Your VA home loan benefit isn’t a single-use coupon that expires the moment you sign your first mortgage. It is a powerful, repeatable, and lifetime financial tool designed to grow with your family. Many veterans on the Space Coast ask, “can I use my VA loan more than once?” as they look to upgrade their lifestyle or build real estate wealth. The answer is a definitive yes.

It is natural to feel protective of a current low rate or confused by the complex entitlement jargon that national lenders often use. You earned this benefit through service. You shouldn’t have to worry about losing it just because you need more space or a new view around Florida. We understand the stress. We know the process. We deliver results.

This guide will show you exactly how to unlock your entitlement multiple times, even if you want to keep your current home as an investment. You’ll learn how to restore your eligibility, discover the rules for holding two VA loans at once, and see how all of this impacts your next move. Our Brevard County lending specialists are here to handle the complex paperwork so you can focus on your future. It’s time to maximize your benefits with a team that values your service.

Key Takeaways

- Your VA loan is a permanent financial asset that offers unlimited reuse, providing a lifetime of homeownership opportunities.

- Discover the specific strategies for how can I use my VA loan more than once to build wealth and secure your next Space Coast property.

- Learn how to leverage bonus entitlement to buy a new home while keeping your current residence as a high-value rental.

- Understand the restoration process to regain your full zero-down payment benefits after selling your previous home.

- Gain a competitive edge in the Melbourne and Palm Bay markets by working with a dedicated local expert who simplifies the complex paperwork.

Can I Use My VA Loan More Than Once? The Short Answer is Yes.

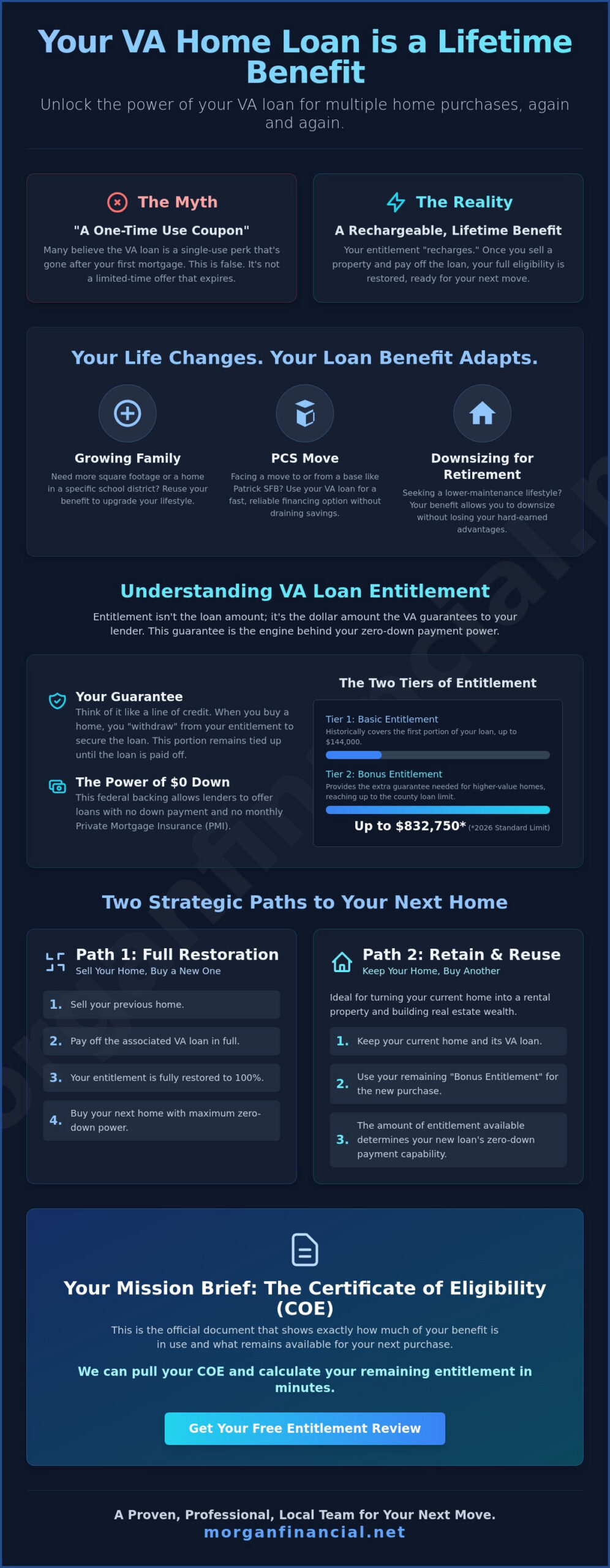

Many veterans believe their mortgage benefit is a one-and-done deal. It isn’t. The VA loan program is a lifetime entitlement that grows with you. You can use the benefit as many times as you want throughout your life. There is no expiration date on your service. Whether you bought your first home ten years ago or just last year, the answer to “can I use my VA loan more than once” is a definitive yes. At Morgan Financial, we specialize in helping Florida veterans navigate these repeat benefits. We’re fast, enjoyable, and consistent!

The Myth of the One-Time Use

The misconception that this is a single-use perk often stems from confusing the loan with one-time grants or limited-time military offers. Some borrowers worry that once they’ve paid off their mortgage, the benefit is exhausted. That is simply false. Your entitlement actually recharges. Once you sell a property and pay off the associated loan in full, your eligibility is restored. It isn’t gone; it’s just waiting for your next move. This “recharge” happens every time you clear the previous obligation. It allows you to maintain the same zero-down payment power for every home you buy in the future.

Why Veterans Choose to Reuse Their Benefits

Life changes fast on the Space Coast, and your housing needs change with it. We see veterans reuse their benefits for a variety of strategic reasons. Growing families in Viera often need more square footage and access to specific school districts. Active-duty members facing a PCS move to or from Patrick Space Force Base need a reliable, high-speed financing option that doesn’t drain their savings. Others are looking to downsize for retirement in Satellite Beach or Indialantic, seeking a low-maintenance lifestyle without losing their hard-earned advantages. The flexibility of this program allows you to transition between these life stages seamlessly. You don’t have to settle for a conventional loan with a high down payment just because you’ve used your VA benefits before. You earned this advantage. Use it.

Navigating repeat benefits requires precision and local insight. You need a team that knows the Brevard County market and the specific VA guidelines. Check out our VA loan resource for more detailed insights into how these benefits work. We handle the heavy lifting and the complex paperwork so you can focus on your next home.

Understanding VA Loan Entitlement: Tier 1 and Tier 2 Explained

Entitlement is the heartbeat of the VA home loan lifetime benefit. It isn’t the total amount of money you can borrow; rather, it is the specific dollar amount the VA guarantees to your lender if you default. This federal backing is the engine that allows you to buy a home with no down payment and no monthly mortgage insurance. When you ask, “can I use my VA loan more than once,” you are really asking about the status of this guarantee. Understanding how it is divided into two distinct tiers is the key to mastering your buying power.

How Entitlement Works Like a Credit Line

Think of your VA entitlement like a specialized bank account or a line of credit. When you use a VA loan to buy a property, you “withdraw” a portion of that guarantee to secure the mortgage. That portion remains “tied up” as long as you own the home and hold the loan. If you still have a balance left in your “entitlement account,” you can use it to buy another home simultaneously. Tier 1, or basic entitlement, historically covers loans up to $144,000. While that figure doesn’t go far in the current Florida market, it works in tandem with Tier 2. Tier 2 entitlement is the bridge to zero-down luxury homes, providing the extra guarantee needed for properties that reach the 2026 standard county limit of $832,750 or higher.

Checking Your Certificate of Eligibility (COE)

Your Certificate of Eligibility is the only document that provides an official record of your entitlement status. For repeat buyers, the COE is the first step in the mission. It acts as a ledger, showing exactly how much of your benefit is currently in use and what remains available for your next purchase. On paper, a “Restoration of Entitlement” appears as a reset of these figures once a previous VA loan is paid in full and the property is sold. It is a clean slate for your next move.

You don’t need to struggle with government portals or wait weeks for an answer. Our team of regional specialists can pull your COE for you in minutes. We analyze the data, calculate your remaining “bonus entitlement,” and help you plan a move to Viera or Indialantic with total clarity. We move fast. We stay local. We get results. If you are ready to see what your service has earned you, reach out to a local expert today for a comprehensive entitlement review.

Two Strategic Ways to Reuse Your VA Loan Benefits

When exploring the question, “can I use my VA loan more than once,” you’ll find two primary paths to success. Each strategy offers unique advantages depending on your financial goals and your timeline. Whether you want a clean slate for your next purchase or you’re ready to start a real estate portfolio, your benefit is flexible enough to accommodate your vision. We help you choose the right path with speed and precision.

Scenario A: Selling and Restoring Entitlement

Selling your current home and paying off the existing mortgage is the most straightforward way to reuse your benefit. This process results in a “Full Restoration” of your entitlement. Once the VA receives proof that the prior loan is satisfied, your $0 down purchasing power resets to its maximum capacity. This is often the cleanest way to buy your next Space Coast home because it removes all previous obligations from your Certificate of Eligibility.

There is also a “one-time restoration” rule for those who want to keep their home. If you have paid off your VA loan in full but still own the property, you can request to have your entitlement restored once. This allows you to use your full benefit for a new primary residence while keeping the original home as a mortgage-free asset or a high-performing rental property.

Scenario B: The Second Tier (Multiple Concurrent Loans)

You don’t always have to sell your current house to use your VA benefit again. By leveraging “Bonus Entitlement,” you can actually have two VA loans at once. This is the ultimate “Keep and Rent” strategy for building Florida real estate wealth. You keep your first home, turn it into a rental, and use your remaining Tier 2 entitlement to secure a second primary residence.

Calculating your remaining entitlement for a second purchase involves looking at the 2026 standard loan limit of $832,750. If you have enough “bonus” left, you could still achieve a $0 down payment on a second home. For high-value Melbourne properties, this often opens the door to “VA Jumbo” opportunities. These loans allow you to exceed standard limits while maintaining the competitive rates and terms unique to the VA program. You must follow these core requirements for concurrent loans:

- Primary Occupancy: You must intend to live in the new home as your main residence.

- Sufficient Entitlement: Your remaining Tier 2 balance must cover at least 25% of the new loan amount to avoid a down payment.

- Lender Approval: You must still meet credit and income requirements for both obligations.

Understanding these scenarios is the first step toward a smarter move. Our team at Morgan Financial specializes in these complex calculations to ensure you maximize every dollar of your benefit. If you’re ready to see how much “bonus” you have left, you can start your purchase journey here. We handle the math so you can find the home.

Navigating the Space Coast Market with a Repeat VA Loan

The Space Coast real estate market moves at a high-speed pace. National call-center lenders often struggle with the specific property tax structures and localized insurance requirements of Brevard County. When you ask, “can I use my VA loan more than once,” you need a partner who truly understands the local landscape. Melbourne and Palm Bay are high-growth areas where a strategic offer is the difference between winning a home and starting your search over. We provide that edge. We understand the mission and we deliver results.

Loan Limits in Brevard County

Many veterans are surprised to learn that for those with full entitlement, the VA has officially removed loan limits. This means your purchasing power is only capped by your income and credit score, not by a government-mandated ceiling. However, these limits still play a crucial role if you intend to keep your current home while buying another. If you have a current active VA loan, the standard 2026 conforming limit of $832,750 becomes the baseline for calculating your zero-down power on a second purchase. This calculation is vital for buyers looking in Merritt Island or Rockledge, where property values often require sophisticated entitlement management. We analyze your specific situation to ensure your bid is both accurate and competitive.

The Morgan Financial Advantage

We are a veteran-owned firm that takes personal responsibility for the financial well-being of our neighbors. Our three-word promise to every Space Coast veteran is simple: Fast, Enjoyable, and Consistent. This isn’t just a brand anchor; it’s the standard for how we process every file. Our Stronger than a Pre-Approval process gives repeat buyers a massive advantage by completing the heavy underwriting work before you even make an offer. This turns your VA loan into a position of strength that sellers in Brevard County recognize and trust. It’s a proven way to stand out in a crowded market.

Strategic bidding requires more than just a pre-approval letter. It requires a local expert who can explain the strength of your VA benefit to a listing agent in Indialantic or Viera. We act as your steady hand in this complex landscape, ensuring your transition to a second or third home is a positive emotional experience. Review our VA Loan Resource for more local market insights. If you’re ready to secure your next home with a team that values your service, contact our local lending specialists today to start your advantage.

Steps to Secure Your Next VA Loan in Florida

Securing a second or third mortgage shouldn’t feel like a battle. You already know the answer to can I use my VA loan more than once is a clear yes, if eligible and qualified. Now you need a logical roadmap to execute that vision. Our process is designed to move you from curiosity to closing with high-energy efficiency. We provide the steady hand you need in a complex landscape.

The journey to your next Space Coast home follows a proven, step-by-step progression:

- Step 1: Connect with a Local Expert. Speak with a regional specialist at Morgan Financial who understands the nuances of repeat VA benefits.

- Step 2: Entitlement Review. We pull your Certificate of Eligibility (COE) and calculate your remaining Tier 1 and Tier 2 status.

- Step 3: Strategic Pre-Approval. We verify your income and credit to determine your maximum zero-down purchasing power.

- Step 4: Close with Confidence. Find your home in Melbourne, Palm Bay, or Viera and let us handle the heavy lifting.

Preparing Your Documentation

Repeat buyers have a slightly different paperwork trail than first-time users. If you have sold a previous home, you’ll need the HUD-1 or Closing Disclosure to prove the prior VA loan was paid in full. This allows us to initiate the restoration of your entitlement immediately. You’ll also need updated income verification, including paystubs and W2s, to reflect your current financial strength. To give you a massive advantage in the competitive Florida market, we utilize our Stronger Than a Pre-Approval process. This completes the underwriting work upfront, showing sellers that your financing is rock-solid.

Closing the Deal

The final phase of the mission requires precision. We coordinate with local appraisers who understand VA standards and the specific value of Space Coast real estate. While the VA handles the appraisal assignment, our local knowledge ensures that the timeline stays on track. Behind the scenes, we manage the “Restoration of Entitlement” paperwork with the VA, ensuring your benefits are correctly updated for this purchase and any future moves. We handle the bureaucracy so you can focus on your move.

Your service earned you a lifetime of benefits. Don’t let confusion over entitlement stop you from building wealth or finding a better home for your family. We are ready to handle the complex paperwork and guide you home. If you’re ready to see how can I use my VA loan more than once applies to your specific goals, connect with our local lending specialists today.

Take Command of Your Space Coast Future

Your VA loan benefit is a permanent financial asset that stays with you long after your service ends. You’ve discovered that the answer to can I use my VA loan more than once is a resounding yes. Whether you are upgrading to a larger family home in Viera or building a rental portfolio in Palm Bay, your entitlement is designed to adapt to your changing needs. You can restore your full power after a sale or leverage bonus entitlement to hold two properties simultaneously.

Don’t settle for a national call-center lender that doesn’t understand the unique nuances of the Brevard County market. Morgan Financial is veteran-owned and operated. We are the dedicated specialists in Space Coast VA lending. Our service is Fast. Reliable. Professional. We handle the complex bureaucracy so you can focus on your family’s next chapter. Start your next VA home purchase with Morgan Financial today. Your next move is within reach, and we are here to guide you home with confidence.

Frequently Asked Questions

How many times can I use my VA loan benefit?

You can use your VA loan benefit an unlimited number of times throughout your life. There is no cap on the total number of home purchases you can make using this program. As long as you have remaining entitlement or have restored it after a sale, the benefit remains yours. It is a permanent advantage.

Can I have two VA loans at the same time?

Yes, you can have two VA loans at the same time by utilizing your Tier 2 or “bonus” entitlement. This is a powerful strategy for Space Coast veterans who want to keep their current home as a rental property while moving into a new primary residence. We calculate your remaining eligibility based on the 2026 standard loan limit of $832,750 to determine your zero-down purchasing power.

Do I have to pay back my first VA loan to use it again?

You don’t have to pay back your first VA loan to use the benefit again, but keeping the first loan active will limit the entitlement available for your next home. If you want to use your full, unlimited entitlement for a new purchase, the original loan must be paid in full. If you keep the first loan, you’ll use “partial entitlement” for the second property.

Is there a waiting period between using VA loans?

There is no specific waiting period required by the VA between using one loan and starting the next. You can theoretically close on a new VA loan immediately after selling your previous home and restoring your entitlement. However, you must still meet the lender’s requirements for income, credit, and employment stability for every new application. We move fast to keep your timeline on track.

What happens to my entitlement if I sell my house?

When you sell your house and pay off the VA loan in full, your entitlement is eligible for a full restoration. This process resets your account, allowing you to use your $0 down payment benefit at its maximum capacity for your next move. Our team handles the restoration paperwork behind the scenes to ensure your Certificate of Eligibility is updated quickly. Effortless. Professional. Local.

Can I use a VA loan again after a foreclosure or short sale?

Yes, you can use a VA loan again even after a foreclosure or short sale, though a waiting period usually applies. Most lenders require a two-year gap following the completion of the foreclosure or short sale before you can qualify for a new VA mortgage. You may also have diminished entitlement if the VA suffered a loss on your previous loan. We analyze your status to find the best path forward.

Do I have to pay the VA funding fee every time I use the loan?

You generally pay the VA funding fee every time you use the benefit, and the rate increases for subsequent uses. For a subsequent use with 0% down in 2026, the fee is 3.3%. However, you are exempt from this fee if you receive disability compensation for a service-connected issue. We help you verify your exemption status early to ensure you aren’t paying more than necessary.

How do I restore my VA loan entitlement?

To restore your entitlement, you must submit a formal request to the VA after your previous loan is paid in full. This usually requires providing a copy of the closing disclosure from your sale. When you ask can I use my VA loan more than once, the restoration process is the mechanical key that unlocks your recurring benefits. We handle this documentation for you to ensure a smooth transition.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.