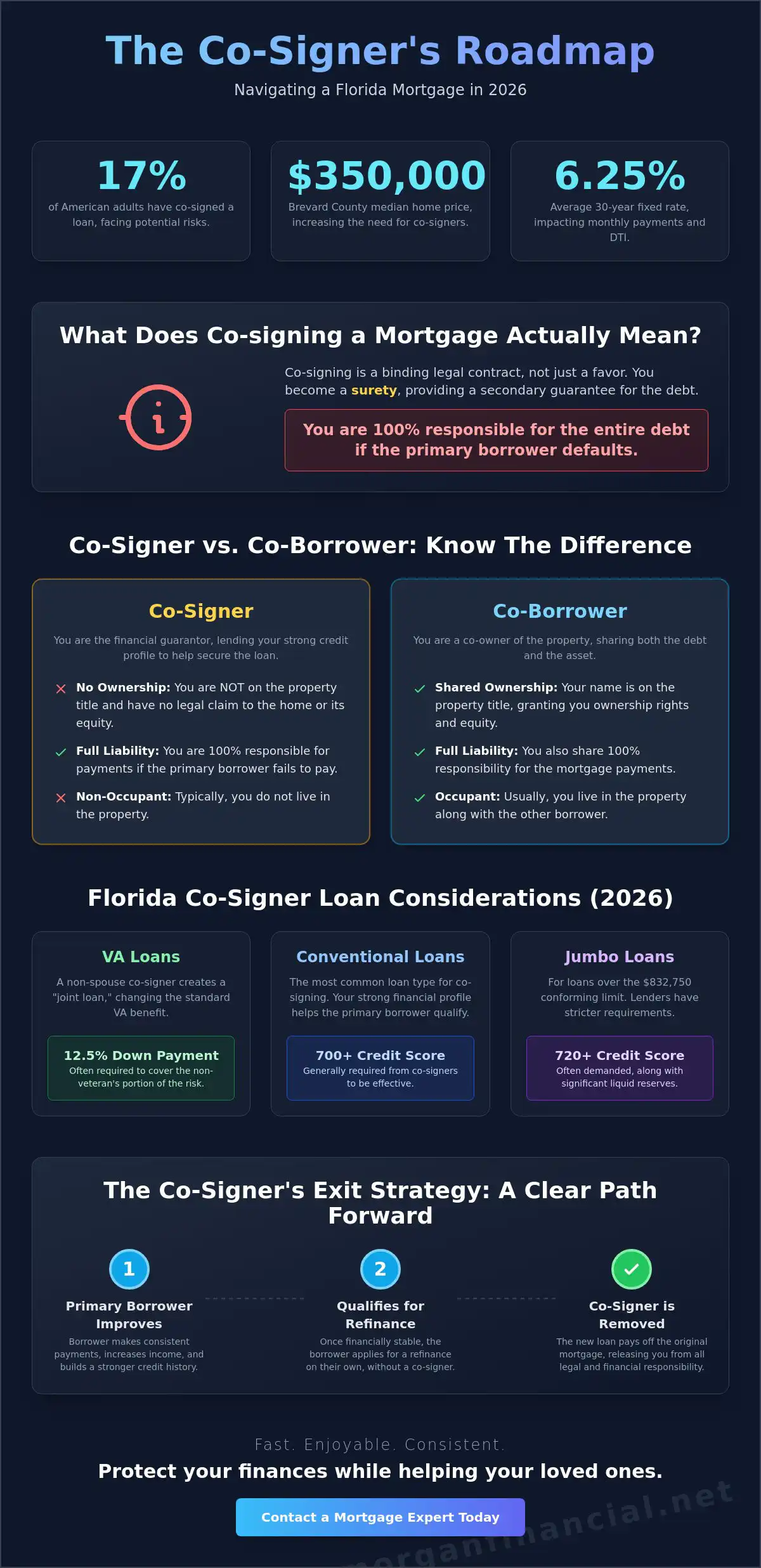

Did you know that 17% of American adults have co-signed a mortgage at least once as of 2026? While helping a family member secure a home in Florida is a generous move, it often comes with a side of anxiety. You likely worry about being tied to a 30-year debt or seeing your credit score drop if a payment is missed.

At Morgan Financial, we believe co signing a mortgage loan should be a strategic bridge, not a financial trap. We’ll show you how to protect your personal borrowing power while helping your loved ones achieve homeownership. You will learn the specific legal liabilities of the 2026 market, the impact on your credit, and the exact steps to be removed from the loan through a future refinance. We’re providing a clear roadmap of Florida market strategies and credit protection to keep your experience fast, enjoyable, and consistent.

Key Takeaways

- Understand the full legal weight of co signing a mortgage loan, which places 100% responsibility for the debt on you regardless of who lives in the home.

- Learn the essential differences between a co-signer and a co-borrower to protect your interests regarding property titles and ownership rights.

- Account for unique Space Coast market factors, including specific property taxes and insurance in Melbourne and Palm Bay, that influence your total monthly debt-to-income ratio.

- Establish a reliable exit strategy using a professional refinance to eventually remove your name and liability from the mortgage once the primary borrower is ready.

What Does Co-signing a Mortgage Loan Actually Mean?

Co-signing is more than a simple favor or a character reference. It is a binding legal contract where a non-occupant party guarantees the full repayment of a home loan. When you are cosigning a mortgage loan, you aren’t just helping someone get through the door. You are telling the lender that you are 100% responsible for the debt if the primary borrower defaults. This arrangement is common in Melbourne and across Florida, especially as the Brevard County median home sale price reached $333,967 in March 2026. Buyers often face high debt-to-income (DTI) ratios or limited credit histories, making a co-signer the only bridge to a successful home purchase.

At Morgan Financial, we believe the process should be fast, enjoyable, and consistent. That starts with total transparency about what you are signing. Lenders are diligent about verifying every dollar. They aren’t just looking at the borrower’s ability to pay; they are looking at yours too. If the primary borrower has an income gap or a credit score that doesn’t quite meet the 2026 standards, your financial profile fills that void to secure the financing.

The Legal Obligation: It Is More Than a Favor

Lenders view a co-signer as equally liable for the mortgage from day one. This isn’t a “backup” role. If a payment is missed, it shows up on your credit report immediately, just as it does for the person living in the house. To understand the legal foundation of this role, it helps to ask: What is a surety? In this context, you act as a surety by providing a secondary guarantee for the debt. This creates a state of “joint and several liability.” In plain English, this means the lender has the legal right to demand the entire monthly payment from you alone if the primary borrower fails to pay, without needing to exhaust all collection efforts against them first.

Who Can Be a Co-signer in Florida?

In the Florida market, co-signers are typically parents, siblings, or very close relatives with a proven track record of financial stability. Lenders generally require co-signers to demonstrate a strong credit score and a stable income that can comfortably absorb the new debt. You don’t have to live in the property to be a co-signer. Your role is purely financial, providing the “cushion” the lender needs to approve the loan. This allows your loved one to build equity in a home while you provide the necessary credit support to make the deal happen.

Co-signer vs. Co-borrower: Navigating Different Loan Types

Distinguishing between a co-borrower and a co-signer is the first step toward a stress-free closing. While both roles involve financial liability, they offer very different levels of control over the property. A co-borrower is usually an occupant who shares ownership and appears on the property title. In contrast, when you are co signing a mortgage loan as a co-signer, you are essentially a ghost on the title. You have no legal claim to the equity or the home itself. You are simply the financial guarantor. As the Federal Trade Commission guide on co-signing points out, this means you take on the full risk of the debt without the benefit of owning the asset.

Conventional and Jumbo Loan Considerations

Conventional and Jumbo loans have their own set of rules for non-occupant co-signers. For 2026, the conforming loan limit for most Florida counties is $832,750. If you are co-signing a mortgage loan for a high-value property that exceeds this limit, you’re entering Jumbo loan territory. These loans often demand higher credit scores from co-signers, sometimes 700 or above, and extensive proof of liquid reserves. One of the biggest risks is the impact on your Debt-to-Income (DTI) ratio. Even if the primary borrower makes every payment on time, Florida lenders will count that entire payment against your income. This can drastically reduce your own borrowing power if you decide to buy another property in Palm Bay or Viera later.

Making the right choice between these roles ensures the process remains fast, enjoyable, and consistent. To get a personalized look at how these loan types affect your credit and future goals, Contact a Mortgage Expert today.

Evaluating the Risks and Rewards for the Co-signer

Helping a loved one purchase a home in the Space Coast is a powerful legacy. It allows them to build equity and financial independence in a market that saw around 1,000 homes sold in March 2026. Beyond the emotional reward, your strong credit profile can be a major asset. By co signing a mortgage loan, you might help the primary borrower qualify for a better interest rate tier, potentially saving them thousands over the life of the loan. However, this generosity requires a clear eyes approach. You should review what to know before co-signing to ensure you aren’t sacrificing your own financial future for someone else’s front door.

Your credit profile is the primary “insurance policy” for the lender. If the borrower misses just one payment by 30 days, your credit score could drop instantly. This happens because the lender reports the delinquency on your credit history exactly as they do for the primary borrower. At Morgan Financial, we want your experience to be fast, enjoyable, and consistent. That means identifying these risks early so you can set up safeguards before the first payment is ever due.

The Impact on Your Future Borrowing Power

If you plan to buy your own property in Brevard County next year, that co-signed debt could be a major hurdle. Lenders generally include the full monthly mortgage payment in your Debt-to-Income (DTI) ratio. This remains true even if you aren’t the one writing the check every month. There is a strategic way around this known as “contingent liability” exclusion. If you can provide 12 months of cancelled checks or bank statements proving the primary borrower paid the mortgage from their own account, some lenders may exclude that debt from your DTI. This is a vital strategy for anyone who doesn’t want their borrowing power frozen for the next 30 years.

Protecting Your Relationship and Credit

Successful co-signing depends on radical transparency. You shouldn’t wait for a late notice to find out there’s a problem. We recommend setting up automatic payments from the borrower’s account to ensure the mortgage is never late. It’s also wise to have a “What if” plan. If the borrower faces a job loss or medical emergency, you need to know immediately so you can step in before the credit damage occurs. Treating this as a professional business arrangement rather than just a family favor keeps the relationship healthy and your credit score protected.

The Florida Factor: Local Market Nuances in Brevard County

Melbourne and the wider Space Coast present a unique set of financial variables that national “big box” lenders often overlook. When you are co signing a mortgage loan in Brevard County, the math involves more than just the principal and interest. You must account for Florida’s specific insurance landscape and property tax structure. For example, homeowners insurance on the Space Coast often requires wind mitigation inspections and, in certain areas of Palm Bay or Titusville, flood insurance. A local firm understands these costs upfront, ensuring your debt-to-income ratio is calculated accurately from the start. You can find more about choosing the right partner in our guide to the Best Home Loan Lenders in FL.

The local market is currently in a healthy, balanced state. In March 2026, around 1,000 homes were sold in Brevard County with an average of 39 days on the market. When you are cosigning a mortgage loan, you are betting on the local economy as much as the borrower. Because the Space Coast is a hub for aerospace and technology, the demand for housing remains resilient. This stability protects the value of the asset you are guaranteeing, making the arrangement a more secure long-term play than in more volatile regions.

Why Local Expertise Matters for Co-signers

Local expertise is vital because of nuances like the Florida Homestead Exemption. While co-signers don’t typically live in the home, the primary borrower’s ability to claim this exemption significantly lowers the annual tax burden. National lenders might not factor this into the initial qualification, potentially overestimating the monthly payment. We provide a process that is fast, enjoyable, and consistent by handling these Brevard-specific details with precision. This local focus ensures there are no surprises at the closing table, keeping the experience stress-free for both you and your family member.

Brevard County Market Context

Growth trends in Titusville and Viera make homeownership a sound investment in 2026. Steady appreciation in home values means the primary borrower builds equity faster. This equity is the key to your exit strategy. As the property value rises, the borrower’s loan-to-value ratio improves. This makes it much easier for them to qualify for a refinance in their own name later. By choosing a home in a high-growth area of Brevard County, you are shortening the time you’ll need to remain on the loan. If you’re ready to explore how the local market affects your role as a guarantor, Speak with a Florida Mortgage Expert today.

The Exit Strategy: How to Stop Being a Co-signer

Co-signing is a strategic financial bridge, not a permanent anchor. While you entered the agreement to help a loved one, your ultimate goal should be a clean exit once the primary borrower is financially stable. When you are co-signing a mortgage loan, you need a documented plan to be removed from the debt. The most common and effective method is a professional refinance. This process allows the primary borrower to take out a new loan in their name only, using the proceeds to pay off the original mortgage and releasing you from all future liability. This is the cornerstone of our Easy Refinance approach, designed to make the transition as smooth as the original purchase.

For those who helped a veteran family member, a loan assumption is another path, though it is considerably rarer in the current market. In a VA loan assumption, a new qualified borrower takes over the existing mortgage terms. While this preserves the original interest rate, it requires strict lender approval and a thorough review of the new borrower’s credit. If neither refinancing nor assumption is viable, selling the property remains the definitive way to clear the debt from your record. In Florida’s resilient market, selling a home often provides enough proceeds to satisfy the mortgage entirely, leaving your credit report clear for your next personal investment.

Preparing the Borrower to Fly Solo

The transition starts long before the refinance application. The primary borrower must prove they can handle the debt-to-income (DTI) ratio on their own. During the first few years of the loan, the borrower should focus on increasing their income and reducing other debts, like car payments or credit cards. Improving their credit score is equally vital. A higher score ensures they qualify for the best possible rates when it’s time to remove your name. We recommend using a Mortgage Calculator to estimate what their new solo payments will look like based on current 2026 market rates.

Timeline for Removal

Lenders typically look for a consistent history of on-time payments before they’ll approve a refinance that removes a co-signer. A period of 12 to 24 months of perfect payment history is the standard benchmark. This history proves to the lender that the primary borrower is reliable. Equity growth in Brevard County also plays a major role. As property values in Melbourne and Viera rise, the borrower’s loan-to-value ratio improves, making the refinance much easier to approve. Once these conditions are met, the process becomes fast, enjoyable, and consistent. When you’re ready to start the transition, Contact Morgan Financial to discuss refinance options and reclaim your full borrowing power.

Secure Your Financial Future While Helping Family

Helping a loved one enter the Florida housing market is a significant achievement. Success depends on understanding that your legal obligation covers 100% of the debt and establishing a firm exit strategy from day one. By focusing on a 12 to 24 month timeline for the primary borrower to build credit and equity, you protect your own borrowing power for future investments in Melbourne or Viera. When you’re co signing a mortgage loan, you need a partner who understands these local nuances and legal realities.

At Morgan Financial, we pride ourselves on being veteran owned and operated. We’ve earned our reputation as Florida’s Trusted Mortgage Experts by making the lending process Fast. Enjoyable. Consistent. Whether you’re navigating a Conventional purchase or a complex VA joint loan, our team provides the steady hand you need to avoid relationship strain and credit damage. Don’t leave your financial legacy to chance. Talk to a Florida Mortgage Expert about Co-signing Options today. We’re here to ensure your path to homeownership is as rewarding as the destination itself.

Frequently Asked Questions

Can I be removed from a mortgage I co-signed?

You can be removed, but the process isn’t automatic. The primary borrower must refinance the mortgage into a new loan in their name only. This typically requires them to prove they can handle the payments alone and usually necessitates 12 to 24 months of perfect payment history. Our team makes this transition fast, enjoyable, and consistent when the borrower is ready to fly solo.

Does co-signing a mortgage affect my ability to get a car loan?

Yes, co-signing will increase your Debt-to-Income (DTI) ratio. Lenders view the entire mortgage payment as your legal obligation, which reduces the amount of income you have available for other financing. This could lead to a lower loan limit or a higher interest rate when you apply for a vehicle or other personal credit lines.

What credit score does a co-signer need for a mortgage in Florida?

In the 2026 Florida market, most lenders require co-signers to have a credit score of at least 700. If you are helping a loved one secure a Jumbo loan for a high-value property on the Space Coast, that requirement often jumps to 720 or higher.

Will co-signing a mortgage for my child affect my taxes?

Generally, co-signing does not change your tax situation because you don’t have ownership interest in the property. Since you aren’t on the title, you cannot claim mortgage interest deductions or the Florida Homestead Exemption. You are simply a financial guarantor. We recommend consulting a tax professional to discuss how this debt interacts with your specific financial profile.

What happens if the primary borrower dies?

You become 100% responsible for the remaining balance of the loan immediately. The debt does not disappear upon the borrower’s death, and the lender will look to you for all future payments. Many families choose to secure a life insurance policy for the primary borrower that covers the mortgage amount to prevent this financial burden from falling solely on the co-signer.

Can a co-signer be a friend instead of a family member?

Yes, a co-signer can be a friend for Conventional and Jumbo loans. While some specific programs prefer relatives, many private lenders allow “non-occupant co-borrowers” who are not related to the primary buyer. However, the legal risks remain identical. You are still fully liable for the debt regardless of your relationship with the person living in the home.

Is a co-signer’s income used to qualify for the loan amount?

Yes, your income is added to the primary borrower’s income to strengthen the application. This combined total helps lower the overall DTI ratio, which can lead to a higher total loan approval. When co signing a mortgage loan, your stable Florida earnings act as the catalyst that allows the borrower to qualify for a home they couldn’t afford on their own.

How long does a co-signer stay on a mortgage?

A co-signer remains on the mortgage for the entire life of the loan, which is often 30 years. There is no point where you “drop off” the contract automatically. You only stop being a co-signer if the loan is paid in full, the property is sold, or the primary borrower successfully refinances the debt into their own name.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.