Your Basic Allowance for Housing isn’t just a monthly stipend for rent; it’s a strategic financial engine that carries more weight than a civilian salary twice its size. When you’re using BAH to qualify for a mortgage, you’re tapping into a unique benefit that civilian buyers simply can’t match. We know the Space Coast market is shifting. With Florida’s median home price reaching $420,000 in April 2026, finding a home near Patrick Space Force Base requires speed, precision, and local expertise.

You deserve a lender who understands the specific math of military life. Because your housing allowance is non-taxable, lenders “gross up” the income, which instantly increases your borrowing capacity. This guide shows you exactly how to leverage the 2026 BAH rates, such as the $2,883 monthly allowance for an E-6 at Patrick SFB, to secure your VA home loan. We’ll walk through the current funding fees, the impact of the 4.2 percent national increase, and how to navigate upcoming PCS dates with total confidence. Fast. Reliable. Local.

Key Takeaways

- Learn how “grossing up” your non-taxable allowance increases your buying power far beyond your base salary.

- Discover the specific requirements for using BAH to qualify for a mortgage in the 2026 Space Coast market.

- Compare current Patrick SFB housing rates against monthly mortgage costs in Melbourne and Palm Bay.

- Navigate the complexities of PCS orders and ETS dates with proven strategies for loan approval.

- Understand why a regional specialist makes the path to homeownership faster and more reliable for military families.

Understanding BAH as a Qualifying Income Source

Stability is the currency of mortgage lending. While civilian buyers often struggle to prove the consistency of their commissions or year-end bonuses, your military income is viewed as rock-solid from day one. Both VA and conventional lenders treat the Basic Allowance for Housing as stable, recurring income that is virtually guaranteed. This reliability is a massive advantage when using BAH to qualify for a mortgage on the Space Coast. It provides a level of certainty that underwriters love to see.

Verification is straightforward and efficient. You won’t need mountains of tax returns or complex profit-and-loss statements. A recent Leave and Earnings Statement (LES) is typically all a lender needs to verify your housing entitlement. This income remains constant even during deployments, providing a unique safety net that civilian salaries can’t match. If you’re preparing for a move to Melbourne or Palm Bay, this predictability allows for a faster, more confident approval process. Our VA loan specialists understand these nuances intimately. We’re fast, reliable, and local.

The Different Types of Housing Allowances

Your specific allowance type dictates your borrowing ceiling. BAH with dependents offers a higher monthly rate, which naturally boosts your maximum loan amount. If you’re receiving Overseas Housing Allowance (OHA) or Partial BAH as a member of the Reserve Component, the calculation shifts slightly. Each variation impacts your buying power differently. Understanding these distinctions is the first step toward securing a home near Cape Canaveral or Patrick SFB. When you’re using BAH to qualify for a mortgage, every dollar counts toward your final loan limit.

Why BAH is Better Than a Standard Salary

Predictability builds trust with underwriters. Military pay scales provide a clear 12-month outlook, making it easier for lenders to project your future earnings. The 4.2 percent national average increase for BAH in 2026 helps service members offset local inflation and rising home prices. BAH is a non-taxable entitlement that directly reduces your Debt-to-Income ratio. Because this money isn’t taxed, every dollar you receive goes further toward covering your principal, interest, and taxes. It’s a high-energy financial tool designed for those who serve. It turns a standard housing benefit into a powerful engine for homeownership.

How Lenders Calculate and “Gross Up” Your BAH Income

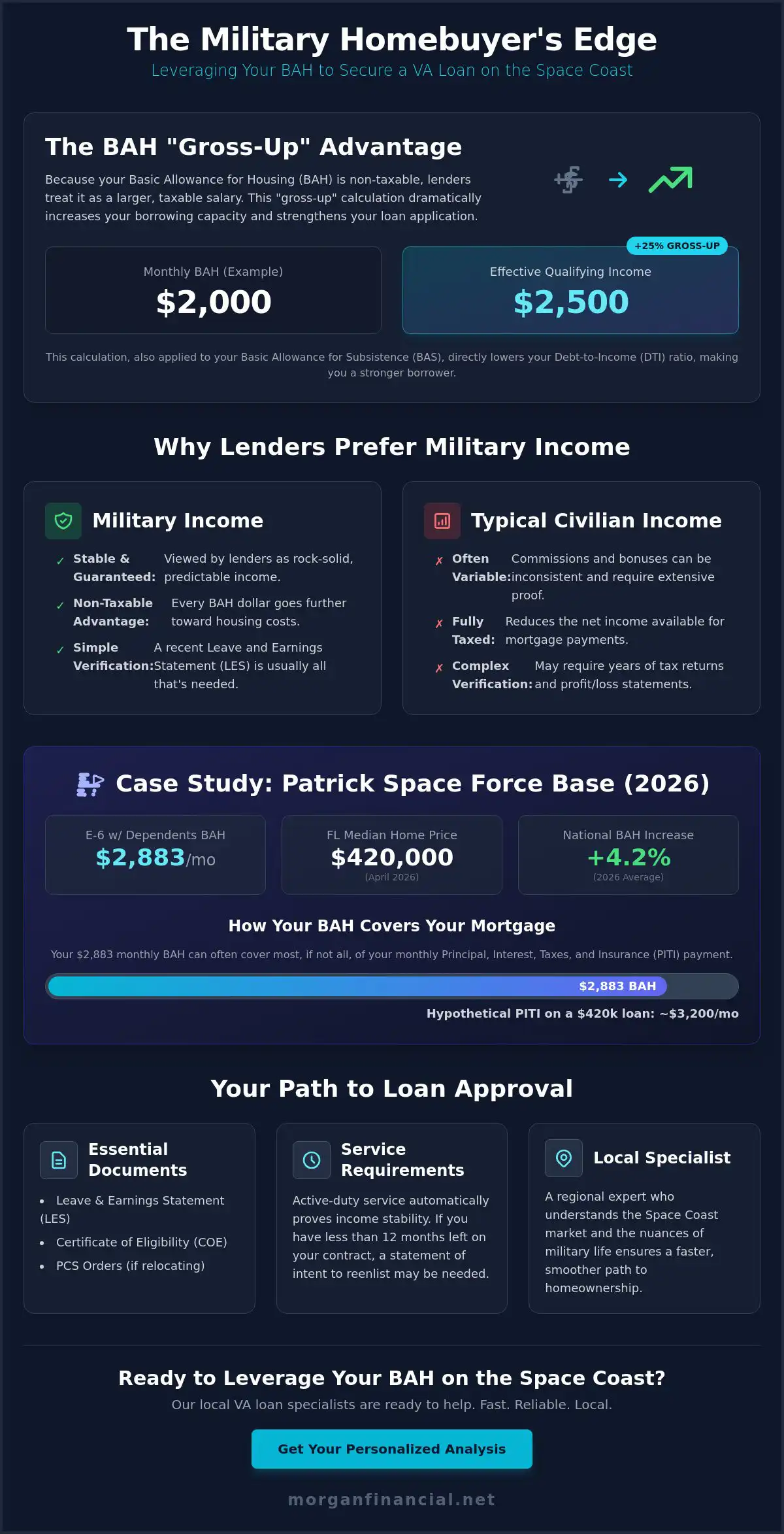

Your housing allowance is more than just a line item on your LES. It’s a powerful multiplier for your purchasing power. Because BAH is non-taxable, underwriters “gross up” this income to account for the tax savings you enjoy. This means we treat your allowance as if it were a larger, taxable salary. When you are using BAH to qualify for a mortgage, this calculation can be the difference between a “maybe” and a “yes” from the underwriting department. It is efficient. It is logical. It is effective.

This gross-up process directly lowers your Debt-to-Income (DTI) ratio. A lower DTI makes your loan profile stronger and more attractive to lenders. To verify this income, we typically need your most recent Leave and Earnings Statement and your Certificate of Eligibility. If you are in the middle of a transition, your PCS orders serve as proof of your future entitlement in the Melbourne or Palm Bay area. We handle the paperwork. You focus on the move. We make the process seamless.

The Math Behind the Gross-Up

The standard calculation involves adding 25 percent to the non-taxable portion of your income. For example, if you receive $2,000 in monthly BAH, a lender will often qualify you as if you earned $2,500. This same math applies to your Basic Allowance for Subsistence (BAS). Consider a $400,000 loan scenario. Without grossing up, a service member might hover right at the edge of acceptable DTI limits. With the gross-up, that same borrower gains significant breathing room. According to industry standards for Using BAH for VA Loans, this practice is essential for accurately representing a veteran’s true financial strength.

Underwriting Standards for 2026

Underwriting standards for 2026 remain focused on income stability. VA guidelines generally look for a 24-month history of stable income, but active-duty service provides an automatic pass for stability. If you have less than 12 months remaining on your current contract, we may need a statement of intent to reenlist or proof of a valid job offer for your post-military career. Your Certificate of Eligibility (COE) is the foundational document that confirms your status and entitlement. If you’re unsure how your specific LES translates to a loan amount, reach out to our Space Coast team for a personalized analysis. We provide clarity. We deliver results. We secure your future.

Balancing Your BAH Against Space Coast Mortgage Payments

Securing a home near Patrick Space Force Base requires a clear-eyed look at the 2026 housing landscape. For an E-6 with dependents stationed at Patrick SFB, the 2026 BAH rate is $2,883 per month. This monthly allowance is a robust tool when using BAH to qualify for a mortgage in Brevard County. It often covers a significant portion, if not all, of your monthly principal, interest, taxes, and insurance (PITI). While the Florida median home price reached $420,000 in April 2026, the Space Coast remains a strategic buy zone due to its unique military community and stable property values.

Local tax exemptions for disabled Veterans provide an additional financial boost. In Florida, Veterans with a service-connected disability may qualify for significant property tax discounts or total exemptions. This reduction in your monthly PITI allows your BAH to stretch even further. It increases your buying power without increasing your out-of-pocket costs. We focus on these regional details to ensure you maximize every benefit you’ve earned. Fast. Reliable. Local.

Space Coast Market Dynamics

The 2026 Melbourne and Palm Bay markets are currently in a healthy rebalancing phase. Inventory has increased to approximately a 4.7-month supply, giving buyers more negotiating power than in previous years. You can use our mortgage calculator to map your specific BAH rate to a realistic home price. Strategic neighborhoods in Viera, Satellite Beach, and Merritt Island continue to hold value well during PCS cycles. These areas offer proximity to the base and the high-tech corridor, making them excellent long-term investments for military families using BAH to qualify for a mortgage.

Maximizing Your Entitlement

Deciding between renting on-base and buying in the community often comes down to a break-even analysis. With the 4.2 percent national average increase in BAH for 2026, many service members find that owning a home is more cost-effective than renting. Your allowance can cover a standard VA loan or act as a substantial subsidy for a larger jumbo loan if you’re looking for more space. Unlike renting, homeownership builds equity that you take with you to your next duty station. Learn more about VA Loan Resources to see how your entitlement compares to current Florida mortgage rates, which averaged around 5.875 percent for VA loans in May 2026. We provide the expertise you need to make an informed, confident decision.

Common Hurdles: PCS Moves, ETS Dates, and Verification

Military life moves fast. Transitioning to the Space Coast or preparing for civilian life brings unique hurdles to the mortgage process. Lenders must verify that your income is stable, predictable, and likely to continue. When you are using BAH to qualify for a mortgage, you must also meet strict occupancy requirements. You must intend to occupy the home as your primary residence, typically within 60 days of closing. We handle the logistics. We verify the data. We protect your investment.

Continuity of income is the benchmark for loan approval. If you are approaching an Expiration of Term of Service (ETS) or retirement, underwriters often apply the “12-month rule.” This means your income must be guaranteed for at least one year following your closing date. If your enlistment ends within that window, you might need a statement of intent to reenlist or a firm job offer in the Melbourne or Palm Bay area. We know the local employers. We understand the timeline. We bridge the gap.

Buying Before You Arrive

You can secure your Florida home before your boots hit the ground. Underwriters can use the future BAH rates for your new duty station to determine your buying power today. This allows you to leverage the $2,883 rate for a Patrick SFB E-6 with dependents even while you are still out of state. A “Statement of Service” letter from your Commanding Officer acts as the primary verification tool. It confirms your rank and service status with total authority. We also verify any transitions from single to dependent rates to ensure using BAH to qualify for a mortgage reflects your actual future income with total precision.

The ETS and Retirement Transition

The final year of service requires specialized documentation to ensure a seamless approval. We can often supplement your BAH with projected retirement pay or verified VA disability income to strengthen your application. This multi-layered approach ensures your Debt-to-Income ratio remains low and your approval remains certain. Working with a local mortgage expert is the best way to prevent last-minute delays caused by transition paperwork. We are organized, transparent, and deeply committed to your success. Contact us today to start your transition with confidence. Fast. Reliable. Local.

Securing Your Florida Home with Morgan Financials Local Expertise

Navigating the Space Coast real estate market requires more than a simple online calculator. It demands a partner who understands the high-stakes nature of military moves and the specific nuances of Florida lending. At Morgan Financial, we don’t just process paperwork; we provide a steady hand in a complex landscape. Being veteran-owned and Space Coast-focused gives us a unique perspective on your needs. When you are using BAH to qualify for a mortgage, you deserve a team that treats your service record with the respect it deserves. We are organized. We are transparent. We are committed.

National call centers often struggle with the intricacies of non-taxable military income. They might miss the “gross-up” opportunities or fail to account for upcoming PCS adjustments. We eliminate that risk through effortless expertise. By staying local, we ensure your loan stays on track and closes on time. This speed and reliability are the hallmarks of our service. We bridge the gap between military entitlement and homeownership success for families across Brevard County. We make the process feel human and accessible.

Our “Stronger Than” Process

A standard pre-approval is often not enough in a competitive market. Sellers in Melbourne and Palm Bay want certainty before they take their home off the market. Our signature process is Stronger than a Pre-Approval because we perform a deep-dive underwriting of your file before you even find a home. This proactive approach identifies potential hurdles early, making your final offer as competitive as a cash bid. We also leverage a network of local appraisers who understand the specific value of neighborhoods near Patrick SFB and Cape Canaveral. This regional authority ensures your valuation is accurate and fair. Find your VA Home Loan in Melbourne, FL with a team that has mastered the local landscape.

Your Local Mission Partner

Personalized service is our standard, not an exception. Our staff includes fellow veterans who understand exactly what it means to move a family across the country on a tight deadline. We prioritize high-energy efficiency to keep you informed at every step of the journey. There are no automated phone trees or detached corporate offices here. You get direct access to regional specialists who take personal responsibility for your financial well-being. We frame the lending process as a positive emotional experience rather than a bureaucratic chore. Get started with your Space Coast purchase today and see how we make homeownership a reality for those who serve. Fast. Reliable. Local.

Take Command of Your Space Coast Future

You’ve earned your housing allowance through service. Now it’s time to put it to work. By leveraging the 25 percent gross-up rule and aligning your 2026 rates with the Melbourne housing market, you turn a monthly entitlement into lasting home equity. Using BAH to qualify for a mortgage is a strategic move to secure your family’s future near Patrick SFB or Cape Canaveral. It transforms a temporary benefit into a permanent foundation.

Morgan Financial is veteran-owned and operated. We are local Space Coast specialists who have closed over $1B in local Florida loans. We understand the rhythm of military life because we’ve lived it ourselves. Our team provides the speed, reliability, and expertise you need to win in a competitive market. We are organized. We are transparent. We are ready.

Apply Now for a Mortgage That Is Stronger Than a Pre-Approval. Your next mission starts with a home you love. We look forward to welcoming you home.

Frequently Asked Questions

Can I use BAH to qualify for a conventional loan, or is it only for VA loans?

You can use your housing allowance for both VA and conventional home loans. While VA loans are the most common choice for service members, conventional underwriters also recognize BAH as stable, recurring income. Most conventional lenders will still allow for the 25 percent “gross up” of this non-taxable income. This ensures your buying power remains high regardless of the specific loan product you choose for your Space Coast home.

Does a lender count my BAH if I am currently living in base housing?

Yes, lenders count your full BAH entitlement even if it currently goes directly to a privatized housing provider. Because you will be vacating base housing to move into your new home, that income becomes available to cover your mortgage. We simply verify the entitlement on your current LES. This allows you to use the full amount for using BAH to qualify for a mortgage on a property in Melbourne or Palm Bay.

What happens to my mortgage qualification if BAH rates drop next year?

Your qualification is protected by individual rate protection. The Department of Defense ensures that as long as you remain at your current duty station and rank, your BAH will not decrease even if the regional rates drop. Lenders qualify you based on the rate you are currently receiving or the rate listed on your PCS orders for the Space Coast. This provides a steady hand for your long-term financial planning.

Can I use my spouse’s income along with my BAH to qualify for a larger mortgage?

Combining your BAH with a spouse’s income is an excellent way to maximize your borrowing power. Lenders will add your spouse’s verified taxable income to your “grossed up” BAH to calculate your total Debt-to-Income ratio. This combined approach is often necessary to secure larger properties in high-demand areas like Viera or Satellite Beach. We analyze both income streams to provide a clear, reliable path to approval.

How do lenders verify BAH if I am about to PCS to Florida?

Lenders verify your upcoming income using your official PCS orders and a Statement of Service from your command. These documents allow us to use the 2026 BAH rates for Brevard County even before you officially report for duty. For example, we can use the $2,883 rate for an E-6 at Patrick SFB to calculate your loan limit today. It is a streamlined, logical process designed to get you into a home quickly.

Is there a limit to how much BAH can be “grossed up” for tax purposes?

The standard limit for “grossing up” non-taxable income is 25 percent. This percentage is set by secondary market guidelines to reflect the typical tax burden you avoid by receiving an allowance instead of a taxable salary. While this is the industry standard, using BAH to qualify for a mortgage requires a lender who knows how to apply this math correctly. We ensure every dollar of your entitlement is working at maximum efficiency.

Can I use my BAH to pay for a mortgage on a multi-family property?

You can use your BAH for a multi-family property as long as you intend to live in one of the units as your primary residence. This is a popular strategy for Veterans looking to build equity while having tenants cover a portion of the mortgage. VA loan guidelines allow for the purchase of up to a four-unit property. We help you navigate the specific occupancy and income requirements for these unique Space Coast investments.

What if my enlistment contract has less than 12 months remaining?

If your contract ends within 12 months of your closing date, you will need to provide additional documentation. This typically includes a statement of intent to reenlist or a valid job offer for a civilian position on the Space Coast. Lenders need to see that your income is likely to continue for at least three years. We work closely with you to gather the necessary paperwork and prevent any last-minute delays. Fast. Reliable. Local.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.