When you’re navigating the home loan process in Melbourne, Florida, you’ll encounter many new terms. One name that often appears in the fine print is Freddie Mac. While you’ll work directly with a local lender like Morgan Financial, understanding Freddie Mac’s role is key to grasping how you can secure a competitive mortgage for your Space Coast home.

Freddie Mac is the invisible engine that provides the liquidity local Florida lenders need to keep mortgages fast, enjoyable, and consistent. Let’s break down what that means for you.

What is Freddie Mac? Defining the Invisible Engine of Florida Real Estate

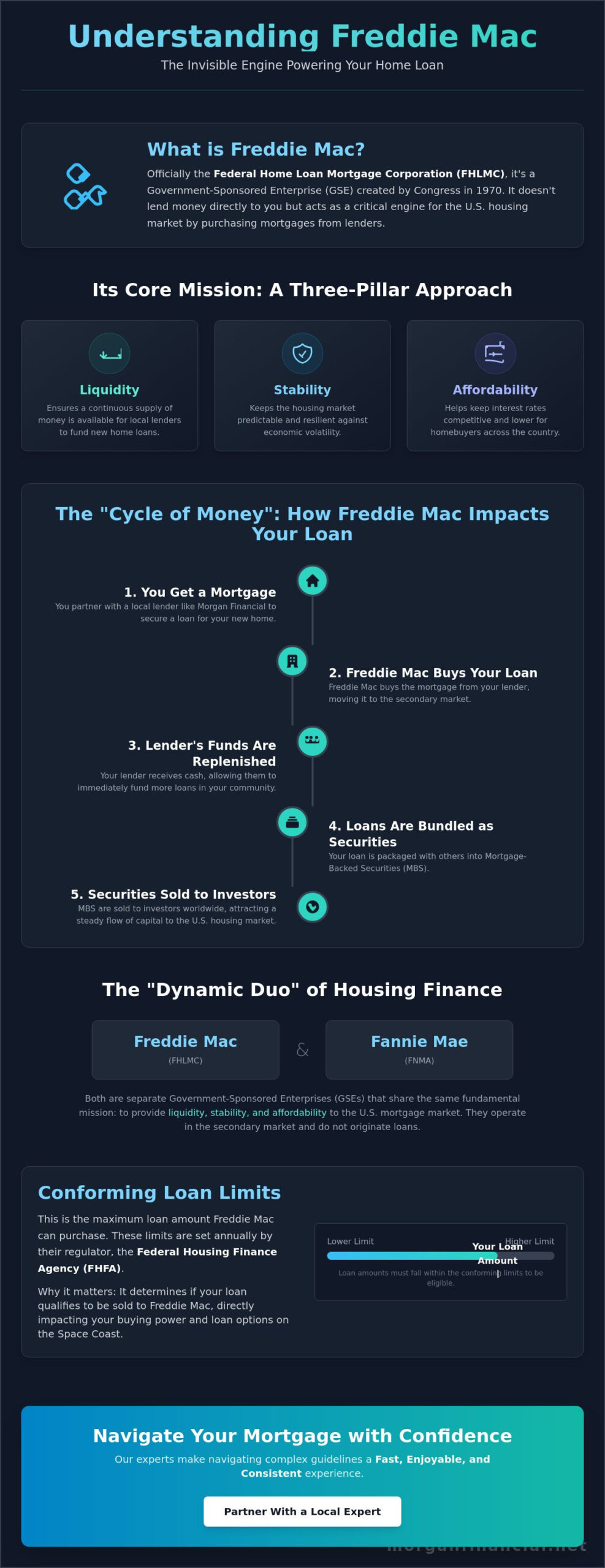

At its core, Freddie Mac is a company that keeps money flowing through the housing market so that lenders can continue to offer home loans to qualified buyers. It’s a crucial piece of the national mortgage puzzle that directly impacts your ability to buy a home in Brevard County.

- Freddie Mac is a Government-Sponsored Enterprise (GSE) created by the U.S. Congress in 1970.

- Its official name is the Federal Home Loan Mortgage Corporation (FHLMC).

- In simple terms, Freddie Mac is a major player in the secondary mortgage market that buys home loans from lenders like banks and mortgage companies.

- Crucially, you do not apply for a loan from Freddie Mac directly. You work with a local expert like Morgan Financial, who originates the loan according to Freddie Mac’s standards.

The Core Mission: Liquidity, Stability, and Affordability

Freddie Mac’s work is guided by three main goals that benefit homebuyers across the country, including right here in Florida:

According to Freddie Mac, this is a well-documented area of ongoing research and practical application.

- Liquidity: By purchasing mortgages from lenders, Freddie Mac frees up cash for those lenders. This ensures there is always a fresh supply of money available for the next family looking to buy a home in our community.

- Stability: It helps keep the housing market predictable, even during economic shifts. This creates a more stable environment for both borrowing and lending.

- Affordability: By packaging loans into trusted investments called mortgage-backed securities (MBS), Freddie Mac makes U.S. mortgages a safe bet for global investors. This high demand helps keep interest rates lower for everyone.

Is Freddie Mac a Government Agency?

This is a common point of confusion. Freddie Mac is not a direct government agency but a “Government-Sponsored Enterprise” (GSE). This hybrid status allows it to operate like a private company while fulfilling a public mission.

- It is a publicly traded company, but it operates under a congressional charter.

- The Federal Housing Finance Agency (FHFA) provides strict oversight and regulation to ensure it operates safely and serves the housing market’s best interests.

- This unique structure helps reduce risk in the mortgage market, which translates into lower borrowing costs for Brevard County homebuyers.

How Freddie Mac Keeps Mortgage Money Flowing in Brevard County

Imagine a local bank only had a set amount of money to lend. Eventually, it would run out, and no one else could get a loan. Freddie Mac prevents this through a simple but powerful “Cycle of Money.”

- You secure a “conforming” conventional loan from a local Florida lender like Morgan Financial to buy your home.

- After your loan closes, Freddie Mac buys that loan from your lender.

- Your lender now has its cash back, plus a small profit, which it can immediately use to fund the next family’s home purchase in Palm Bay or Titusville.

- This continuous cycle ensures that mortgage funds are always available at the local level, making the market reliable and efficient.

The Secondary Mortgage Market Explained

The mortgage world has two main parts. The primary market is where you interact directly with your lender. The secondary market is the behind-the-scenes powerhouse where Freddie Mac operates.

Research published by FDIC Affordable Mortgage Lending Guide shows that this is a well-documented area of ongoing research and practical application.

- Freddie Mac bundles the loans it buys into investment products known as Mortgage-Backed Securities (MBS).

- These securities are then sold to investors around the globe, from pension funds to insurance companies.

- Because these investments are backed by Freddie Mac, they are considered very safe, which keeps global capital flowing into the U.S. housing market and helps keep your mortgage rates competitive.

Why This Matters for Your “Fast and Consistent” Closing

Freddie Mac’s role isn’t just about money; it’s also about efficiency. By creating a set of standardized guidelines for mortgages, it makes the entire process smoother.

- These standardized guidelines allow for faster, more predictable loan processing because lenders know exactly what criteria a loan must meet to be sold.

- Freddie Mac provides lenders with powerful automated underwriting systems, like its Loan Product Advisor®, which can analyze a loan application in minutes.

- When your loan application meets these well-defined “conforming” standards, it leads to a stress-free experience and a consistent path to closing day.

Freddie Mac vs. Fannie Mae: Understanding the Dynamic Duo of Housing Finance

You’ll often hear Freddie Mac mentioned alongside another GSE, Fannie Mae. For the average Melbourne homebuyer, the practical difference between them is minimal, but it’s helpful to know they are two sides of the same coin.

- Both are GSEs that perform the nearly identical role of buying mortgages on the secondary market.

- Historically, they purchased loans from different types of lenders, but today their operations are very similar.

- Your lender, not you, will typically decide whether your loan is better suited for Freddie Mac or Fannie Mae guidelines.

- An expert lender like Morgan Financial is fluent in both sets of guidelines and will navigate them to find the best possible fit for your financial situation.

Key Similarities in Standards

For conventional loans, Freddie Mac and Fannie Mae are more alike than different. They are both overseen by the FHFA, which means their core requirements are closely aligned.

- They follow the same conforming loan limits set annually by the FHFA.

- They require similar credit score, down payment, and debt-to-income thresholds for conventional loans.

- The impact on your interest rate and monthly payment is generally the same regardless of which GSE ultimately backs your loan.

Minor Differences Borrowers Should Know

While subtle, some differences can matter in specific scenarios. This is where having an experienced mortgage partner is crucial.

- They may have slight variations in how they treat certain types of income (like self-employment) or specific debt obligations.

- Each has its own unique affordable loan programs, such as Freddie Mac’s Home Possible® program.

- Having a lender who understands these nuances ensures your application is structured for success from the very beginning.

Conforming Loan Limits and Your Space Coast Home Purchase

Freddie Mac and Fannie Mae only purchase mortgages up to a specific dollar amount. This ceiling is known as the “conforming loan limit,” and it’s a critical number for anyone planning to purchase a home in Florida.

- These limits are set each year by the FHFA and are based on average home price changes.

- Loans that fall within these limits are called “conforming loans.”

- Loans that exceed these limits are called “Jumbo loans,” which have different qualification criteria. Morgan Financial is an expert in both.

- In high-value areas like Satellite Beach or Indialantic, understanding these limits is especially important as you start your home search.

Conforming Limits for Brevard County

For most of Brevard County, the standard conforming loan limit applies. This limit for a single-family home is adjusted annually to keep pace with the local real estate market. An expert at Morgan Financial can provide you with the exact, up-to-date limit for the current year. If your dream home in Viera exceeds this limit, we can seamlessly transition you to one of our competitive Jumbo loan options.

Qualifying for a Freddie Mac-Backed Loan

To qualify for a conventional loan that meets Freddie Mac guidelines, lenders will assess a few key areas of your financial profile:

- Down Payment: While 20% is ideal to avoid private mortgage insurance (PMI), some Freddie Mac-backed programs allow down payments as low as 3%.

- Credit Score: A higher credit score generally leads to a better interest rate. Lenders look for strong, consistent credit histories.

- Debt-to-Income (DTI) Ratio: This is a measure of your monthly debt payments compared to your gross monthly income. Freddie Mac has specific DTI thresholds that borrowers must meet.

Navigating Freddie Mac Guidelines with Melbourne’s Trusted Mortgage Experts

Freddie Mac is a national entity, but your homebuying journey is deeply local. Morgan Financial acts as your personal liaison, translating these complex federal standards into a simple, clear, and successful mortgage experience right here on the Space Coast.

- We understand the nuances of Freddie Mac requirements and how they apply to the Brevard County market.

- Our expertise in conventional, VA, and jumbo loans ensures you get the right product for your unique goals.

- As a veteran-owned and Florida-focused lender, we combine national-level knowledge with the dedicated service a national call center can’t match.

The Morgan Financial Difference: Fast. Enjoyable. Consistent.

We believe getting a mortgage shouldn’t be stressful. Our entire process is built to deliver on our promise of a superior homebuying experience.

- We leverage cutting-edge technology to streamline underwriting that is fully compliant with Freddie Mac standards, ensuring speed and accuracy.

- We provide personalized, one-on-one service for buyers in Cocoa Beach, Merritt Island, and every corner of Brevard County.

- Our team is committed to total transparency, so you’ll always know the status of your loan and understand every step of the process.

Ready to Start Your Space Coast Home Search?

The first step toward buying a home is getting pre-approved. This shows sellers you are a serious buyer and gives you a clear budget to work with.

- A pre-approval from Morgan Financial confirms your eligibility for loan programs that meet Freddie Mac standards.

- We can evaluate your financial profile today and help you understand your buying power in Rockledge, Cape Canaveral, or your desired neighborhood.

- Contact a Mortgage Expert at Morgan Financial to explore your options.

Frequently Asked Questions About Freddie Mac

- Does Freddie Mac lend money directly to homebuyers?

- No. Freddie Mac does not originate loans or work directly with consumers. It operates in the secondary market by purchasing loans from primary lenders like Morgan Financial, who you work with to secure your mortgage.

- How do I know if Freddie Mac owns my mortgage in Florida?

- After your loan closes, you can use the official Freddie Mac Loan Look-Up Tool to see if they own your loan. You will need to provide basic information like your name, address, and the last four digits of your Social Security number. You can find the secure tool on their website: Freddie Mac Loan Look-Up Tool.

- What is the difference between Freddie Mac and FHA loans?

- Freddie Mac backs conventional loans, which are not insured or guaranteed by the federal government. FHA loans are a type of government-backed loan insured by the Federal Housing Administration, designed to help buyers with lower credit scores or smaller down payments. Morgan Financial specializes in conventional loans, not FHA loans.

- Why did Freddie Mac buy my loan after I closed with Morgan Financial?

- This is a standard and healthy part of the mortgage process. By selling your loan to Freddie Mac, we replenish our funds, allowing us to continue providing mortgages to other homebuyers in the community. Your loan terms do not change, and in many cases, you will continue to make your payments to the same loan servicer.

- Can I get a VA loan through Freddie Mac?

- No, Freddie Mac does not purchase VA loans. VA loans are guaranteed by the U.S. Department of Veterans Affairs and are securitized by a different GSE called Ginnie Mae. As veteran-owned VA loan experts, Morgan Financial can guide you through that separate process. You can learn more in our VA Loan Resource center.

- What is a “conforming loan”?

- A conforming loan is a mortgage that meets the size and underwriting guidelines set by the FHFA, allowing it to be purchased by Freddie Mac or Fannie Mae. Loans that exceed the maximum size limit are known as “jumbo loans.”

- Does Freddie Mac set the interest rates for my Melbourne mortgage?

- No. Freddie Mac does not set interest rates. Rates are determined by the primary lender (like Morgan Financial) based on overall market conditions, the specifics of the loan product, and your individual financial profile, including your credit score and down payment.

- What happens to my mortgage if Freddie Mac goes out of business?

- This is extremely unlikely given its critical role in the U.S. housing market and its oversight by the federal government. However, even if it were to happen, your mortgage would still be valid. The ownership of the loan would simply be transferred to another entity, and your obligation to make payments as agreed would remain unchanged.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.