That 3% interest rate you are chasing might actually be the most expensive mistake you make this year. While the idea of an assumption sounds like a financial win, the reality of the 2026 Florida market is often far more complex. When comparing an assumable va loan vs. new va loan, many buyers discover that the massive cash required to cover the equity gap outweighs the monthly savings. You need clarity. You need speed. You need a partner who knows the Space Coast. Fast. Enjoyable. Consistent.

It’s natural to feel frustrated by current rates, especially when you’re trying to maximize your hard-earned benefits. We agree that finding the lowest payment is a priority, but the process shouldn’t be a source of constant stress. This article will compare the long-term savings of an assumable VA loan against the speed and flexibility of a new VA loan to find your best path to homeownership. We’ll explore how to preserve your VA entitlement and why a new loan often provides the fast, reliable closing process you deserve without the typical 90-day waiting period.

Key Takeaways

- Master the fundamental differences between inheriting a seller’s existing interest rate and securing a fresh 2026 loan with full benefits.

- Uncover why the “equity gap” in Space Coast markets like Palm Bay and the beaches might require six figures in cash to close an assumption.

- Protect your future borrowing power by learning how a substitution of entitlement keeps veteran sellers whole during the process.

- Evaluate the assumable va loan vs. new va loan trade-off to see if saving on interest is worth a significantly longer closing timeline.

- Use our 2026 decision matrix to choose your best path based on your available cash, move-in schedule, and long-term financial goals.

VA Loan Assumption vs. New VA Loan: The Fundamental Differences

How VA Loan Assumptions Work

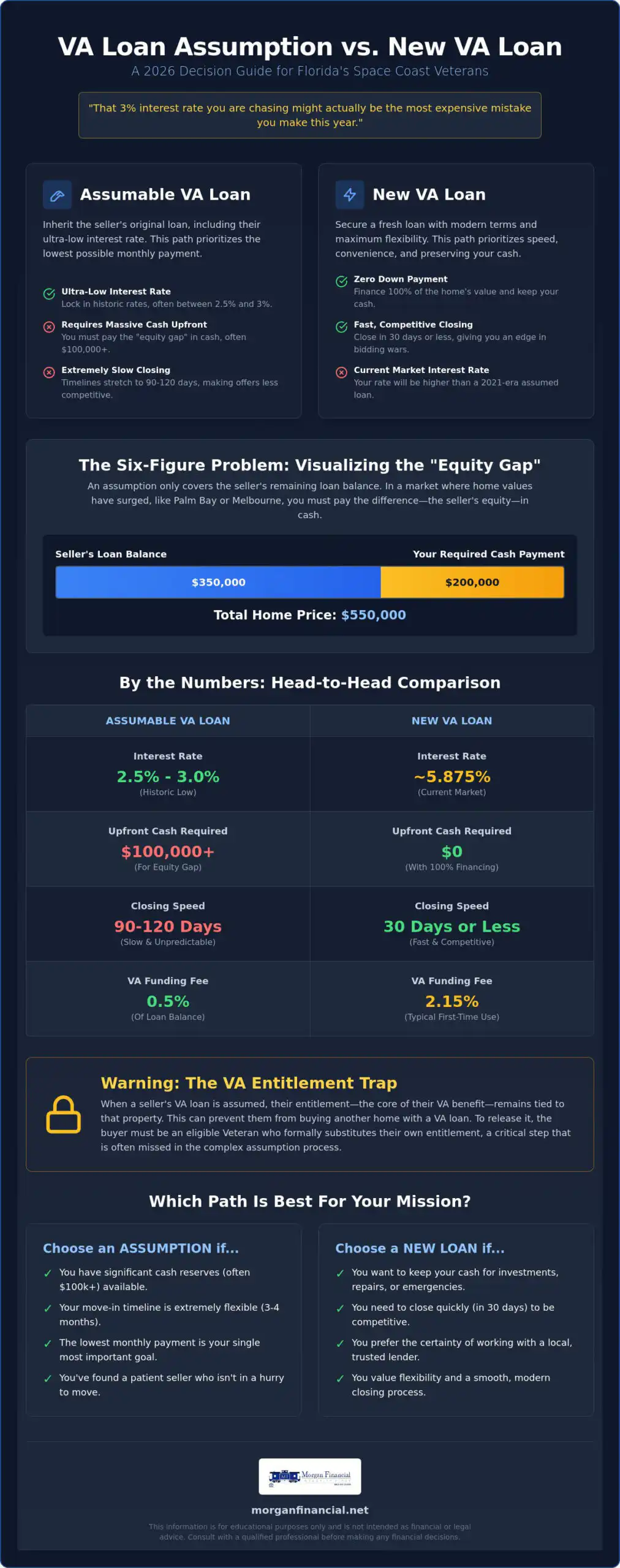

An assumption allows a buyer to step into the seller’s shoes. You take over the existing mortgage balance, the remaining repayment term, and the original interest rate. This is a specific feature of assumable mortgages, which include all VA-backed loans by federal law. If a seller locked in a 3% rate in 2021, you inherit that 3% rate. However, you also take over the exact remaining balance. If the home is worth $500,000 but the loan balance is only $350,000, you must cover that $150,000 "equity gap" in cash. The process is also notoriously slow. Because you are at the mercy of the seller’s existing mortgage servicer rather than choosing your own local partner, timelines often stretch to 60 or even 90 days. It’s a bureaucratic marathon that requires patience and deep pockets.

The Perks of Starting Fresh with a New VA Loan

Choosing a new VA home loan offers a completely different experience. You aren’t limited by the seller’s equity or their previous financial decisions. You start a fresh contract with terms that fit your current life. Consider these advantages:

- Zero Down Payment: You can finance the full purchase price up to the 2026 standard limit of $832,750 without needing six figures of cash to cover an equity gap.

- Lender Choice: You choose who handles your money. You can work with a team that prioritizes transparency, communication, and local expertise.

- Aggressive Timelines: In a market like Melbourne or Palm Bay, speed wins. A new loan can typically close in 30 days or less with a focused local team.

The core trade-off is the interest rate. While you won’t get a 2021 rate, you gain the ability to move quickly and keep your cash in the bank for repairs or investments. For many Florida buyers, the "interest rate win" of an assumption is quickly neutralized by the stress of a three-month closing and the exhaustion of personal savings. We help you weigh these factors with expert VA loan resources tailored to our unique regional landscape. Reliable. Efficient. Proven.

Side-by-Side Comparison: Rates, Costs, and Timelines

Deciding between an assumable va loan vs. new va loan requires a cold look at the numbers. In June 2026, VA purchase rates are sitting around 5.875%, which is a stark contrast to the 2.5% or 3% rates many Florida homeowners secured just a few years ago. On a $400,000 loan, that difference can save you hundreds of dollars every month. However, the interest rate is only one piece of the puzzle. You must also account for the VA funding fee. A new VA loan typically carries a 2.15% fee for first-time use with 0% down, while an assumption fee is a flat 0.5% of the loan balance. On paper, the assumption looks like a landslide victory, but the hidden costs often tell a different story.

The Upfront Cash Requirement

The biggest hurdle in 2026 is the "equity gap." When you assume a loan, you only take over the seller’s existing balance. If a home in Melbourne is selling for $550,000 but the seller only owes $350,000, you have to bring $200,000 in cash to the closing table. Because home values across the Space Coast have surged, these gaps are frequently reaching six figures. While market conditions for assumable mortgages make the low rates attractive, most buyers don’t have that kind of liquid cash sitting in a bank account. You could explore secondary financing to cover the difference, but those second mortgages often come with much higher interest rates that eat away at your primary savings. If you want to keep your cash for renovations or investments, a new loan with 0% down is the superior financial move.

Closing Speed and Market Competitiveness

Speed is currency in the Florida housing market. A new VA loan with a local team can close in 30 days or less. In contrast, an assumption often drags on for 90 to 120 days because you’re forced to work with the seller’s existing national servicer. These large institutions aren’t always motivated to move quickly on a process that doesn’t generate a new loan for them. Many sellers in Palm Bay or Merritt Island won’t even look at an assumption offer because they can’t afford to wait four months to move. If you’re in a bidding war, a Stronger Than A Pre-Approval letter for a new loan carries far more weight than a slow assumption request. If you’re unsure which path fits your timeline, reach out to our team for a personalized comparison. Fast. Reliable. Local.

The Entitlement Trap: What Buyers and Sellers Must Know

Most Veterans understand that their VA loan benefit is a powerful tool for building wealth. However, few realize that this benefit can be accidentally "locked away" for decades during a property transfer. When evaluating an assumable va loan vs. new va loan, the impact on your VA entitlement is the most critical factor for your long-term financial freedom. Your entitlement isn’t just a number on a certificate. It is your ticket to future 0% down homeownership. If you lose it in a bad deal, you lose your edge in the market.

In a standard sale involving a new VA loan, the process is a clean slate. The buyer secures their own financing, and the seller’s entitlement is fully restored the moment the old loan is paid off. Both parties walk away with their benefits intact. An assumption changes this dynamic completely. Unless specific steps are taken, the seller’s entitlement remains tied to the house even after they no longer own it. This "entitlement trap" can prevent a Veteran seller from using their benefits to buy their next primary residence. It’s a high-stakes gamble that requires expert guidance. Fast. Enjoyable. Consistent.

Substitution of Entitlement Explained

To avoid the trap, the buyer must be a Veteran who agrees to a "Substitution of Entitlement." This means the buyer uses their own VA eligibility to replace the seller’s. Substitution of Entitlement is the essential legal maneuver that swaps the buyer’s VA eligibility for the seller’s, ensuring the seller can use their full benefits on their next home. This process requires meticulous paperwork and approval from the VA. If the buyer is a non-Veteran, this substitution cannot happen. In that scenario, the seller’s entitlement stays with the property until the loan is eventually paid off or refinanced. For many, that could mean waiting 25 years to get their benefits back.

Risks for the Seller in an Assumption

Selling your home via assumption to a non-Veteran is a massive risk. Beyond the loss of future benefits, you may face ongoing liability. If the new owner defaults, your credit and your VA eligibility could be severely damaged. Even with a Veteran buyer, the process is complex. If the servicer doesn’t grant a formal "Release of Liability," you remain financially responsible for the debt. This is why many local experts suggest a new VA loan as the safer path. It provides a guaranteed exit strategy and protects your financial future. If you are a seller in Melbourne or Palm Bay, don’t let your benefits get tied up in a bureaucratic nightmare. Contact our team to discuss how to keep your entitlement secure while moving forward with confidence.

Navigating the Space Coast Market: Local Considerations

When weighing an assumable va loan vs. new va loan in Brevard County, geography is your biggest variable. The 2026 real estate market here moves with a specific energy, driven by the aerospace boom and our unique coastal landscape. While the allure of a low interest rate is strong, the local reality of home appreciation often dictates your strategy. You need a partner who understands why a deal in Titusville looks completely different than one on the beaches. Fast. Reliable. Local.

Brevard County Equity Analysis

Florida’s appreciation rates through early 2026 have created a massive divide in assumption feasibility. In areas like Titusville, where entry-level housing is more common, the equity gap might be manageable for a buyer with some savings. However, on Merritt Island and the beaches, "The Gap" has become a significant hurdle. Many homeowners who bought or refinanced in 2021 now sit on hundreds of thousands of dollars in equity. If you want to assume their loan, you must bring that entire difference to the closing table in cash. Most buyers find this requirement prohibitive, especially when the standard VA loan limit for 2026 has increased to $832,750. You can use our mortgage calculators to see if the monthly savings of an assumption actually justify depleting your liquid assets. Often, keeping that cash for investments or home improvements provides a better long-term return than chasing a 3% rate.

The Speed Advantage in Florida Real Estate

Real estate moves at the speed of light in Melbourne and Palm Bay. Sellers here are often looking for a clean, certain exit, especially if they are relocating for work at the Space Center or Patrick Space Force Base. A 21-day close is the gold standard that wins bidding wars. Dealing with national "big bank" servicers on an assumption is the opposite of that. These institutions frequently drag the process out for 90 days or longer, leading to extreme frustration for everyone involved. Sellers don’t want to leave their moving plans in limbo while a detached corporate office slowly reviews paperwork. We take a different approach. By choosing a new VA loan through Morgan Financial, you benefit from a streamlined, logical process designed to get you into your home without the wait. Use our VA loan resource to evaluate how local listings fit your specific goals. If you’re ready to secure a home on your own timeline, contact our team today to start your fast, reliable closing process.

Decision Matrix: Which Path Should You Take?

The choice between an assumable va loan vs. new va loan ultimately comes down to your personal balance sheet and your move-in urgency. In the 2026 Florida market, there is no one-size-fits-all answer. You must weigh the long-term interest savings against the immediate need for liquid capital and a predictable closing date. Making the wrong move can tie up your VA entitlement for decades or cost you the home of your dreams in a competitive bidding war. You need a clear strategy. You need a partner who understands the local stakes. Fast. Reliable. Local.

- Choose an Assumable VA Loan IF: You have significant cash reserves to cover the equity gap, your timeline allows for a 4-month closing process, and both the buyer and seller are Veterans looking to swap entitlement.

Many Space Coast buyers are opting for a hybrid approach. They secure a new VA loan today to win the house and keep their cash liquid for other investments. If market rates drop later in 2027 or 2028, they can utilize an Easy Refinance to lower their monthly payment. This strategy provides the immediate gratification of homeownership without the bureaucratic nightmare of a slow assumption. It’s a logical, streamlined path to building wealth in Brevard County.

When Assumption is the Clear Winner

While the equity gap makes assumptions difficult for many, they remain a powerful tool in specific scenarios. If you are navigating a family transfer or a divorce situation where speed is less critical, the savings from a legacy interest rate are hard to beat. You should also consider an assumption if the home has low equity, though this is increasingly rare in 2026 Florida. Always calculate your break-even point. If the cash required to cover the equity gap takes 20 years to "earn back" through monthly savings, a new loan is almost always the smarter financial play. We help you run these numbers with precision and transparency.

Starting Your Journey with Morgan Financial

Navigating the complexities of VA eligibility and entitlement restoration requires a steady hand. Our team provides the regional authority and professional confidence you need to move forward. We don’t just process loans; we act as your local guide through the entire Space Coast real estate landscape. Whether you are buying in Melbourne, Palm Bay, or the beaches, we ensure your interests are protected at every turn. Ready to see which path fits your budget? Contact our Melbourne-based team to run your specific numbers and secure your fast, reliable closing process today.

Take the Next Step Toward Your Space Coast Home

Choosing the right mortgage path is about more than just a single interest rate. It’s about protecting your financial flexibility and your future borrowing power. We’ve explored how the massive equity gap and entitlement risks can turn a seemingly low-rate assumption into a long-term burden. Securing a new VA loan ensures you keep your cash liquid and your timeline moving forward without the stress of bureaucratic delays. Your analysis of an assumable va loan vs. new va loan should lead you to the path that offers the most certainty and speed for your family.

As local Space Coast experts since 2002, we are a Veteran-owned and operated team of specialists in VA entitlement restoration. We take pride in being the steady hand that guides our neighbors through complex financial landscapes. Fast. Reliable. Local. This is the standard you deserve when using the benefits you worked so hard to earn.

Ready to secure your Space Coast home? Start your VA Loan application with Morgan Financial today!

You’ve earned these benefits. Let’s make sure you use them to their full potential and move into your new home with total confidence.

Frequently Asked Questions

Can a non-Veteran assume a VA loan in Florida?

Yes, any creditworthy individual can assume a VA loan, regardless of military service. However, there is a major catch for the seller. If a non-Veteran assumes the mortgage, the seller’s VA entitlement remains tied to the property until the loan is paid off. This is a critical point to consider when weighing an assumable va loan vs. new va loan. The buyer must still meet the specific credit and income requirements set by the existing lender.

How long does the VA loan assumption process actually take in 2026?

The assumption process typically takes between 45 and 90 days. Some national mortgage servicers may take even longer because they aren’t structured for speed. This is significantly slower than the 30-day timeline you can expect with a new VA purchase loan. If you need to move quickly, an assumption might not be the best fit. Fast. Reliable. Local. Those are traits you’ll find with a new loan rather than a bureaucratic assumption.

Do I still need a down payment for a new VA loan if I’ve used one before?

No, you don’t need a down payment for subsequent use as long as you have remaining entitlement. The VA funding fee for subsequent use with 0% down is 3.3% in 2026. However, if you choose to put at least 5% down, that fee drops to 1.5%. This flexibility allows you to keep your cash in the bank while still securing a competitive interest rate on a fresh mortgage.

What is the ‘equity gap’ and how do I pay for it during an assumption?

The equity gap is the difference between the home’s purchase price and the seller’s remaining loan balance. You must pay this entire amount in cash at the time of closing. In high-demand areas like Merritt Island or the beaches, this gap can easily reach six figures. Most buyers cover this requirement using personal savings or the proceeds from selling a previous home. There’s no 0% down option for an assumption if the home has gained value.

Will my VA entitlement be restored immediately after I sell via assumption?

Your entitlement is only restored immediately if the buyer is a Veteran who agrees to a substitution of entitlement. If the buyer is a non-Veteran, your entitlement stays with the house. This prevents you from using your full VA benefits on your next home purchase. A new VA loan avoids this trap entirely by paying off your old debt and releasing your entitlement the day you close.

What are the closing costs for an assumable VA loan vs. a new one?

Assumption closing costs are usually lower because you aren’t paying for a full loan origination. The primary cost is a 0.5% VA funding fee based on the existing loan balance. A new VA loan includes a higher funding fee, typically 2.15% for first-time use, along with standard lender and third-party fees. While the assumable va loan vs. new va loan cost comparison favors the assumption on paper, the massive cash required for the equity gap is the real financial hurdle.

Can I get a second mortgage to cover the equity gap on an assumption?

Yes, it’s possible to get a second mortgage to cover the gap, but it’s difficult. Many lenders won’t take a second position behind an assumed VA loan. These secondary loans also carry much higher interest rates than the primary mortgage. If you have to borrow the equity gap at 9% or 10%, your total monthly payment might be higher than if you had simply taken a new VA loan at today’s market rates.

Is there a VA funding fee on an assumed loan?

Yes, there is a mandatory 0.5% VA funding fee on all assumed loans. This fee is calculated based on the remaining principal balance at the time of the transfer. It’s a flat fee that applies to both Veteran and non-Veteran buyers. You must pay this fee in cash at closing. While it’s lower than the fee for a new loan, it’s still a cost that needs to be factored into your total move-in budget.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.