Can You Buy a House with Student Loan Debt in Florida?

Yes, absolutely. Buying a house in Florida with student loan debt is not just a possibility; for many professionals and Veterans on the Space Coast, it’s a smart financial reality. The persistent myth that you must be debt-free to own a home is one of the most significant barriers holding people back from building equity. Florida lenders, especially local experts who understand the market, are far more interested in your ability to manage monthly payments than the total six-figure balance on your student loans.

The landscape of mortgage lending has evolved. Lenders now recognize student debt as a standard part of the modern financial profile, not an automatic disqualifier. With the right strategy, loan product, and local guidance, your student debt becomes a simple math problem to solve, not a roadblock to your dream of owning a home in Brevard County.

- Yes, buying a home with student debt in Florida is entirely achievable.

- Lenders focus on your ability to manage monthly payments, not just the total balance.

- Florida’s diverse loan landscape offers specific paths for debt-carrying professionals and Veterans.

- The "Steady hand in a complex landscape" approach: Why local expertise matters for debt holders.

The Reality of Student Debt in the Housing Market

Recently, a significant portion of homebuyers in Florida, particularly in thriving professional hubs like Melbourne and Palm Bay, will be navigating the process with student loans. Waiting to pay off this debt entirely can be a costly mistake. While you spend years—or even decades—aggressively paying down loans, home prices and interest rates can rise, potentially pricing you out of the market. The equity you could have been building in your own home is instead going toward your landlord’s mortgage.

Since 2020, lender perspectives have shifted dramatically. Underwriters are now more sophisticated in how they evaluate student debt, recognizing that many borrowers are on long-term, low-payment plans that are perfectly manageable. They’ve moved from a rigid, one-size-fits-all approach to a more nuanced evaluation of your overall financial health.

Total Balance vs. Monthly Impact

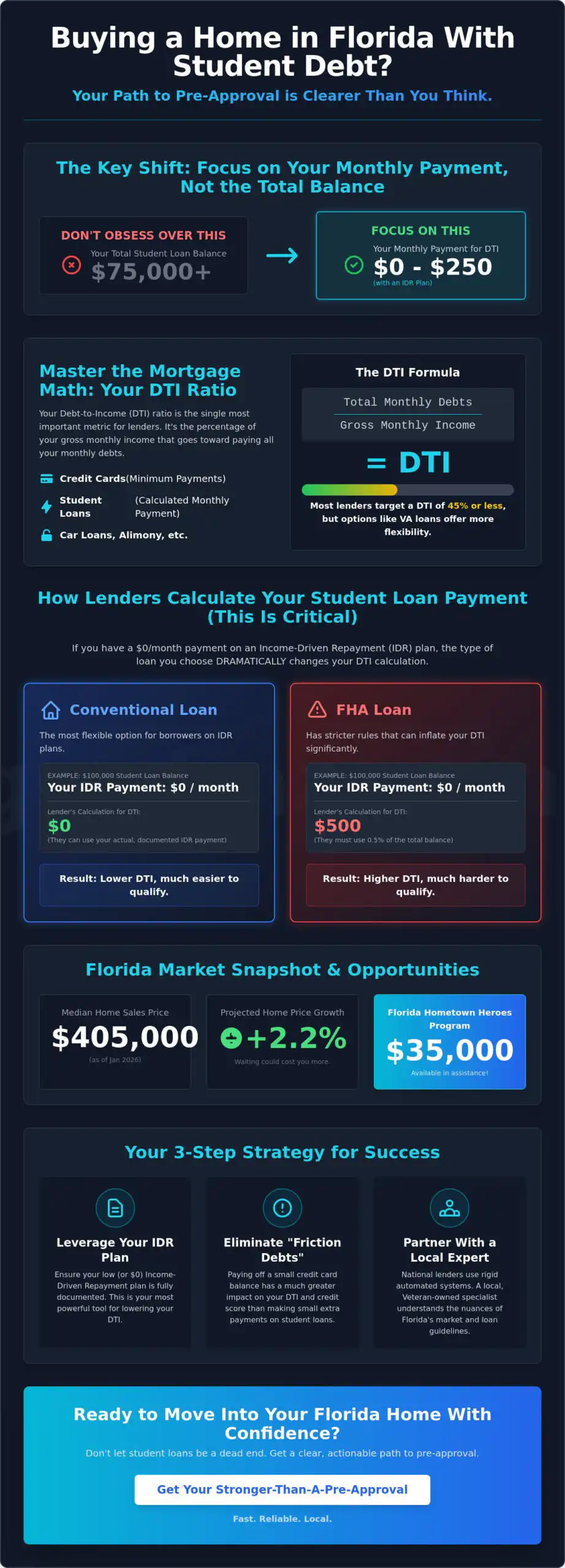

Seeing a student loan balance of $80,000, $150,000, or more can be intimidating. It’s easy to assume that no bank would trust you with a mortgage on top of that. However, lenders are focused on a much more practical number: your monthly debt obligation. They differentiate between the "scary" total loan number and the "workable" monthly payment.

This is where the concept of the Debt-to-Income (DTI) ratio comes into play. It’s a simple calculation that compares your total monthly debt payments to your gross monthly income. Your $150,000 student loan might only require a $250 monthly payment under an Income-Driven Repayment (IDR) plan, which has a very different impact on your DTI than a private loan with a $1,200 monthly payment. Understanding this distinction is the first step toward mortgage approval.

The Math Behind the Mortgage: DTI and Your Student Loans

Your Debt-to-Income (DTI) ratio is the heartbeat of your mortgage application. It’s the primary metric lenders use to assess your ability to comfortably handle a new mortgage payment alongside your existing debts. For borrowers with student loans, understanding how this number is calculated is non-negotiable. Lenders have specific, non-intuitive rules for calculating your student loan payment, especially if it’s currently in deferment or on an IDR plan.

Even if your monthly payment is $0 under a SAVE or PAYE plan, lenders won’t use $0 in their calculation. To account for a future potential payment, they typically use a percentage of your total loan balance. The most common formulas are:

- The 0.5% Rule: Many conventional loans (backed by Fannie Mae) will use 0.5% of your outstanding loan balance as your monthly payment. For a $100,000 loan, this would be calculated as a $500 monthly payment.

- The 5% VA Rule: VA loan programs use 5% of the balance, divided by 12 months. For that same $100,000 loan, the calculated monthly payment would be approximately $417.

- The Actual Documented Payment: The best-case scenario is when a lender can use the actual, fully amortized payment listed on your credit report or loan statement. This is often possible if you are on a standard repayment plan.

While DTI is critical, your credit score remains the ultimate indicator of your financial discipline. A strong history of on-time payments—including your student loans—tells Florida lenders that you are a reliable borrower, which can help offset a DTI ratio that is on the higher side.

Calculating Your DTI for a Florida Home Purchase

You can calculate your own DTI to see where you stand before ever speaking to a lender. The formula is straightforward:

(Total Monthly Debt Obligations / Gross Monthly Income) = DTI Ratio

Here’s a step-by-step breakdown:

- Calculate Your Gross Monthly Income: This is your total income before taxes or any other deductions are taken out. If you earn $90,000 a year, your gross monthly income is $7,500.

- Add Up Your Monthly Debt Obligations: This includes your minimum monthly payments for credit cards, car loans, personal loans, and, of course, your student loans (using the lender’s calculation method described above). Do not include current rent, utilities, or cell phone bills.

- Divide and Convert: Divide your total monthly debts by your gross monthly income. For example, if your debts are $2,500 and your income is $7,500, your DTI is $2,500 / $7,500 = 0.33, or 33%.

To get a clearer picture of your specific situation, it’s helpful to use a dedicated tool. You can use our mortgage calculators to run your own numbers and estimate your potential buying power.

The Role of Credit Scores and Payment History

Your payment history is the single most important factor affecting your credit score. A long record of consistent, on-time student loan payments is a massive "gold star" on your application. It demonstrates to underwriters that you honor your financial commitments, even over the long term. This history of responsible borrowing is precisely what lenders want to see.

It’s also important to understand how student loans affect your credit utilization. Unlike a credit card, where a high balance relative to your limit can tank your score, student loans are treated as installment debt. A high balance does not negatively impact your credit utilization ratio in the same way. As long as you are making payments on time, your student loan debt is actively helping you build a positive credit history, which is essential for securing the best mortgage rates in Florida.

VA vs. Conventional: Choosing the Right Florida Loan Program

For Florida homebuyers with student debt, not all mortgage products are created equal. The two most powerful and flexible options are VA Home Loans and Conventional Loans. At Morgan Financial, we specialize in these products precisely because they offer the most effective solutions for borrowers managing educational debt, especially for our community of Veterans and professionals on the Space Coast.

We strategically focus on VA and Conventional loans over FHA or USDA options. FHA loans often come with stricter DTI calculations for student debt and mandatory mortgage insurance for the life of the loan. VA and Conventional products provide more forgiving guidelines and better long-term financial advantages for our clients.

VA Loan Advantages for Debt-Carrying Veterans

For eligible Veterans, active-duty personnel, and surviving spouses in Florida, the VA loan is hands-down the most powerful tool for buying a home with student loan debt. The Department of Veterans Affairs prioritizes a Veteran’s overall financial stability over rigid DTI caps.

The key advantages include:

- Residual Income Guidelines: Instead of a strict DTI limit, VA lenders focus on "residual income"—the amount of money left over each month after all major expenses (including the new mortgage and student loans) are paid. If you can demonstrate sufficient residual income for your family size and location, a DTI ratio that would be rejected for a conventional loan can often be approved.

- More Lenient Student Loan Calculations: VA guidelines are often more flexible in how they calculate student loan payments, sometimes allowing for the use of a documented IDR payment, even if it’s very low.

- Zero Down Payment: The ability to buy a home with 0% down is a massive strategic advantage. It allows you to preserve your cash savings, which can be used to pay down other high-interest consumer debt (like credit cards) to further improve your financial picture before closing.

To learn more about how these benefits can work for you, explore our comprehensive VA loan resource for Space Coast Veterans.

Conventional Loan Strategies

A Conventional loan is an excellent option, particularly for high-earning professionals who may not be VA-eligible. While Conventional DTI requirements are typically stricter than VA guidelines (often capping around 43-50%), there are effective strategies to make your application successful.

One powerful tool is the use of "Gift Funds." If a family member provides a financial gift for your down payment, it can significantly improve your profile. A larger down payment reduces the total loan amount, which in turn lowers your proposed monthly mortgage payment and improves your DTI ratio. This can be the single move that pushes your application over the finish line.

It’s also crucial to factor in Private Mortgage Insurance (PMI). If you put down less than 20%, you will have a monthly PMI payment, which is added to your debt obligations and impacts your DTI. Planning for this extra cost is essential for a smooth approval process.

Preparation Strategy: How to Get Ready to Buy on the Space Coast

Securing a mortgage with student debt isn’t just about meeting the minimum requirements; it’s about presenting the strongest possible financial profile to lenders. A proactive preparation strategy can make all the difference, especially in competitive Brevard County markets like Viera and Titusville. The goal is to reduce financial "friction" and assemble a file that is clean, organized, and easy for an underwriter to approve.

Start by auditing your student loan status. Are you on the repayment plan that is most advantageous for a mortgage application? Sometimes, a slightly higher monthly payment that is fully amortized can be better for DTI calculations than a $0 IDR payment that forces the lender to use the 0.5% balance rule. You should also focus on lowering other, more impactful debts. Paying off a $5,000 credit card balance will have a much greater positive effect on your DTI than making an extra $5,000 payment on a $100,000 student loan.

Finally, nothing demonstrates seriousness and strength like getting a fully underwritten pre-approval. Our unique Stronger Than a Pre-Approval process puts your file through underwriting before you even make an offer, giving you the power of a cash buyer in the competitive Space Coast market.

Tactical Debt Reduction

When preparing for a mortgage, not all debt reduction is created equal. The two classic methods, "Snowball" (paying off smallest balances first) and "Avalanche" (paying off highest interest rates first), should be viewed through the lens of DTI improvement.

Crucially, you must avoid taking on any new debt in the six to twelve months before applying for a home loan. A new car loan can single-handedly derail your home buying plans by drastically increasing your DTI ratio. The best first step is always to consult a mortgage consultant early in the process. We can analyze your specific debt profile and create a targeted plan to put you in the strongest possible position for approval.

Local Market Readiness in Brevard County

Understanding the local market dynamics in Brevard County is a key part of your strategy. Inventory levels and demand in Viera can be very different from those in Cocoa or Satellite Beach. In a fast-moving market, sellers receive multiple offers, and they are looking for the one that is most certain to close without delays.

This is where our Stronger Than a Pre-Approval program becomes your ultimate competitive advantage. A standard pre-qualification letter is based on a surface-level review of your finances. Our process involves a full credit and income review by an underwriter upfront. When you make an offer with our approval letter, you are signaling to the seller that your financing is solid and secure. This level of preparation can be the deciding factor that gets your offer accepted over others, even if the bid is slightly lower.

Partnering with Morgan Financial: Your Local Florida Mortgage Experts

Navigating a home purchase with student loan debt requires more than just a calculator; it requires a strategic partner who understands the local landscape and specializes in the loan products that serve you best. As a Veteran-owned and operated lender, Morgan Financial is built on a foundation of service and expertise. We understand the unique financial profiles of our Space Coast community, from active-duty personnel at Patrick SFB to the engineers and professionals driving our local economy.

Your journey to homeownership is our mission, and we are here to provide the steady hand you need to succeed. Additionally, for those who want to ensure their debt management aligns with their long-term wealth goals, Mainstream Financial Group offers the financial advisory and retirement planning expertise necessary for a secure future.

Why a Local Specialist Beats a National Bank

When you work with a national call-center lender, you’re just another file number. When you work with Morgan Financial, you’re our neighbor. Our team lives and works in Melbourne, Satellite Beach, and the surrounding communities. We have intimate knowledge of local Florida property taxes, insurance requirements, and closing costs that out-of-state lenders simply can’t match.

This local expertise translates into a smoother, faster, and more predictable closing process. We anticipate regional hurdles before they become problems and provide personalized service from loan professionals who are invested in the community. You get direct access to your dedicated expert, ensuring your questions are answered quickly and accurately.

Ready to Start Your Journey?

Student loan debt doesn’t have to be a barrier to homeownership in Florida. With the right strategy and the right local partner, you can turn your dream of owning a home on the Space Coast into a reality. Our process is designed for speed and clarity, empowering you with the confidence you need to make a strong offer.

Your next step is simple. Let our team of dedicated professionals show you the clear path to a mortgage approval. We’ll analyze your situation, identify the best loan program for your needs, and provide a concrete action plan.

Start your Florida home purchase today.

Frequently Asked Questions About Buying a Florida Home with Student Debt

**Can I buy a house in Florida if my student loans are in default?

**

Generally, no. Most mortgage programs, including VA and Conventional, require you to be current on all federal debt. If your loans are in default, you will likely need to enter a rehabilitation program and make a series of on-time payments before you can be eligible for a mortgage.

**How much student loan debt is too much for a mortgage?

**

There is no specific dollar amount that is "too much." Lenders are concerned with your debt-to-income (DTI) ratio, not the total loan balance. A borrower with a $200,000 student loan balance but a high income and low monthly payment could easily qualify, while someone with a $30,000 balance but a lower income and high monthly payment might struggle.

**Do Florida lenders use my total student loan balance or my monthly payment?

**

Lenders use your monthly payment for the DTI calculation. However, if your reported monthly payment is $0 (as in some IDR plans) or you are in deferment, they will not use $0. Instead, they will use a calculated figure, typically 0.5% of your total loan balance for Conventional loans, or your documented IDR payment for some VA loan scenarios.

**Can I use a VA loan if I have a high DTI from student loans?

**

Yes. The VA loan is one of the best options for borrowers with high DTI. The VA uses a more holistic approach that prioritizes residual income over a strict DTI cap. If you can show you have enough money left over each month to cover family living expenses, the VA may approve a loan with a DTI that would be denied by other programs.

**Should I consolidate my student loans before applying for a mortgage?

**

It depends. Consolidation can sometimes lower your monthly payment, which would help your DTI ratio. However, it can also extend your repayment term. It is critical to speak with a mortgage professional before making any changes to your loan structure, as it could have unintended consequences on your qualification.

**How does an Income-Driven Repayment (IDR) plan affect my mortgage approval?

**

An IDR plan can be very beneficial, as it often results in a low monthly payment that helps your DTI ratio. However, be aware that lenders will not use a $0 payment. They will use either the documented monthly payment or a calculated payment based on a percentage of your total loan balance (e.g., 0.5%). Having the official IDR documentation from your loan servicer is crucial.

**What is the minimum credit score needed to buy a house with student debt in Florida?

**

Credit score requirements vary by loan type. For Conventional loans, a minimum score of 620 is typically required, but better interest rates are available for scores of 740 and above. For VA loans, the VA itself does not set a minimum score, but most lenders look for a score of 620 or higher. A strong credit history with on-time payments is vital for both.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.