Key Takeaways

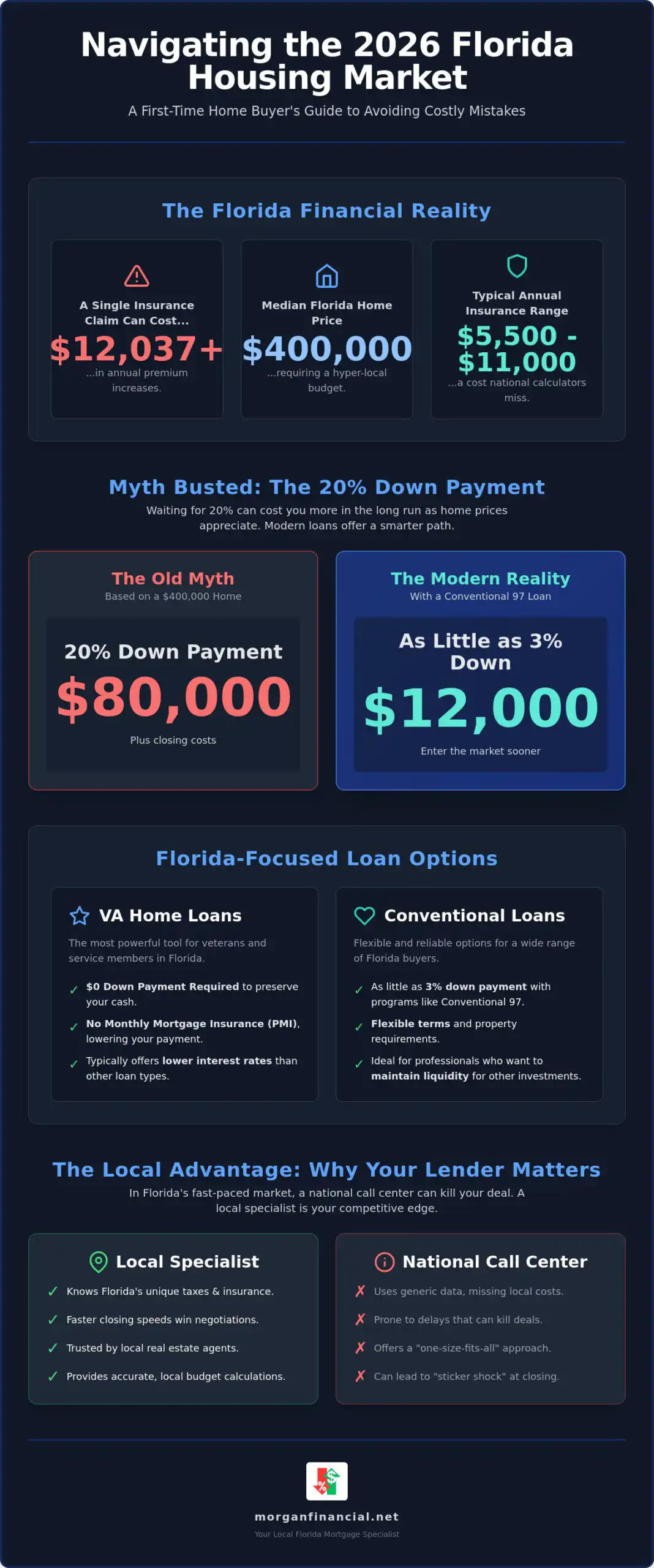

- A 2026 conventional loan may be limited by the FHFA conforming loan limit, which is $832,750 for a one-unit property in most U.S. areas.

- A Loan Estimate is a three-page form that lenders must provide within three business days after receiving a mortgage application, and it shows estimated rate, payment, taxes, insurance, and closing costs.

- Florida homeowners may qualify for a homestead exemption that can reduce taxable value by as much as $50,000 if the property is their permanent residence.

- Most homeowners insurance does not cover flood damage, and NFIP building coverage for homeowners is capped at $250,000 with contents coverage up to $100,000.

- Eligible VA buyers may be able to buy with no down payment, but they must still meet VA and lender standards for credit, income, occupancy, and the full loan file.

What are the most common first time home buyer mistakes in Florida in 2026?

The biggest first time home buyer mistakes in Florida happen when buyers focus only on the purchase price instead of the full monthly payment, approval strength, insurance risk, and cash needed to close. A home that looks affordable online may feel very different after taxes, homeowners insurance, flood insurance, HOA dues, mortgage insurance, and closing costs are added.

Florida buyers should treat the mortgage payment as only one part of the budget. In Brevard County, Space Coast buyers should also think about coastal exposure, condo rules, military relocation timelines, and insurance availability before choosing a property.

Here are the mistakes Morgan Financial sees buyers try to avoid before making an offer:

| Mistake | Why it matters in Florida | Better move |

|---|---|---|

| Shopping before pre-approval | You may not know your real budget or loan options | Get reviewed before touring homes |

| Budgeting only for principal and interest | Taxes, insurance, HOA dues, and mortgage insurance can change affordability | Review full payment and cash to close |

| Ignoring flood risk | Standard homeowners insurance usually does not cover flood damage | Check flood zone and quote coverage early |

| Waiting to compare loan programs | FHA, VA, conventional, and assistance options work differently | Compare programs before choosing a price range |

| Making credit changes before closing | New debt or lower credit scores can affect approval | Avoid new credit until after closing |

| Skipping Loan Estimate review | Fees and payment details may be misunderstood | Review the Loan Estimate line by line |

| Forgetting homestead timing | Tax savings are not automatic at closing | Apply with the county property appraiser after purchase |

Why is shopping before pre-approval a mistake?

Shopping before pre-approval is risky because a buyer may fall in love with a home before knowing the loan amount, monthly payment, and conditions they can actually support. A true mortgage review looks at income, credit, assets, debts, property type, and loan program fit.

Pre-approval is different from browsing online calculators. A calculator may not account for Florida homeowners insurance, flood insurance, HOA dues, mortgage insurance, or county-specific taxes.

A stronger first step is to speak with a Florida mortgage team before making offers. Morgan Financial can help buyers compare realistic payment ranges, documentation needs, and loan options before the search becomes emotional.

For Space Coast buyers near Melbourne, Viera, Palm Bay, Cocoa Beach, Titusville, Patrick Space Force Base, and Cape Canaveral, early preparation can also help with PCS timelines, VA eligibility questions, and fast-moving contracts.

How do Florida taxes, insurance, and flood risk change your real budget?

Florida buyers should budget for property taxes, homeowners insurance, possible flood insurance, HOA dues, and maintenance before deciding what home price is comfortable. These costs can change the monthly payment even when the interest rate and loan amount stay the same.

Florida’s homestead exemption may reduce taxable value by as much as $50,000 for eligible permanent residents, but the buyer must apply through the county property appraiser. The exemption is not the same as a lender credit, and it does not automatically make the first year’s escrow estimate lower.

Flood risk matters across Florida, not just on the beach. FEMA’s FloodSmart program says most homeowners and renters insurance does not cover flood damage, and NFIP homeowner building coverage is up to $250,000 while contents coverage is up to $100,000.

In Brevard County, buyers considering Cocoa Beach, Satellite Beach, Indialantic, Indian Harbour Beach, Melbourne Beach, or other coastal areas should quote insurance early. Buyers farther inland, including Melbourne, West Melbourne, Palm Bay, Rockledge, and Titusville, should still check flood maps and coverage options before closing.

What loan program mistakes should first-time buyers avoid?

First-time buyers should not choose a loan program based only on the lowest down payment because approval, mortgage insurance, seller concessions, property type, and long-term payment all matter. A lower down payment can help, but it does not automatically mean the lowest total cost.

Conventional loans, FHA loans, VA loans, USDA loans, and Florida assistance programs can all serve different borrowers. The right fit depends on credit, income, assets, military eligibility, property location, occupancy, and underwriting findings.

For 2026, the FHFA baseline conforming loan limit for one-unit properties is $832,750 in most of the United States, while high-cost area limits can be higher. Buyers using conventional financing should confirm the correct county limit and whether their loan amount is conforming or jumbo.

FHA limits are county-based, and HUD’s FHA Mortgage Limits tool lets buyers look up FHA or GSE mortgage limits by state, county, MSA, limit type, and year.

Eligible veterans, active-duty service members, and certain surviving spouses should also review VA loan options early. VA says a VA-backed purchase loan can offer no down payment when the sales price is not higher than the appraised value, but the borrower must still meet VA and lender standards for credit, income, occupancy, and other requirements.

How can buyers avoid closing-cost and contract surprises?

Buyers can avoid closing-cost surprises by reviewing the Loan Estimate early, asking what can change, and confirming seller credits, escrows, prepaid items, and inspection-related costs before signing. The lowest advertised payment is not always the full cost of buying.

The CFPB says the Loan Estimate shows the estimated interest rate, monthly payment, total closing costs, taxes, insurance, and whether payments may change later. It also explains that receiving a Loan Estimate does not mean the loan has been approved or denied.

Florida buyers should pay close attention to these items:

- Down payment: The amount you put toward the purchase price.

- Closing costs: Lender, title, recording, appraisal, credit report, prepaid, and escrow-related charges.

- Prepaids: Upfront interest, insurance premiums, and tax/insurance escrow deposits.

- Seller credits: Funds the seller may agree to contribute, subject to loan program rules.

- HOA or condo costs: Application fees, estoppel fees, transfer fees, dues, reserves, and special assessments.

- Inspection costs: Home inspection, wind mitigation, four-point inspection, termite inspection, pool inspection, or roof review when needed.

- Rate-lock terms: How long the rate is locked and what happens if closing is delayed.

A good rule is to review the Loan Estimate before you spend money on inspections, moving plans, or furniture. Buyers should also avoid opening new credit, financing a car, changing jobs, or moving funds around without talking to the mortgage team first.

What steps should Florida buyers take before making an offer?

A Florida buyer should complete mortgage preparation, document review, payment planning, insurance quoting, and property-risk checks before making an offer. This makes the offer stronger and reduces the chance of surprises during underwriting.

Use this process before you write a contract:

- Get mortgage reviewed. Share income, assets, debts, credit, and goals with a mortgage professional.

- Compare loan options. Review FHA, conventional, VA, USDA, and assistance options when applicable.

- Build a full payment estimate. Include principal, interest, taxes, homeowners insurance, flood insurance, HOA dues, and mortgage insurance.

- Check cash to close. Confirm down payment, closing costs, prepaids, escrow deposits, and reserves.

- Quote insurance early. Ask about homeowners, flood, wind, and property-specific concerns.

- Review property type. Condos, manufactured homes, multi-unit homes, and homes with repairs may need extra review.

- Protect your approval. Avoid new credit, large deposits without documentation, and major financial changes before closing.

- Plan the local timeline. Insert Morgan Financial local stat here: [Insert Morgan Financial average first-time buyer closing timeline or Brevard County buyer preparation statistic here].

For buyers in Viera, Palm Bay, Titusville, Satellite Beach, and the surrounding Space Coast, local guidance can be the difference between a clean contract and a stressful closing. Morgan Financial’s education-first approach helps buyers understand the numbers before they commit.

FAQ: Florida First-Time Home Buyer Mistakes

Is it a mistake to start home shopping before getting pre-approved?

Usually, yes. Shopping before pre-approval can lead to homes that do not match your actual budget, loan options, or cash-to-close range. A mortgage review helps you understand payment, loan program fit, required documents, and possible approval conditions before you make an offer.

Can a first-time buyer in Florida buy with less than 20% down?

Yes. Many first-time buyers may use FHA, VA, conventional low-down-payment, USDA, or assistance options depending on eligibility. Less than 20% down may involve mortgage insurance or program-specific costs, except some VA loans do not require monthly PMI or MIP for eligible borrowers.

Do Florida first-time buyers need flood insurance?

It depends. Flood insurance may be required if the property is in a high-risk flood zone and the buyer uses a mortgage, but buyers outside required zones may still choose coverage. FEMA says most homeowners insurance does not cover flood damage, so buyers should quote coverage early.

Is the Florida homestead exemption automatic after closing?

No. Florida’s homestead exemption is not automatic just because you bought a home. Eligible homeowners generally apply through the county property appraiser for their permanent residence. The Florida Department of Revenue says the exemption can reduce taxable value by as much as $50,000.

Should I compare FHA, VA, and conventional before choosing a home?

Yes. Loan program rules can affect down payment, mortgage insurance, appraisal requirements, seller credits, property eligibility, and total payment. Comparing programs before shopping helps you avoid choosing a property or price range that does not fit your approval path.

Can opening a new credit card hurt my mortgage approval?

Yes. New credit can change your credit score, monthly debt, debt-to-income ratio, and underwriting findings. Buyers should avoid new credit cards, car loans, furniture financing, and major purchases before closing unless their mortgage team confirms the impact first.

Does a Loan Estimate mean I am approved?

No. The CFPB says a Loan Estimate shows the terms the lender expects to offer if you move forward, but it does not mean the lender has approved or denied the loan. Final approval depends on underwriting, documentation, property review, and loan conditions.

Conclusion

The best way to avoid common Florida first-time buyer mistakes is to prepare before shopping, budget beyond the purchase price, and review loan options with a local mortgage team. Taxes, insurance, flood risk, closing costs, and loan program rules can all affect affordability.

Morgan Financial is a veteran-owned, veteran-operated, veteran-focused mortgage lender based in Melbourne, Florida. For help preparing to buy in Brevard County or anywhere in Florida, contact Morgan Financial before you make an offer.

Compliance Disclaimer

Mortgage guidelines, rates, fees, and program requirements can change and may vary based on credit, income, assets, property type, occupancy, loan amount, and underwriting findings. This article is for educational purposes only and is not a commitment to lend or a guarantee of approval. Contact Morgan Financial for guidance specific to your situation.

Disclaimer

This content is provided for informational purposes only and should not be construed as financial, legal, or lending advice. It is not a commitment to lend. Mortgage programs, rates, terms, and availability are subject to change without notice and may vary by borrower and location. All loans are subject to credit approval and applicable underwriting guidelines. Not all applicants will qualify. Consult with a licensed mortgage professional regarding your specific situation.