lower your monthly expenses while building equity in the Space Coast community. This process is about more than just a mortgage; it’s about claiming the rights earned through service and sacrifice.

Morgan Financial has been veteran-owned and operated since 2002. We specialize in the nuances of VA home loans and Florida tax laws to ensure you never leave an earned benefit on the table. Our team pairs deep local Brevard County expertise with national-level processing speed to provide a lending experience that is efficient, transparent, and deeply respectful. You deserve a partner who acts as a steady hand through every step of the journey.

Secure Your Future with a Veteran-Owned VA Loan Expert

Your new beginning in Florida is closer than you think. We’re ready to help you turn these benefits into a place you are proud to call home.

Frequently Asked Questions

Can I get a VA loan if my spouse died after we were married?

Yes, you can qualify if your spouse’s death resulted from a service-connected disability or if they were rated as totally disabled for a specific period before passing. This benefit honors their service by providing you with a stable home environment in the Sunshine State. We help you verify these specific details through the VA quickly. Fast. Reliable. Local.

What happens to the VA loan benefit if I remarry?

You generally retain your eligibility if you remarry at age 57 or older, provided the marriage occurred after December 16, 2003. Remarrying before this age usually terminates the benefit unless that marriage later ends through death or divorce. It’s a complex rule, but we provide the clarity you need to move forward with confidence.

Do surviving spouses pay the VA funding fee in Florida?

No, eligible surviving spouses are completely exempt from paying the VA funding fee on any purchase or refinance. This saves you thousands of dollars at closing, which is a massive advantage when securing a VA loan for surviving spouse Florida. We ensure this exemption is applied correctly from the very start of your application to keep your savings intact.

Are there specific Florida property tax breaks for surviving spouses?

Yes, Florida provides a $5,000 widow’s exemption and a potential 100% homestead tax exemption for spouses of fallen heroes. These state-level benefits drastically increase your purchasing power and lower your monthly escrow payments. We work with local property appraisers to help you maximize these significant savings in Brevard County.

How do I get a Certificate of Eligibility (COE) as a spouse?

You obtain a COE by submitting VA Form 26-1817 along with the veteran’s DD214, your marriage license, and the death certificate. Our team uses the LGY system to expedite this process for you. It’s a streamlined, logical way to get the answers you need without the bureaucratic wait.

Can I use a VA loan to refinance a home I already own?

Yes, you can use a VA loan to refinance your existing primary residence through a Cash-Out Refinance or an Interest Rate Reduction Refinance Loan (IRRRL). This allows you to lower your interest rate or access your home’s equity for necessary expenses. We analyze your current mortgage to find the most efficient path forward for your financial stability.

What credit score does a surviving spouse need for a VA loan in 2026?

While the VA doesn’t set a hard minimum, most lenders in 2026 require a credit score of 620 or higher. We look at your entire financial picture, not just a single number, to find a solution that works. Our goal is to provide a reassuring path to approval that accounts for your unique life circumstances.

Can I use the VA loan benefit more than once as a surviving spouse?

Yes, you can use your home loan entitlement multiple times throughout your life. Once you sell the previous home and pay off the loan, your full entitlement can be restored for your next Florida home purchase. This flexibility allows you to adapt as your housing needs change.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.