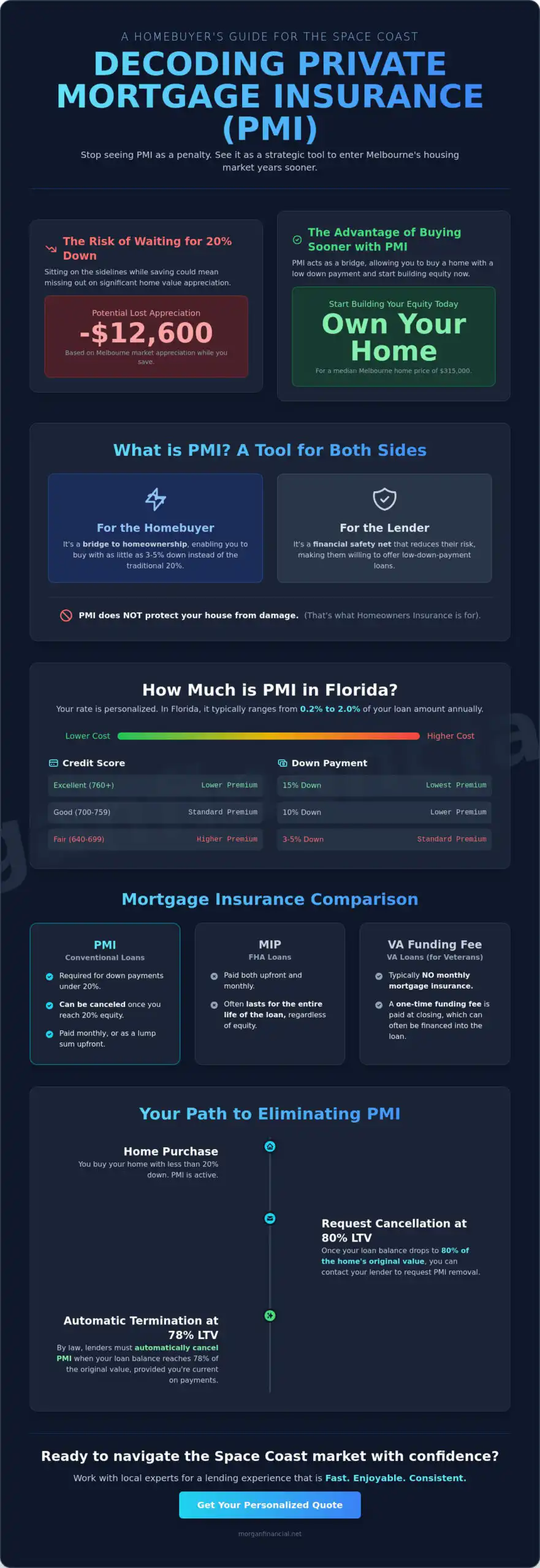

Waiting until you have a full 20% down payment could cost you $12,600 in lost appreciation while you sit on the sidelines of the Melbourne market. Most buyers view private mortgage insurance as an annoying penalty, but it’s actually a strategic tool that gets you into a home years sooner. When you understand the true pmi meaning, you stop seeing it as a hidden fee and start seeing it as a bridge to homeownership in the Space Coast.

We know that unexpected costs in the mortgage process create unnecessary anxiety, especially when the median home price in Melbourne has reached $315,000 as of March 2026. You deserve a lending experience that is Fast. Enjoyable. Consistent. This guide explains exactly how PMI impacts your monthly payment, how it compares to VA funding fees, and the specific federal rules for eliminating it once your equity grows. You’ll learn how to master your mortgage and eventually cancel this insurance for good.

Key Takeaways

- Master the true pmi meaning to see how this strategic tool allows you to buy a home in Melbourne with less than 20% down.

- Understand how your credit score and down payment size influence your specific rate, which typically ranges from 0.2% to 2% annually in Florida.

- Discover why veterans often bypass monthly insurance costs entirely by utilizing VA loans and the one-time funding fee instead.

- Identify the exact milestones for removing PMI automatically at 78% or requesting cancellation at 80% of your home’s original value.

- Work with local experts to navigate the 2026 Space Coast market with a process that is Fast. Enjoyable. Consistent.

What Does PMI Mean for Space Coast Homebuyers?

Understanding the pmi meaning is the first step toward a stress-free closing in Melbourne. At its core, Private Mortgage Insurance is a risk-mitigation tool used by conventional lenders. It acts as a financial safety net for the bank if a borrower stops making payments. While it might seem like a one-sided deal, it serves a vital purpose for you. It allows you to secure a home loan with as little as 3% or 5% down instead of the traditional 20%.

There’s a common paradox here. You pay the premium, but the lender gets the protection. This often causes frustration for first-time buyers. However, without this insurance, most lenders wouldn’t offer low-down-payment options at all. In the 2026 Melbourne market, where homes sell in an average of 63 days, waiting years to save $63,000 for a 20% down payment on a $315,000 home often means missing out on appreciation. PMI is the bridge that lets you cross from renter to owner today.

Don’t confuse this with your homeowners insurance. While your hazard insurance protects your actual house from Florida storms or fire, PMI only protects the mortgage balance. It doesn’t cover your belongings or structural repairs. It’s a specific financial instrument designed to manage lending risk and expand access to the housing market.

The Role of PMI in Conventional Loans

Lenders require PMI on conventional loans when the Loan-to-Value (LTV) ratio exceeds 80%. Your specific premium isn’t a flat fee. It’s calculated based on your credit score and your exact down payment percentage. A higher credit score usually leads to lower monthly costs. This system rewards financial responsibility while providing an affordable path to your new front door. It’s how we keep the process Fast. Enjoyable. Consistent. and get you into your Space Coast home without waiting decades to save a massive down payment.

Disambiguation: PMI vs. Other Economic Terms

When you search for the pmi meaning online, you might see headlines about the “Purchasing Managers’ Index.” That’s a global economic indicator used by manufacturing experts. It has nothing to do with your Florida mortgage. For your closing, the only “PMI” that matters is your insurance premium. You should also distinguish it from MIP, or Mortgage Insurance Premium. While PMI is for conventional loans, MIP is specific to FHA loans. Unlike PMI, which you can eventually remove, MIP often stays for the life of the loan. Knowing this difference helps you choose the most affordable home loan for your specific situation.

Calculating the Cost: How Much is PMI in Florida?

In Florida, PMI isn’t a one-size-fits-all charge. Most homeowners in the Sunshine State see rates between 0.2% and 2% of the loan amount annually. If you’re looking at the $315,000 median home price in Melbourne as of March 2026, your costs will vary based on your financial profile. Grasping the pmi meaning in terms of your monthly budget helps you plan for the long term. To truly understand What Does PMI Mean for your wallet, you have to look at your credit score and your down payment. A borrower with a 760 score and 10% down will pay significantly less than someone with a 640 score and 3% down. Your debt-to-income (DTI) ratio also plays a role in how insurers price your risk. Because Melbourne is currently a seller’s market, having a clear understanding of these costs ensures your offer is both competitive and sustainable.

At Morgan Financial, we prioritize transparency. We provide consistent estimates early in the process so you don’t face surprises at the closing table. Our goal is to make the lending experience Fast. Enjoyable. Consistent. We analyze local Brevard County property values to ensure your total monthly payment fits your lifestyle. When property values rise, as they did with the 4% increase seen in early 2026, your PMI costs are tied to the loan amount. We help you navigate these fluctuations with professional confidence and hometown pride.

Monthly vs. Upfront PMI Payments

Most Melbourne buyers choose to pay their PMI monthly. It gets bundled into your PITI (Principal, Interest, Taxes, and Insurance) payment. It’s predictable and requires less cash at closing. However, you can opt for single-premium PMI. This involves paying a one-time lump sum upfront. While it increases your closing costs, it lowers your monthly obligation and can increase your buying power. There are also split-premium options that combine both methods for flexible budgeting. This allows you to customize your loan to fit your current cash flow needs.

Using a Mortgage Calculator to Estimate PMI

Don’t guess your monthly budget. When you analyze the pmi meaning for your specific loan, you see that it’s a temporary cost with a long-term benefit. You can use our mortgage calculator to see your potential PMI based on different scenarios. Compare a 5% down payment against 10% or 15% to see how the premium drops as your equity increases. Seeing these numbers side-by-side helps you decide the best way to enter the Brevard County market. If you have questions about these figures, Contact a Mortgage Expert to get a personalized quote.

PMI vs. VA Funding Fee: The Veteran Advantage

For those who served, the pmi meaning shifts from a monthly obligation to a non-factor. VA loans are a cornerstone of the Space Coast real estate market because they never require monthly mortgage insurance. Instead of an ongoing premium, veterans typically pay a one-time VA Funding Fee. This fee can be paid upfront or rolled into the total loan amount, ensuring your monthly budget stays focused on principal and interest rather than lender protection. In a market where Melbourne home prices rose 4.0% over the last year, keeping your monthly overhead low is a major strategic win.

As of April 2026, the VA Funding Fee for first-time use with 0% down is 2.15% of the loan amount. For subsequent use, the rate is 3.3%. Compared to conventional PMI, which can cost up to 2% annually, the one-time fee is often much more cost-effective over the life of the loan. There’s an even bigger advantage for many: veterans receiving any level of VA disability compensation are completely exempt from this fee. This makes the VA product the most affordable home loan available in Brevard County. We take pride in being Florida’s Trusted Mortgage Experts, ensuring our local heroes navigate these benefits with a process that is Fast. Enjoyable. Consistent.

Why VA Loans Win on the Space Coast

The math is simple for Melbourne veterans. On a median-priced home of $315,000, a conventional buyer with 3% down might pay hundreds extra every month in PMI. A VA borrower avoids that monthly drain entirely while still putting 0% down. This increased purchasing power is vital in a seller’s market where homes average 63 days on market. You get to keep more of your hard-earned money in your pocket while building equity in a growing community. Explore our VA Loan Resource for Brevard County veterans to see how these savings apply to your specific situation.

When Conventional with PMI Might Still Make Sense

Despite the VA advantage, conventional loans with PMI remain a strong choice for certain buyers. If you are a multi-property owner or have significant equity from a previous sale, a conventional product might offer more flexibility. Conventional loans also have different appraisal and inspection standards that can sometimes be beneficial in specific high-equity scenarios. If you’re looking for ways to How to Remove or Avoid PMI through a larger down payment or a different loan structure, it’s worth weighing both options. Our team helps you analyze the pmi meaning for your specific financial goals so you can choose the path that leads to the most enjoyable home-buying experience.

How to Remove or Avoid PMI on Your Florida Home

Mastering the pmi meaning involves knowing exactly when this monthly cost ends. The Homeowners Protection Act (HPA) is a federal law that ensures you aren’t stuck with insurance premiums forever. You have the right to request PMI cancellation once your loan balance is scheduled to reach 80% of the home’s original value. If you stay current on your payments, your lender is legally required to automatically terminate the insurance when your balance hits 78% LTV. For a $315,000 home in Melbourne, reaching that 22% equity milestone is a significant financial victory that immediately lowers your monthly overhead.

There is also a “final termination” rule. If you haven’t reached the 78% threshold, the lender must still cancel the insurance at the midpoint of your loan’s amortization schedule. On a 30-year mortgage, this happens at the 15-year mark. However, most Space Coast homeowners don’t want to wait a decade and a half to save money. Homeowners who are serious about eliminating PMI faster and building equity more aggressively may want to explore how a 15yr fixed mortgage accelerates wealth building for Florida homeowners by reaching the equity threshold in significantly less time. We focus on making your mortgage experience Fast. Enjoyable. Consistent. and that includes helping you find the quickest path to equity.

Leveraging Florida Market Appreciation

Rising home values in Palm Bay and Titusville provide a unique opportunity to eliminate insurance early. In March 2026, Melbourne saw a 4.0% increase in median sale prices compared to the previous year. If your home’s value has jumped significantly, you don’t have to wait for your scheduled payments to hit the 80% mark. You can order a new appraisal or a broker price opinion (BPO) to prove your current equity has surpassed 20%. If the math works in your favor, learn about our easy refinance process to move into a loan without any insurance requirements at all.

Avoiding PMI at the Start

The most direct way to bypass the pmi meaning entirely is a 20% down payment. While this is the gold standard, it isn’t the only path. Some buyers use “piggyback loans,” where a second mortgage covers 10% of the cost, leaving you with an 80% primary loan and a 10% down payment. Another option is Lender-Paid Mortgage Insurance (LPMI). With LPMI, the lender pays the premium in exchange for a slightly higher interest rate. This can be a smart move if you plan to stay in the home for a long time and want a predictable, single monthly payment. If you want to see which strategy fits your budget, Contact a Mortgage Expert to explore your options today.

Working with Florida’s Trusted Mortgage Experts

Navigating the Space Coast real estate market requires more than just a basic understanding of pmi meaning. It requires a partner who knows the nuances of Brevard County lending, from the specific insurance requirements in coastal zones to the fast-paced nature of Melbourne’s current seller’s market. We pride ourselves on being Florida’s Trusted Mortgage Experts. Our team understands that mortgage insurance isn’t just a line item on your closing disclosure; it’s a strategic factor that determines your monthly lifestyle. We help you weigh the costs of PMI against the benefits of entering the market today rather than years from now. This personalized approach ensures your lending experience remains Fast. Enjoyable. Consistent.

Every homebuyer has a unique financial profile. Some may benefit from a conventional loan with a small down payment, while others find that a VA loan offers the most affordable path. We don’t believe in a one-size-fits-all mortgage. Instead, we provide the professional confidence you need to make an informed decision. By analyzing your credit score, debt-to-income ratio, and long-term equity goals, we help you minimize costs and maximize your purchasing power. We act as your steady hand throughout the entire process, ensuring you feel secure from your initial pre-approval to the moment you receive your keys.

Personalized Lending in Melbourne and Beyond

Our roots run deep in the local community. From the quiet streets of Indialantic to the growing neighborhoods in West Melbourne, we serve our neighbors with hometown pride. As a veteran-owned business, we bring a level of transparency and high-energy efficiency to the lending process that traditional big-box banks often lack. We don’t just process paperwork; we build relationships. Whether you’re a first-time buyer trying to grasp the pmi meaning or a veteran looking to leverage your hard-earned benefits, we provide a stress-free experience that prioritizes your success. You deserve an overachiever in your corner who takes personal responsibility for your financial well-being.

Ready to Start Your Home Search?

The Melbourne market moves at a brisk pace. With homes averaging 63 days on the market as of March 2026, you can’t afford to wait until you find a house to start your financial paperwork. Getting pre-approved is the most critical step you can take. It signals to sellers that you are a serious, qualified buyer who has already mastered the complexities of the mortgage process. We invite you to start your purchase journey today by speaking with one of our local mortgage experts. We will sit down with you to compare all available loan products side-by-side, ensuring your monthly payment is both predictable and affordable. Contact Morgan Financial to discuss your PMI and loan options and discover how we make homeownership an enjoyable reality.

Secure Your Future in the Melbourne Market

Private mortgage insurance shouldn’t be a source of anxiety. Once you grasp the full pmi meaning, it becomes a strategic asset that helps you build equity in a market that saw a 4.0% price increase in early 2026. Whether you utilize the VA loan advantage to skip monthly premiums entirely or use PMI to enter the market with a low down payment, you’re taking a definitive step toward long-term wealth. Federal law protects your investment by ensuring these payments aren’t permanent, with automatic removal milestones that reward your growing equity.

As Florida’s Trusted Mortgage Experts, we are here to ensure your journey is Fast. Enjoyable. Consistent. We are a veteran-owned and operated team that takes pride in serving our neighbors from Melbourne to the beaches. You don’t have to navigate these complex financial decisions alone. Our professionals are ready to help you compare loan products and find the perfect fit for your budget. Talk to a Space Coast Mortgage Expert Today to find the most affordable path to your new front door. We look forward to helping you call Florida home.

Frequently Asked Questions

Is PMI required on all mortgage loans in Florida?

No, PMI is not mandatory for every Florida loan. It only applies to conventional mortgages where the down payment is less than 20% of the purchase price. Government-backed options like VA loans bypass this monthly cost entirely; while FHA loans use a different system called Mortgage Insurance Premium (MIP).

How long do I have to pay for private mortgage insurance?

You typically pay PMI until your loan-to-value ratio reaches 78% for automatic termination. However, you have the right to request cancellation once you reach 80% equity. This timeline depends on your specific payment schedule and how quickly your home value appreciates in the local market.

Can I get a refund on PMI if I refinance my home?

Refinancing usually does not result in a refund for monthly PMI premiums already paid. If you chose a single-premium upfront option, you might receive a pro-rated refund in very specific cases. Most homeowners find their “refund” comes in the form of a significantly lower monthly payment after the refinance eliminates the insurance requirement.

Does PMI cover me if I lose my job or cannot pay my mortgage?

No, PMI does not provide you with any personal financial protection. It is strictly a risk-mitigation tool that protects the lender if the loan goes into foreclosure. If you want coverage for job loss or disability, you would need to purchase a separate mortgage protection insurance policy.

What is the difference between PMI and the VA funding fee?

PMI is a recurring monthly expense that stays on your loan until you build enough equity. The VA funding fee is a one-time charge that ranges from 1.25% to 3.3% as of April 2026. Understanding the pmi meaning versus the funding fee helps veterans choose the most cost-effective path for their Space Coast home purchase.

How do I know if my LTV is low enough to cancel PMI?

Divide your current principal balance by the original purchase price of your home. If that number is 0.80 or lower, you have reached the 80% LTV threshold required to request cancellation. You can also use a new appraisal to see if Melbourne’s 4.0% annual appreciation has pushed your equity higher than your original loan terms suggest.

Does PMI increase my property taxes in Brevard County?

PMI has no impact on your property taxes. Your taxes are determined by the Brevard County Property Appraiser based on your home’s assessed value and local millage rates. While both are often bundled into your monthly mortgage payment, they are completely separate financial obligations.

Can I pay off my PMI in one lump sum at closing?

Yes, you can choose single-premium PMI at your closing to avoid monthly charges. This allows you to pay the entire cost upfront, which lowers your recurring monthly obligation. It is an excellent way to simplify your pmi meaning and maximize your monthly cash flow from day one.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.