Mortgage underwriting is the lender’s review of your income, credit, assets, property, title, insurance, and loan program rules before final approval. For Brevard County homebuyers, underwriting often includes extra attention to Florida property taxes, homeowners insurance, flood risk, condo or HOA details, and any conditions that must be cleared before closing.

Key Takeaways

- A Loan Estimate is a three-page form provided after a mortgage application, and the CFPB says the lender must provide it within three business days of receiving the application.

- A Loan Estimate does not mean the loan is approved; the CFPB says the lender may still ask for additional financial information if the borrower moves forward.

- A Closing Disclosure is a five-page form with final loan terms, projected payments, and closing costs, and the lender must provide it at least three business days before closing.

- Fannie Mae says stable and predictable income is a foundational part of loan underwriting, and lenders must document that income is stable, has a history of receipt, and is reasonably expected to continue.

- Florida property owners may qualify for homestead benefits that can reduce taxable value by as much as $50,000, but applications go through the county property appraiser.

What is mortgage underwriting?

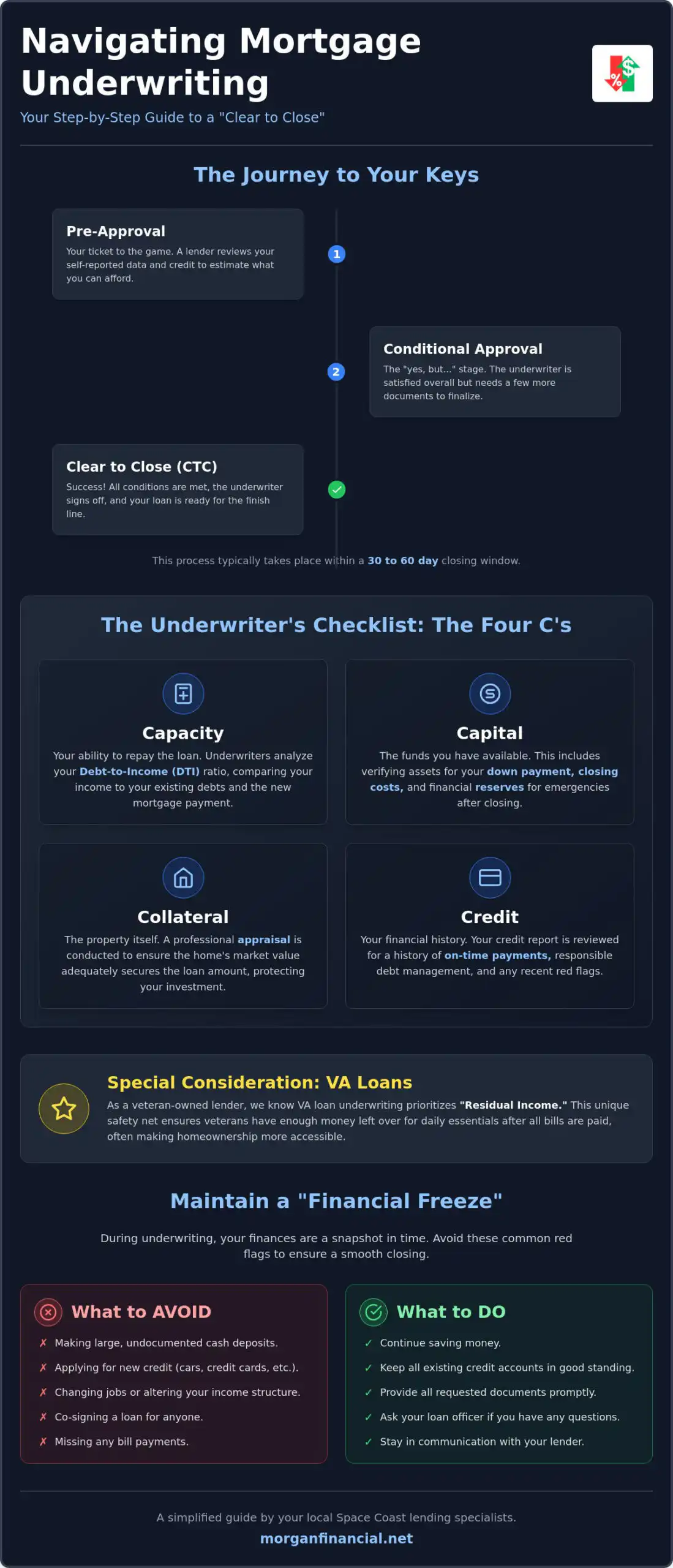

Mortgage underwriting is the step where the lender verifies that the borrower, property, and loan terms meet program and investor requirements before the loan can close. It is not just a credit check; it is a full review of the loan file.

An underwriter may review your pay stubs, W-2s, tax returns, bank statements, credit report, debts, gift funds, contract, appraisal, title work, homeowners insurance, flood certification, and loan program findings.

For a Brevard County buyer, the property side can matter as much as the borrower side. A home in Melbourne, Viera, Palm Bay, Cocoa Beach, Satellite Beach, Titusville, or Cape Canaveral may raise different questions about insurance, flood risk, condo review, repairs, or property tax estimates.

Underwriting is normal. A request for more documents does not automatically mean something is wrong.

What happens during mortgage underwriting in Brevard County?

During mortgage underwriting, the lender checks whether your income, credit, assets, property, insurance, and closing details support the loan you are requesting. The goal is to confirm that the file meets the rules before the lender issues final approval.

Here is a simple view of what underwriting usually reviews:

| Underwriting area | What the underwriter reviews | Brevard buyer example |

|---|---|---|

| Income | Pay, self-employment, bonuses, retirement income, military income, or other qualifying income | A Patrick Space Force Base buyer using BAH, base pay, or spouse income |

| Credit | Credit history, payment patterns, debts, disputes, and new accounts | A buyer who opened furniture credit before closing may need review |

| Assets | Down payment, closing costs, reserves, gift funds, and source of deposits | A Palm Bay buyer with a large recent bank deposit may need documentation |

| Property | Appraisal, property type, repairs, condo status, and occupancy | A Cocoa Beach condo may need condo project review |

| Insurance | Homeowners, wind, flood, and coverage details | A beachside property may need early insurance quoting |

| Title | Ownership history, liens, judgments, taxes, and closing requirements | A title issue may need to clear before closing |

| Loan program | FHA, VA, conventional, USDA, or assistance rules | A VA borrower must meet VA and lender requirements |

| Closing disclosure | Final terms, payment, and closing costs | The CFPB says the Closing Disclosure must arrive at least three business days before closing. |

Florida adds a few local pressure points. Insurance availability, wind mitigation, flood coverage, HOA budgets, condo documents, and tax estimates can all affect the final approval path.

Why does underwriting ask for more documents?

Underwriting asks for more documents when the file needs clarification, updated information, or proof that a guideline has been met. A document request is common and does not automatically mean the loan is in trouble.

Fannie Mae’s Selling Guide says stable and predictable income is foundational to underwriting, and the lender must document that income has a history and is reasonably expected to continue. That is why an underwriter may ask for updated pay stubs, a written verification of employment, tax returns, a profit-and-loss statement, or an explanation of income changes.

Fannie Mae also says Desktop Underwriter may give minimum income documentation requirements, but the lender must decide whether more documentation is needed for the specific borrower and situation. In plain English, automated findings help, but the lender still has to make sure the file makes sense.

Common underwriting requests include:

- Updated pay stubs or bank statements.

- A letter explaining a credit inquiry or late payment.

- Proof of where a large deposit came from.

- Gift letter and donor documentation.

- Updated homeowners insurance quote.

- Condo or HOA documents.

- Appraisal repair confirmation.

- Clarification on employment, overtime, commission, or self-employment income.

- Final verification that no new debt has changed the approval picture.

The best response is fast, complete, and simple. Send exactly what the mortgage team asks for, avoid partial screenshots when full statements are needed, and do not move money around without asking first.

What can delay mortgage underwriting?

Mortgage underwriting is most often delayed by missing documents, new debt, unclear deposits, appraisal issues, title problems, insurance changes, or property-specific concerns. Many delays are preventable when buyers stay responsive and avoid financial changes before closing.

In Brevard County, underwriting delays may come from Florida-specific property issues. A coastal or barrier island property may need flood or wind insurance review. A condo in Cocoa Beach, Satellite Beach, or Cape Canaveral may need project documentation. A home with roof, electrical, plumbing, or safety issues may need repairs before final approval depending on the loan program.

Property taxes can also confuse payment estimates. The Brevard County Property Appraiser warns buyers not to assume property taxes will remain the same after purchasing real estate. Florida buyers should also understand that homestead benefits may reduce taxable value for eligible permanent residents, but the application goes through the county property appraiser.

Avoid these actions during underwriting:

- Do not open new credit cards.

- Do not finance furniture, appliances, a boat, or a vehicle.

- Do not change jobs without discussing it first.

- Do not make large undocumented deposits.

- Do not move funds between accounts without keeping a paper trail.

- Do not ignore insurance, title, or appraisal requests.

- Do not assume a pre-approval is the same as final approval.

What does conditional approval mean?

Conditional approval means the underwriter has reviewed the file and identified items that must be satisfied before the loan can receive final approval or clear to close. It is a positive step, but it is not the finish line.

Conditions can be borrower-related, property-related, title-related, insurance-related, or closing-related. Some are simple, like an updated pay stub. Others may take longer, like an appraisal revision, condo document review, title correction, or proof that a repair has been completed.

A “clear to close” usually means the lender has cleared the required underwriting conditions and the closing process can move forward, subject to final closing documents, funding, and any last-minute quality control checks.

The CFPB says the Closing Disclosure gives final details about the loan terms, projected payments, and closing costs, and the lender must give it at least three business days before closing. Brevard buyers should use that three-day review period to compare the final numbers with earlier estimates and ask questions before signing.

How can Brevard homebuyers make underwriting smoother?

Brevard homebuyers can make underwriting smoother by getting fully documented early, responding quickly, avoiding new debt, and reviewing insurance and property details before the final week. Preparation is the best way to reduce stress.

Use this underwriting checklist before and during contract:

- Get mortgage reviewed before shopping. A strong file starts before the offer.

- Send complete documents. Full bank statements are better than screenshots.

- Explain income clearly. Tell the mortgage team about overtime, commission, bonus, self-employment, military income, retirement income, or job changes.

- Document assets. Keep records for large deposits, transfers, gifts, and funds used for closing.

- Quote insurance early. Florida homeowners insurance, wind coverage, and flood coverage can affect affordability and underwriting.

- Check property type. Condos, manufactured homes, multi-unit homes, and homes needing repairs can require more review.

- Stay financially quiet. Do not open new credit or take on new debt before closing.

- Review the Loan Estimate. The CFPB says the Loan Estimate includes estimated rate, monthly payment, closing costs, taxes, insurance, and whether terms may change.

- Review the Closing Disclosure. Compare final loan terms and closing costs before signing.

- Keep your mortgage team updated. New deposits, job changes, contract changes, inspection issues, or insurance changes should be shared quickly.

Morgan Financial is local to Melbourne and understands the Space Coast market. That matters when a loan file involves Brevard property taxes, insurance, flood zones, VA borrowers, military relocation, beachside condos, or tight contract timelines.

FAQ: Mortgage Underwriting for Brevard Homebuyers

Is mortgage underwriting the same as pre-approval?

No. Pre-approval is an early review of your loan qualifications, while underwriting is the deeper file review before closing. Underwriting verifies documents, property details, title, insurance, and loan program rules. A pre-approval can help you shop, but final approval depends on the full file.

Does a Loan Estimate mean I am approved?

No. The CFPB says a Loan Estimate shows the loan terms the lender expects to offer if you move forward, but it does not mean the lender has approved or denied your application. The lender may still ask for more financial information during processing and underwriting.

Why did underwriting ask for the same document again?

Usually, underwriting asks again because a document expired, was incomplete, had missing pages, showed a new issue, or needed clarification. Bank statements, pay stubs, insurance quotes, and employment information may need updates before closing. Send complete documents quickly to keep the file moving.

Can I be denied after conditional approval?

Yes. Conditional approval is not final approval. A loan can still run into problems if conditions are not cleared, new debt appears, income changes, insurance is unacceptable, appraisal issues are unresolved, or title problems remain. Do not make financial changes until after the loan closes.

How long does underwriting take in Brevard County?

It depends. Timing varies by loan type, documentation, appraisal, title, insurance, property type, and how quickly conditions are answered. A straightforward file may move faster than a condo, self-employed borrower, repair issue, or complex VA/FHA file. Ask Morgan Financial for a current local timeline.

What should I avoid during mortgage underwriting?

Avoid new credit, large purchases, job changes, undocumented deposits, moving funds without records, and ignoring document requests. These actions can change your credit, debt-to-income ratio, assets, or approval findings. Before changing anything financial, ask your mortgage team how it may affect the file.

Why does Florida insurance matter in underwriting?

Florida insurance matters because the lender must confirm acceptable property coverage before closing. Homeowners insurance, wind coverage, flood coverage, deductibles, and premium changes can affect both property eligibility and monthly payment. In Brevard County, quote insurance early, especially for coastal, condo, or older homes.

What happens after clear to close?

Usually, clear to close means the main underwriting conditions are satisfied and closing documents can be prepared. You still need to review the Closing Disclosure, bring any required funds, sign final documents, and complete funding. The CFPB says the Closing Disclosure must be provided at least three business days before closing.

Conclusion

Mortgage underwriting is the final detailed review that confirms whether your income, credit, assets, property, title, insurance, and loan program meet approval requirements. For Brevard homebuyers, local factors like property taxes, Florida insurance, flood risk, condo review, and military relocation can make preparation even more important.

Morgan Financial helps Space Coast buyers understand the underwriting process before surprises create stress. Contact Morgan Financial for local mortgage guidance before you write an offer or as soon as your file enters underwriting.

Compliance Disclaimer

Mortgage guidelines, rates, fees, and program requirements can change and may vary based on credit, income, assets, property type, occupancy, loan amount, and underwriting findings. This article is for educational purposes only and is not a commitment to lend or a guarantee of approval. Contact Morgan Financial for guidance specific to your situation.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.